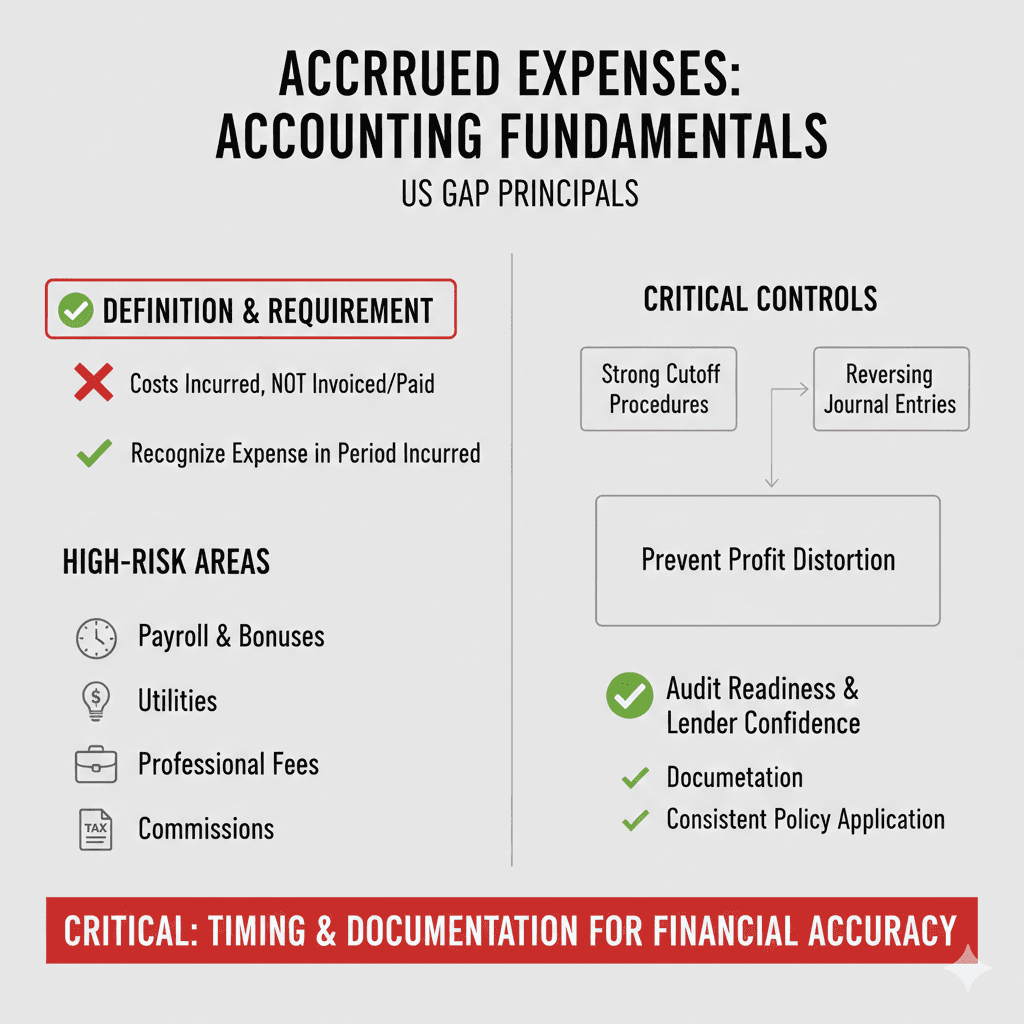

Accrued expenses are liabilities for costs incurred but not yet invoiced or paid.

US GAAP requires expenses to be recognized in the period incurred, not when cash is paid.

Payroll, bonuses, interest, utilities, professional fees, commissions, and taxes are the highest-risk month-end accrual areas.

Strong cutoff procedures and reversing journal entries prevent profit distortion.

Documentation and consistent policy application are critical for audit readiness and lender confidence.

Executive Summary

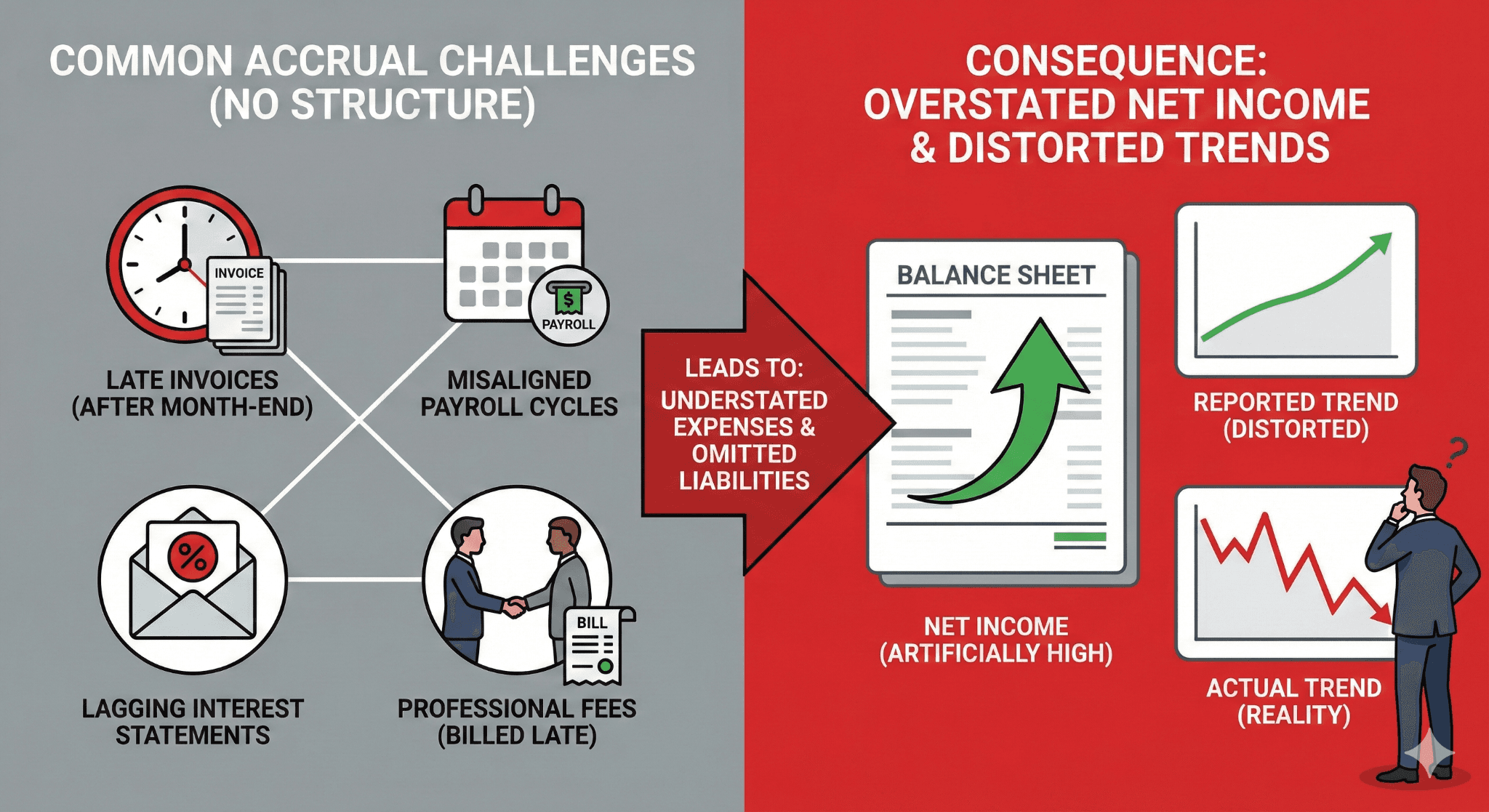

Accrued expenses are one of the most misunderstood yet financially impactful elements of a disciplined month-end close. Under US GAAP accrual accounting principles, expenses must be recognized in the period in which the obligation arises, regardless of when the invoice is received or cash is paid. This requirement directly affects profit, working capital, EBITDA, and covenant compliance.

In small and mid-market businesses, invoices frequently arrive after month-end. Payroll cycles rarely align with calendar periods. Interest statements lag. Professional fees are billed after services are completed. Without structured accrual procedures, expenses are routinely understated and liabilities omitted. The result is overstated net income and distorted trend analysis.

This guide explains the governing GAAP framework, defines key terminology, and walks through detailed case scenarios with calculations and journal entries. It also outlines practical QuickBooks Online workflows for recording and reversing accrual entries. Controllers, accountants, and bookkeepers can use this as a month-end playbook to implement consistent, defensible accrual accounting.

1. What Are Accrued Expenses Under US GAAP?

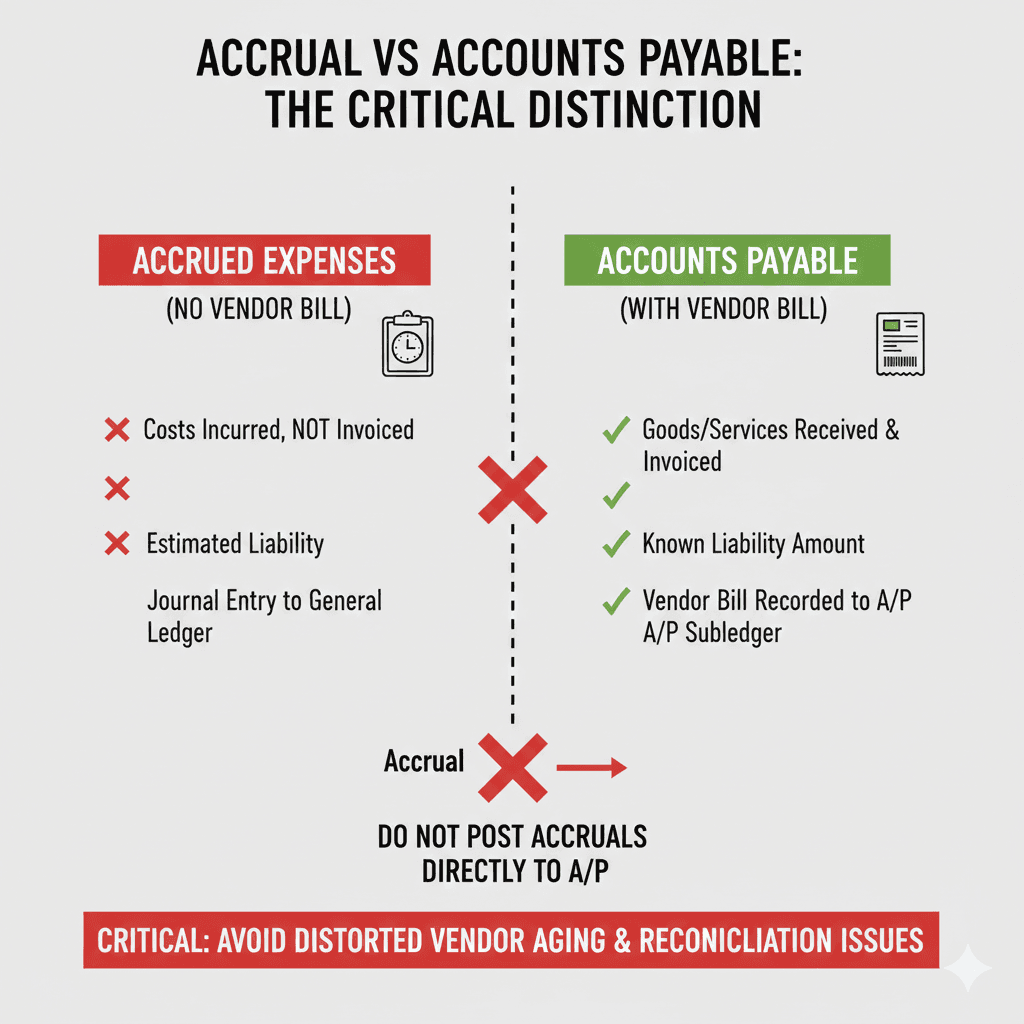

An accrued expense is a liability for goods or services received but not yet invoiced or paid. The obligation exists, even if paperwork has not arrived.

Under US GAAP accrual accounting principles, expenses must be recognized when incurred. This concept aligns with the matching principle, which requires expenses to be recorded in the same period as the related revenues.

Key Definitions

Accrual Accounting: Recognizing revenues and expenses when earned or incurred.

Accrued Liability: Obligation for expense incurred but unpaid.

Cutoff: Ensuring transactions are recorded in the correct reporting period.

Reversing Entry: Journal entry automatically reversed in the next accounting period.

Accrued Expense vs Accounts Payable vs Prepaid Expense

Item | Accrued Expense | Accounts Payable | Prepaid Expense |

Invoice received? | No | Yes | Yes |

Expense incurred? | Yes | Yes | Not yet |

Cash paid? | No | No | Yes |

Balance sheet classification | Liability | Liability | Asset |

Example | Payroll earned but unpaid | Vendor bill received | Insurance paid in advance |

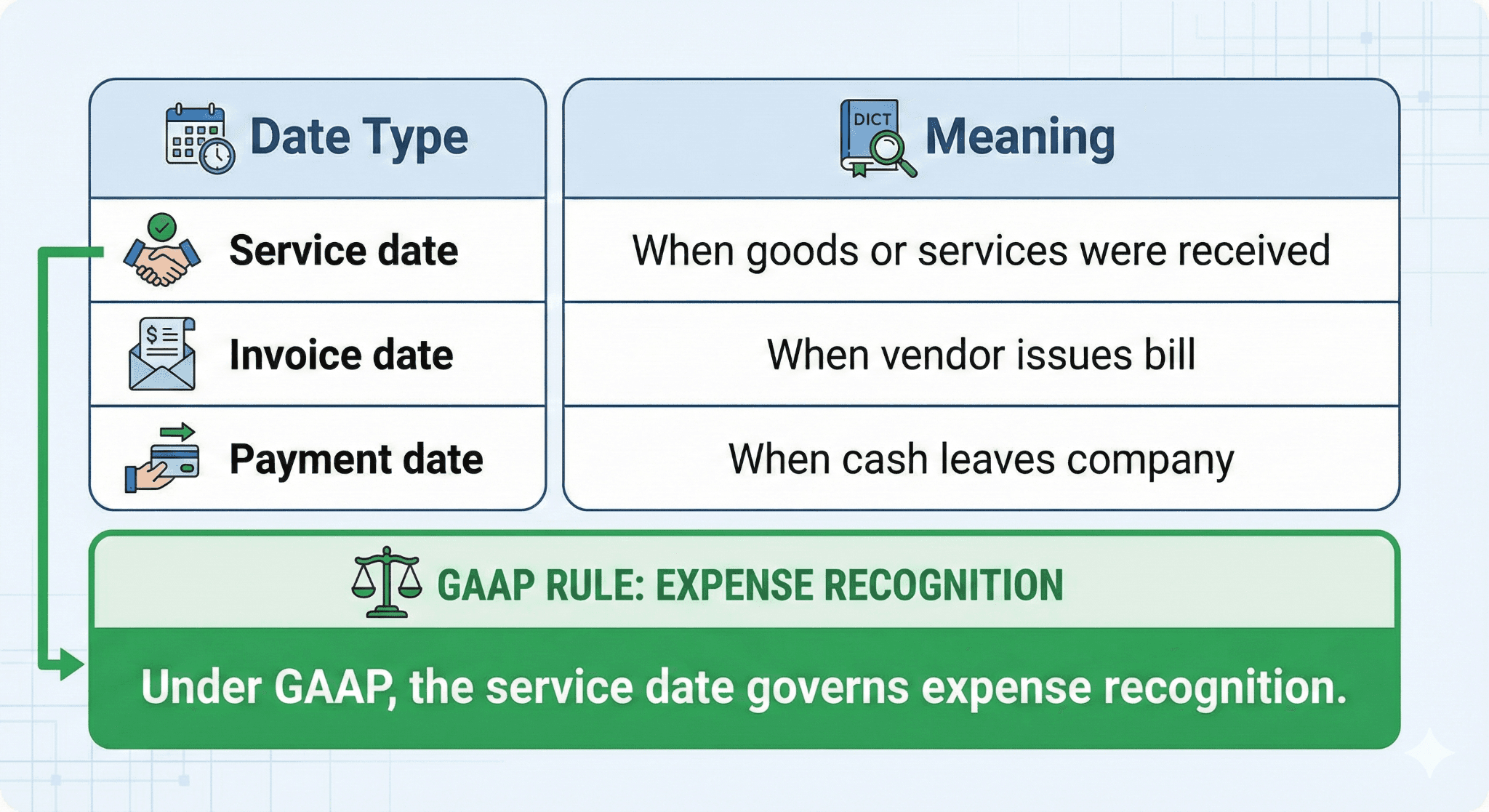

2. The Month-End Cutoff Framework

Month-end cutoff is the process of identifying expenses that relate to the current period but will be paid or invoiced later.

The Three Critical Dates

3. Detailed Case Scenarios

Below are real-world scenarios common in SMB environments. Each example includes calculations and journal entries.

Case Scenario 1: Payroll Accrual Across Period-End

Facts

Biweekly payroll covers March 20–April 2.

Payday is April 5.

Total payroll: $42,000.

Month-end is March 31.

Step 1: Calculate Daily Payroll

$42,000 ÷ 14 days = $3,000 per day.

Step 2: Determine Days in March

March 20–31 = 12 days.

Step 3: Calculate Accrual

12 × $3,000 = $36,000.

Journal Entry March 31

Dr Payroll Expense 36,000

Cr Accrued Payroll Liability 36,000

Reversal April 1

Dr Accrued Payroll Liability 36,000

Cr Payroll Expense 36,000

When payroll is processed April 5, the expense posts normally. The reversal prevents duplication.

Impact if Not Accrued

March profit overstated by $36,000.

April profit understated by $36,000.

For businesses with thin margins, this distortion materially affects EBITDA.

Case Scenario 2: Employer Payroll Taxes

Assume employer payroll taxes equal 8 percent of gross wages.

Accrued wages: $36,000

Employer taxes: $2,880

Combined Accrual Entry

Dr Payroll Expense 36,000

Dr Payroll Tax Expense 2,880

Cr Accrued Payroll Liability 38,880

Many businesses forget employer taxes in accrual calculations, understating liabilities.

Case Scenario 3: Accrued Interest on Term Loan

Facts

Principal: $1,200,000

Interest rate: 7 percent annually

Monthly interest payment due on 15th of following month

Month-end: June 30

Monthly Interest Calculation

$1,200,000 × 7% ÷ 12 = $7,000.

If no invoice or bank debit has occurred, June still requires accrual.

Journal Entry June 30

Dr Interest Expense 7,000

Cr Accrued Interest Payable 7,000

If omitted, liabilities are understated and interest coverage ratios inflated.

Case Scenario 4: Utilities Accrual with Estimation

Electricity usage varies seasonally.

Facts

July invoice received August 12 for $9,800.

June invoice was $8,900.

Production volume increased 5 percent in July.

Estimate July expense:

$8,900 × 1.05 ≈ $9,345.

Conservative approach may round to $9,500.

Journal Entry July 31

Dr Utilities Expense 9,500

Cr Accrued Utilities Liability 9,500

When actual invoice arrives, adjust variance.

If actual invoice equals $9,800, record:

Dr Utilities Expense 300

Cr Accrued Utilities Liability 9,500

Cr Accounts Payable 300

Alternatively, reverse accrual and book full invoice.

Case Scenario 5: Professional Services Performed but Not Billed

Audit firm performs interim fieldwork December 10–20. Invoice expected January 25.

Engagement estimate: $60,000 total. Interim phase estimated at 40 percent.

Accrual required December 31:

$60,000 × 40% = $24,000.

Journal Entry December 31

Dr Professional Fees Expense 24,000

Cr Accrued Professional Fees 24,000

Failure to accrue may lead to audit adjustment.

Case Scenario 6: Sales Commissions Earned but Unpaid

Commission rate: 5 percent of sales.

December sales: $800,000.

Commissions paid January 10.

Accrual required:

$800,000 × 5% = $40,000.

Journal Entry December 31

Dr Commission Expense 40,000

Cr Accrued Commissions Payable 40,000

If omitted, gross margin appears artificially strong in December.

Case Scenario 7: Bonus Accrual Based on Annual Performance

Executive bonus tied to EBITDA target.

Performance metrics met as of year-end.

Bonus pool estimated at $150,000.

Under GAAP, if payment is probable and amount reasonably estimable, accrue liability.

Journal Entry December 31

Dr Bonus Expense 150,000

Cr Accrued Bonus Liability 150,000

Case Scenario 8: Property Taxes Assessed Quarterly

Annual property tax: $120,000.

Billed quarterly at $30,000.

Monthly accrual:

$120,000 ÷ 12 = $10,000.

Even if bill arrives April 15, January–March require accruals.

Case Scenario 9: Credit Card Charges at Month-End

Credit card statement closes May 28.

Expense incurred May 29–31 totals $12,500.

Statement not yet generated.

Review credit card portal activity and accrue:

Dr Various Expenses 12,500

Cr Accrued Credit Card Liability 12,500

Case Scenario 10: Construction Subcontractor Work Completed but Unbilled

Subcontractor completed $85,000 of work by September 30.

Billing expected October 15.

Accrue September 30:

Dr Construction Expense 85,000

Cr Accrued Subcontractor Payable 85,000

Job costing accuracy depends on this entry.

4. Estimation Techniques and Controls

Accrual accounting often requires estimation. Estimation must be reasonable and supported.

Common Estimation Methods

Method | Use Case | Example |

Straight-line allocation | Fixed annual costs | Property tax |

Historical average | Utilities | Prior month usage |

Percentage completion | Professional services | Audit engagement |

Rate-based calculation | Payroll or commissions | Daily wage rate |

Controllers should document assumptions and retain worksheets.

5. Reversing Entries in QuickBooks Online

QuickBooks Online allows automatic reversing entries dated first day of next month.

Workflow

Create journal entry dated last day of month.

Select “Reverse” option.

Set reversal date to first day of next period.

Attach supporting documentation.

Reversals prevent duplicate expense recognition when vendor bills are entered.

6. Advanced Mini Case: Multi-Accrual Close

A $25 million manufacturing company closing April identified:

Payroll accrual: $112,000

Commissions: $48,000

Utilities estimate: $15,000

Interest accrual: $9,500

Professional fees: $22,000

Total accruals: $206,500.

Before accruals, April net income: $480,000.

After accruals: $273,500.

Without accruals, EBITDA margin overstated by 4 percentage points. Lender covenant required minimum 12 percent margin. True margin fell to 11.2 percent, triggering internal review.

Accrual discipline prevented misleading reporting.

7. Common Errors and Audit Findings

Error | Consequence |

Accruing invoice date instead of service date | Period distortion |

Forgetting reversal | Double expense |

Using Accounts Payable for accrual | Aging confusion |

No documentation | Audit comment |

Ignoring employer payroll taxes | Liability understatement |

Cutoff errors remain a common audit adjustment in SMB financial statements.

8. Materiality and Policy Design

Each company should establish a written accrual policy.

Example policy elements:

Accrue items exceeding $2,500.

Accrue recurring categories regardless of amount.

Review all payroll periods spanning month-end.

Document all estimates.

Consistency is critical. Inconsistent accrual practices reduce financial statement reliability.

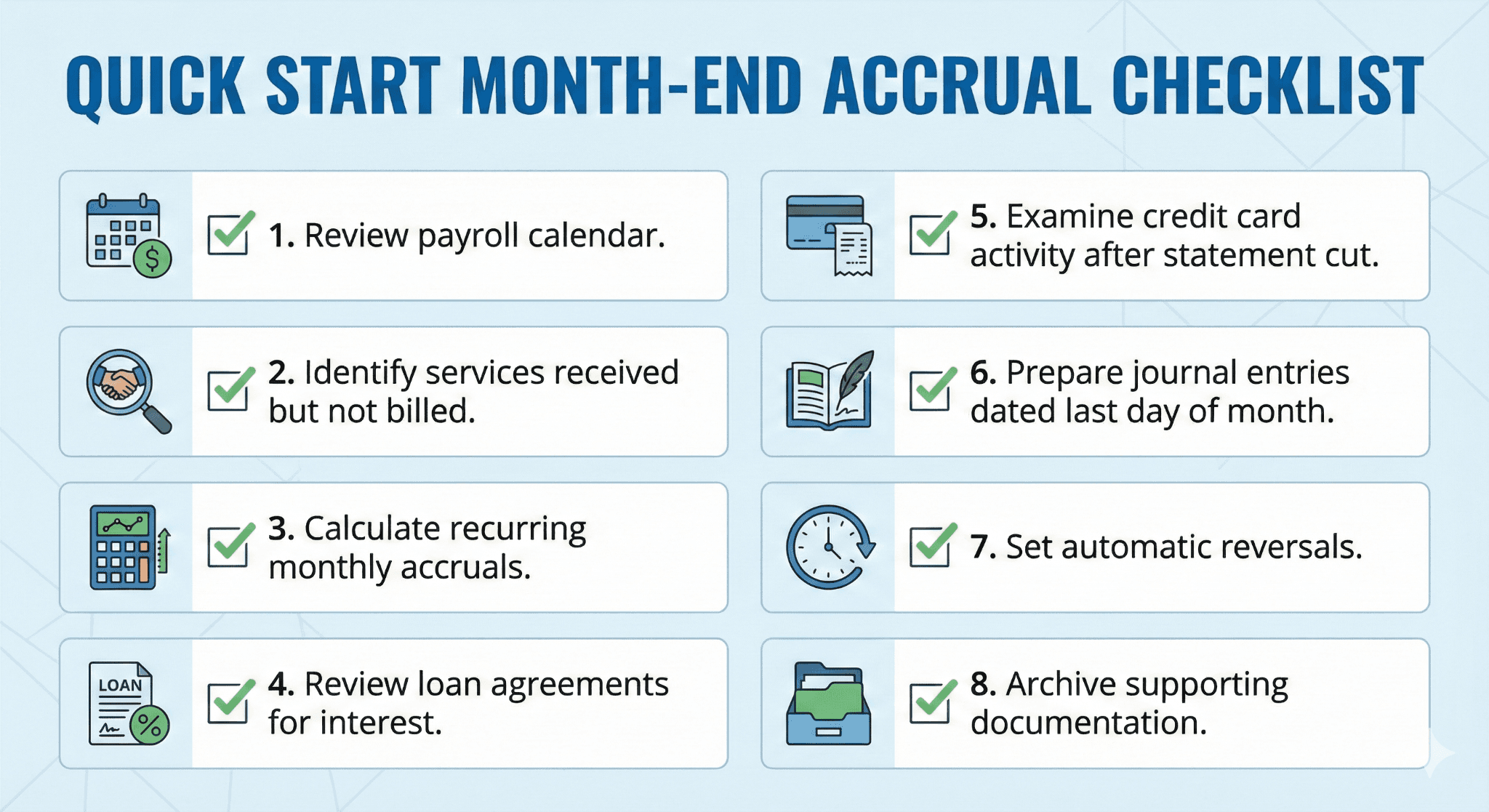

9. Quick Start Month-End Accrual Checklist

10. Frequently Asked Questions

1. Are accrued expenses required for small businesses?

If financial statements are prepared under GAAP, yes.

2. Can I wait for the invoice instead?

No. GAAP requires recognition when incurred.

3. How accurate must estimates be?

Reasonably accurate based on available information.

4. What is the largest accrual for service companies?

Payroll and commissions are typically largest.

5. Should accruals be reviewed monthly?

Yes. Update assumptions each month.

11. Risks and Mitigation

Risk | Financial Impact | Mitigation |

Understated liabilities | Inflated working capital | Formal cutoff checklist |

Profit volatility | Misleading trends | Consistent accrual schedule |

Covenant breach | Lender risk | Pre-close EBITDA analysis |

Audit adjustment | Reputational impact | Documentation binder |

12. Final Thoughts

Accrued expenses are not optional estimates. They are required elements of accrual accounting under US GAAP. For SMBs operating in QuickBooks Online, disciplined month-end accrual procedures transform financial reporting from reactive bookkeeping into reliable management accounting.

Accrual accounting aligns expenses with economic reality. It smooths volatility, protects credibility, and supports informed decision-making.

A structured accrual schedule, supported by documentation and reversing entries, is the backbone of a professional month-end close.

Glossary

Accrued Expense: Liability for expense incurred but unpaid.

Cutoff: Assigning transactions to correct reporting period.

Matching Principle: Recognizing expenses in same period as related revenue.

Reversing Entry: Journal entry reversed in next accounting period.

Materiality: Significance threshold affecting decision-making.