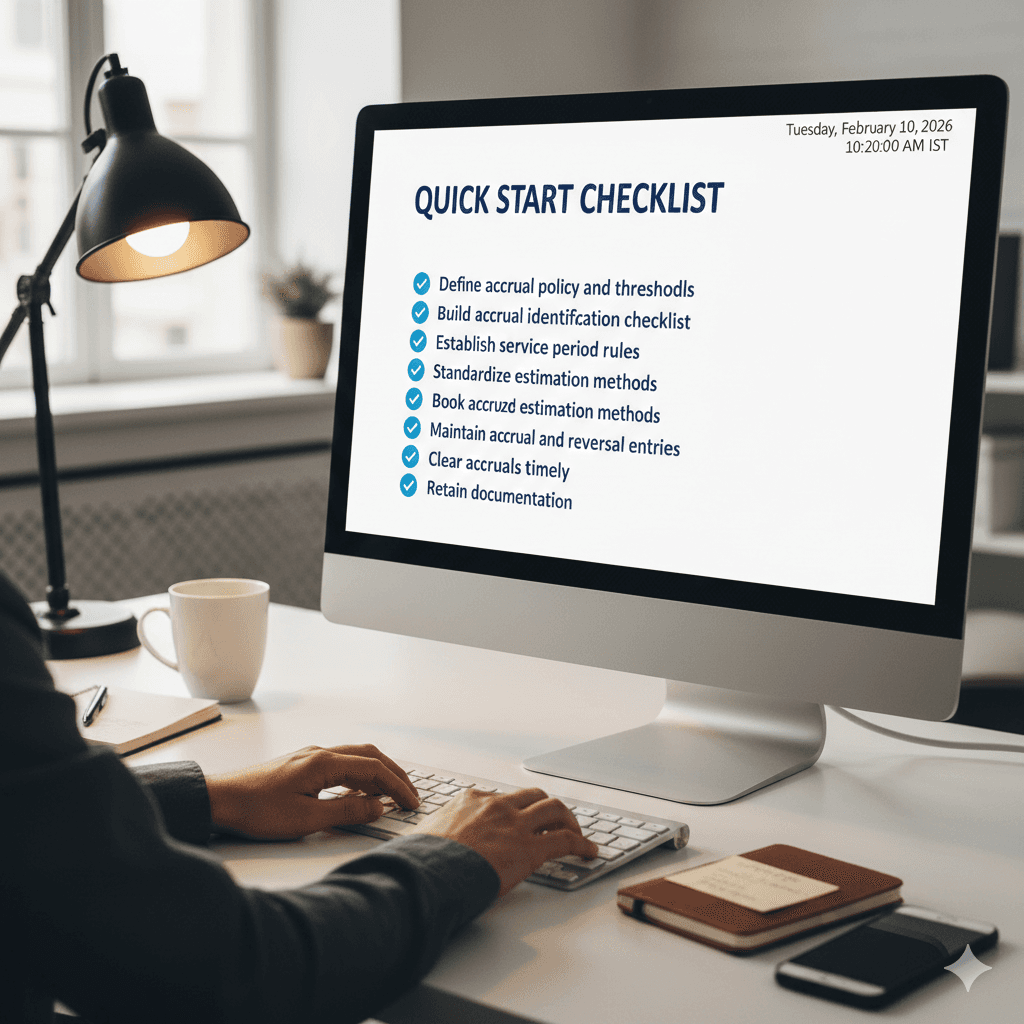

Accrued expenses fail at the intersection of timing, judgment, and weak documentation.

Invoice receipt date does not determine expense recognition.

Service period drives accrual decisions, not vendor billing behavior.

QuickBooks requires compensating controls for accruals.

Clear decision rules and evidence reduce audit adjustments dramatically.

Executive Summary

Accrued expenses exist to solve a timing problem. Services are received today. Invoices arrive later. Accounting must bridge that gap.

In QuickBooks-heavy environments, this bridge is fragile. Month-end closes depend on memory, inbox checks, and ad hoc journal entries. Teams debate whether to accrue based on invoice receipt dates instead of service periods. Documentation lives in emails or spreadsheets, disconnected from the general ledger.

Auditors do not test intent. They test outcomes. Missed accruals, late reversals, and unsupported estimates are among the most common findings in SMB and mid-market audits.

This article provides a practical framework for designing and implementing comprehensive internal control procedures for accrued expenses. The focus is execution. Each control is illustrated with real-life scenarios that accountants and controllers face every month, especially around cutoff, invoice timing, and service periods.

1. Understanding Accrued Expenses: The Non-Negotiables

1.1 What an Accrued Expense Is

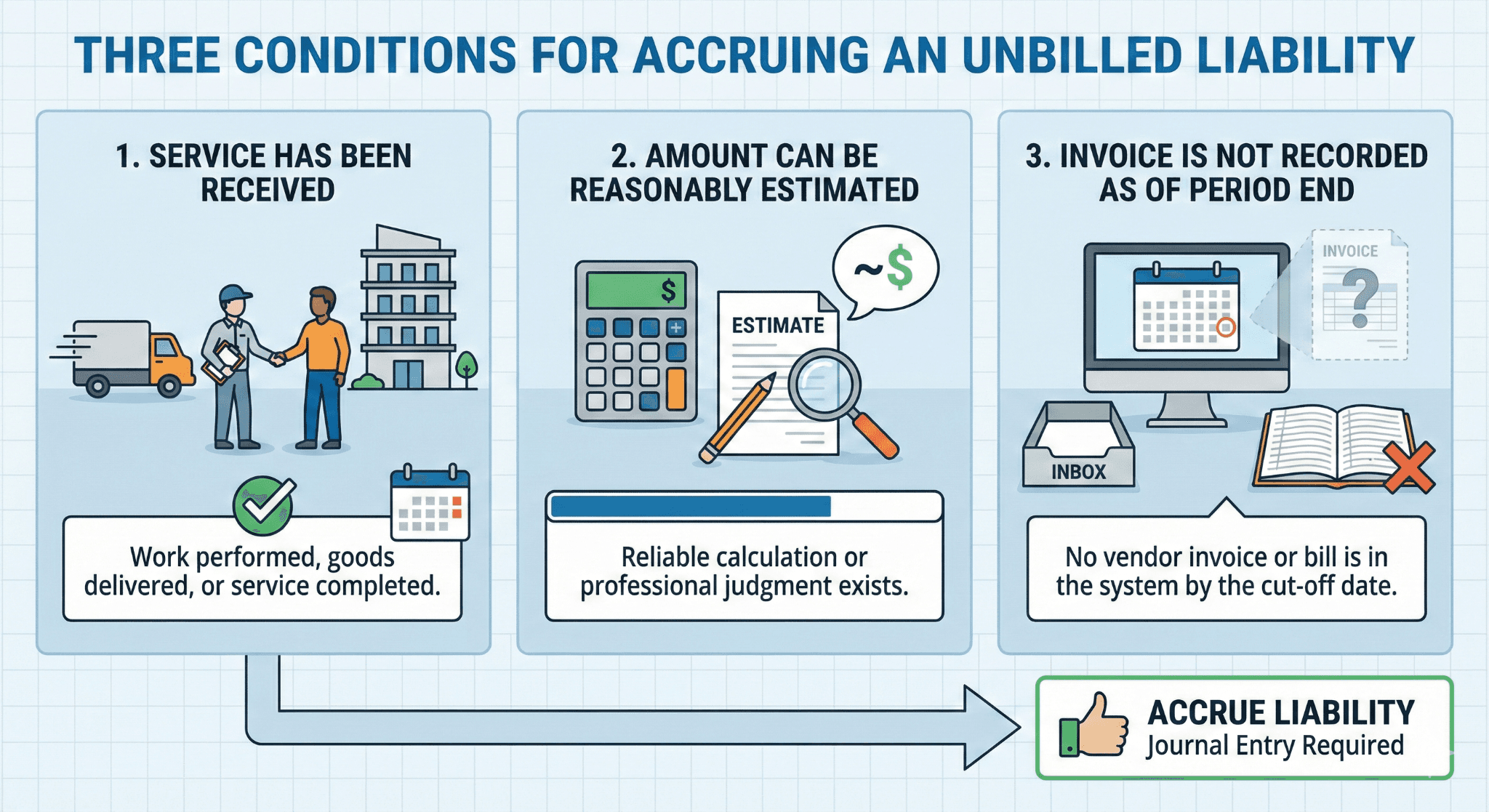

An accrued expense is a liability for goods or services already received but not yet invoiced or paid.

Three conditions must exist:

The service has been received.

The amount can be reasonably estimated.

The invoice is not recorded as of period end.

An accrued expense is a liability recorded on a company's balance sheet under U.S. Generally Accepted Accounting Principles (US GAAP) to reflect costs incurred during an accounting period for which payment has not yet been made. This concept is fundamental to the accrual basis of accounting and is required by the revenue recognition principle (ASC 606) and the expense recognition principle (matching principle), ensuring that expenses are reported in the same period as the revenues they helped generate.

Key US GAAP Requirements for Recognizing Accrued Expenses:

Definition of a Liability (FASB Concepts Statement No. 6): An accrued expense meets the definition of a liability, which is a probable future sacrifice of economic benefits arising from present obligations of a particular entity to transfer assets or provide services to other entities in the future as a result of past transactions or events. The obligation arises because the entity has received the service or benefit.

Expense Recognition (Matching Principle): The expense must be recognized in the period the goods or services were consumed or the economic benefit was received, regardless of when the invoice is received or cash is paid. This ensures the company's financial statements accurately reflect the true economic performance of the period.

Measurability: The amount of the expense must be reasonably estimable. While an exact invoice is not required, US GAAP requires that the amount recorded be based on the best available objective information, such as contract terms, historical patterns, or standard rates. If the amount cannot be reasonably estimated, the expense should not be accrued, and disclosure may be required if the potential liability is material.

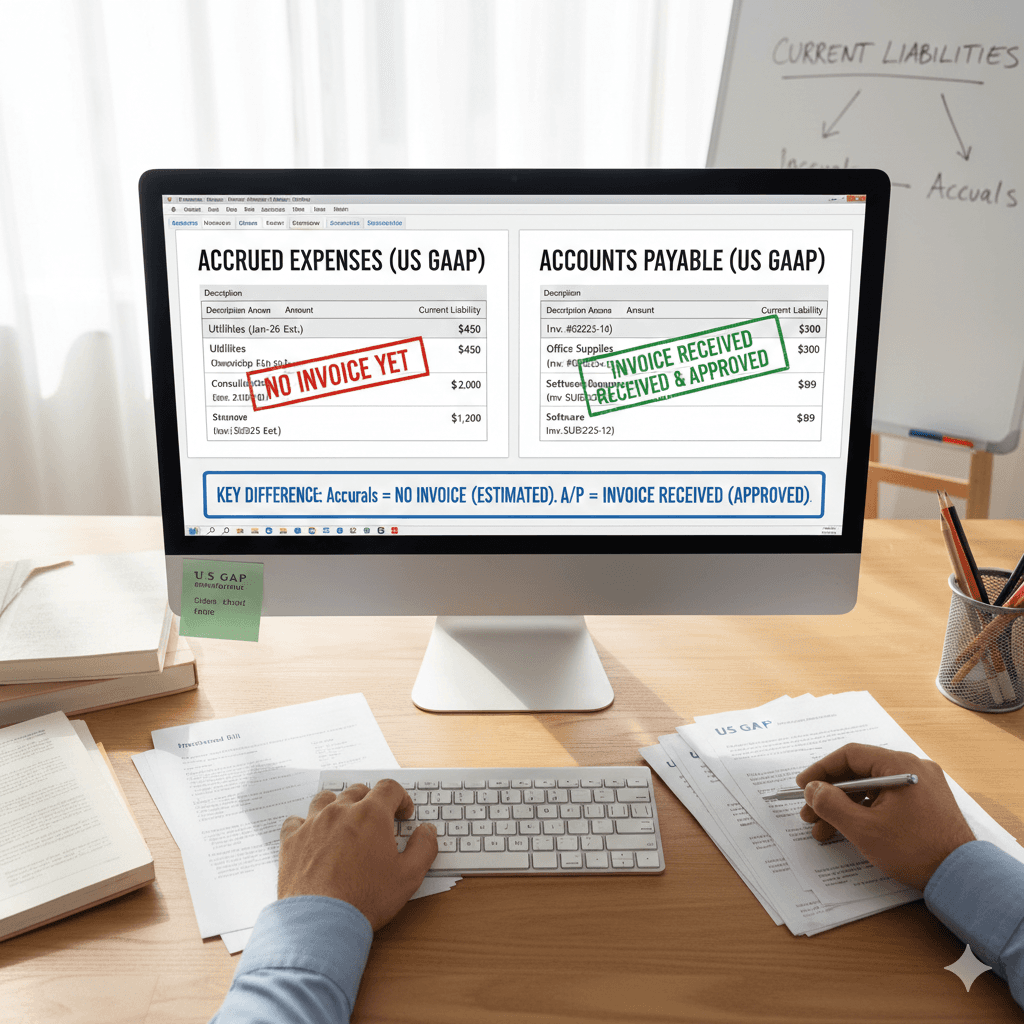

Distinction from Accounts Payable: Under US GAAP, accrued expenses are distinct from Accounts Payable (A/P). Accrued expenses are liabilities recognized without a vendor invoice being processed, based on estimation. A/P represents liabilities for goods or services received where the vendor invoice has been received and approved for payment. Both are classified as current liabilities if payment is due within one year or the operating cycle, whichever is longer.

Journal Entry (Under US GAAP):

To recognize the accrued expense:

Date | Account | Debit | Credit |

Period End | Expense Account (e.g., Salaries Expense) | XXX | |

Accrued Liability (e.g., Accrued Wages Payable) | XXX | ||

To record the expense incurred but not yet paid |

When the actual payment is made or the invoice is received:

Date | Account | Debit | Credit |

Subsequent Period | Accrued Liability (to remove the obligation) | XXX | |

Cash or Accounts Payable | XXX | ||

To settle the previously accrued liability |

.

2. The Core Accrual Decision Framework

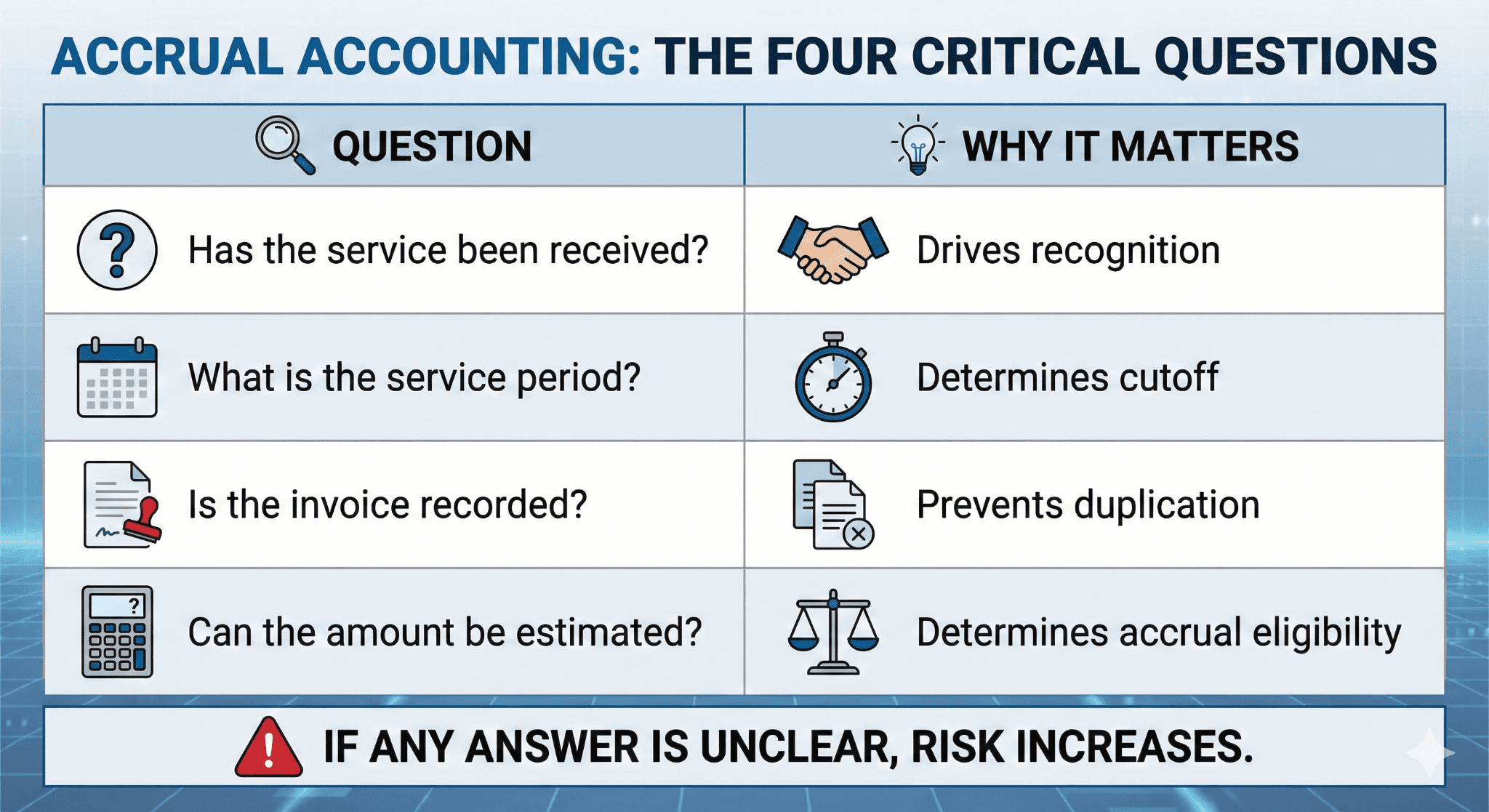

Before booking any accrual, the accountant must answer four questions.

Question | Why It Matters |

Has the service been received? | Drives recognition |

What is the service period? | Determines cutoff |

Is the invoice recorded? | Prevents duplication |

Can the amount be estimated? | Determines accrual eligibility |

If any answer is unclear, the risk increases.

3. Practical Case Studies: Invoice Timing and Month-End Cutoff

Case Study 1: Invoice Received Before Month-End, Service Extends Beyond

Scenario

Vendor invoice date: March 28

Invoice received: March 29

Service period: April 1 – April 30

Accounting period: March close

Common Mistake

Expense recorded in March because invoice was received before close.

Correct Treatment

Do not accrue. Do not expense. Record as prepaid or defer recognition.

Why

No service was received in March. Accrual criteria are not met.

Control Lesson

Invoice receipt date does not override service period.

Documentation Required

Invoice

Contract or service period confirmation

Accounting memo explaining deferral decision

Case Study 2: Invoice Received After Month-End, Service Fully in Prior Month

Scenario

Service period: March 1 – March 31

Invoice date: April 3

Invoice received: April 5

March close in progress

Correct Treatment

Accrue expense in March.

Journal Entry (March 31)

Debit: Expense

Credit: Accrued expenses

Reversal (April 1)

Debit: Accrued expenses

Credit: Expense

Why

Service was fully received in March. Invoice timing is irrelevant.

Documentation Required

Prior month contract or engagement letter

Estimation worksheet

Accrual JE support

Case Study 3: Invoice Received After Month-End, Partial Service Period

Scenario

Service period: March 15 – April 14

Invoice received: April 10

Total invoice: $3,000

Decision Required

Accrue only the portion related to March.

Calculation

March portion: 17 days

Total days: 31

Accrued amount: $1,645

Common Failure

Teams accrue full invoice or skip accrual entirely.

Control Requirement

Defined proration methodology documented in policy.

4. Service Period Ambiguity: Gray Areas That Break Controls

Case Study 4: Utilities with Estimated Usage

Scenario

Utility bill received April 12

Billing period: March 10 – April 9

Correct Accrual

Estimate March 10 – March 31 portion

Accrue based on prior usage trends

Documentation

Prior utility bills

Estimation logic

Calculation worksheet

Audit Expectation

Consistency over precision.

Case Study 5: Professional Fees Without Clear Time Sheets

Scenario

Legal firm invoice pending

Ongoing engagement

No time sheets received

Decision

Accrue based on engagement scope and historical billing.

Risk

Management bias if unsupported.

Mitigation

Engagement letter

Prior month invoices

Conservative estimation rule

5. When Not to Accrue: Over-Accrual Is Also a Control Failure

Case Study 6: Goods Not Yet Received

Scenario

Purchase order issued

No delivery as of month-end

No invoice received

Correct Treatment

Do not accrue.

Why

No service or goods received.

Common Error

Accruing based on PO alone.

Case Study 7: Invoice Recorded Before Close

Scenario

Invoice received March 31

Bill entered March 31

Payment pending

Correct Treatment

Do not accrue.

Why

Liability already recorded in accounts payable.

Control

Accrual checklist must confirm invoice posting status.

6. Accrual Documentation: What Auditors Actually Want

6.1 Minimum Accrual Support Package

Every accrual should have:

Document | Purpose |

Service evidence | Confirms receipt |

Calculation | Supports amount |

Policy reference | Consistency |

JE approval | Authorization |

Reversal link | Completeness |

Attachments must be stored in or referenced from QuickBooks.

7. Accrual Reversal and Clearing Controls in Practice

Case Study 8: Failure to Reverse Accrual

Scenario

March accrual booked

April invoice recorded

Accrual not reversed

Impact

Expense duplicated.

Control

Mandatory reversal entry dated first day of next period.

Case Study 9: Clearing Accrual Upon Invoice Receipt

Best Practice in QuickBooks

Record invoice to expense

Clear accrual via reversal

Tie invoice number in memo

Review Control

Monthly list of open accruals reviewed by controller.

8. Accrued Expense Rollforward: The Anchor Control

Case Study 10: Rollforward Prevents Material Misstatement

Scenario

Accrued expenses balance grew month over month

No rollforward performed

Control Added

Monthly rollforward showing:

Opening balance

New accruals

Reversals

Settlements

Outcome

$120,000 stale accrual identified before audit.

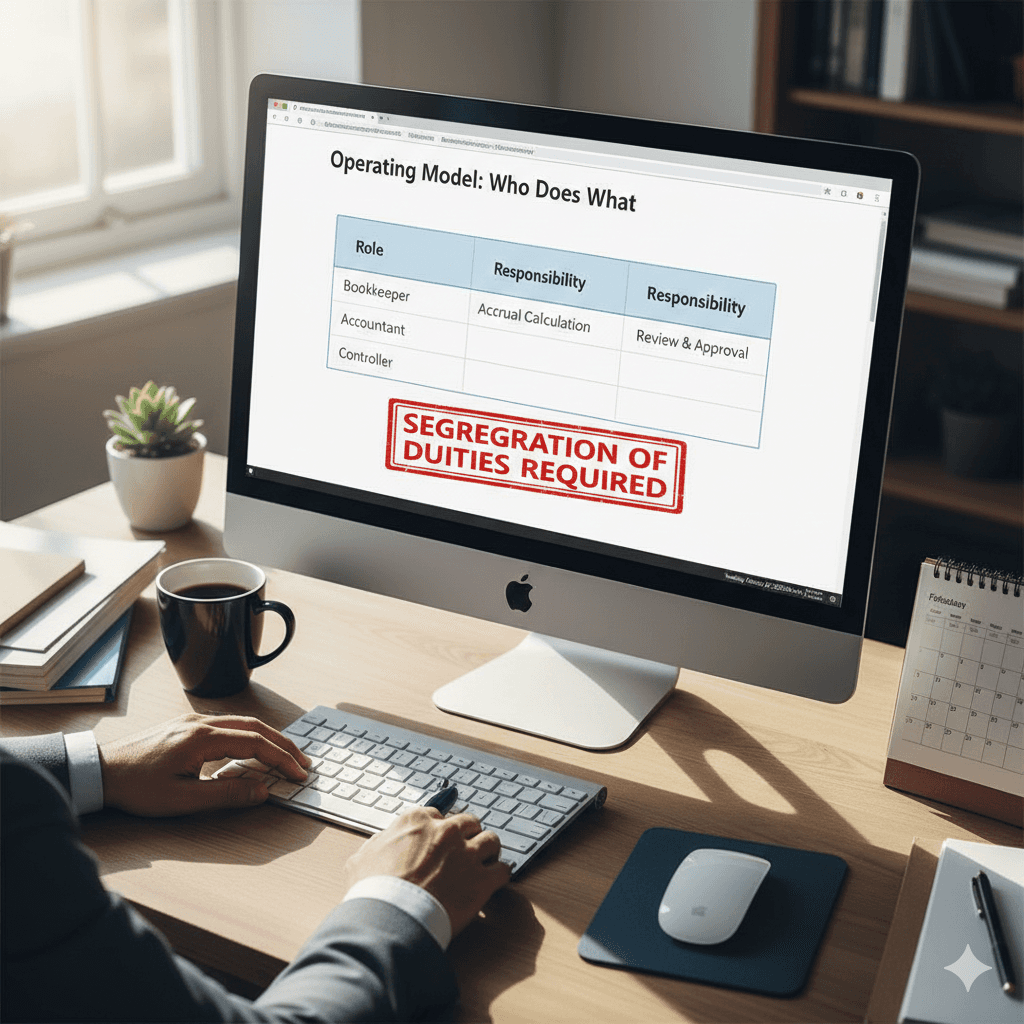

9. Operating Model: Who Does What

Role | Responsibility |

Bookkeeper | Data collection |

Accountant | Accrual calculation |

Controller | Review and approval |

Segregation of duties is required even in small teams.

Tool and Workflow Comparison

Method | Risk Level | Audit Outcome |

Memory-based accruals | High | Weak |

Checklist-driven accruals | Medium | Acceptable |

FinBoard.ai module | Low | Strong |

Risks and Mitigations

Risk | Mitigation |

Invoice timing confusion | Service-period rule |

Estimation bias | Standard formulas |

Missed reversals | Mandatory auto-JE |

Weak evidence | Documentation pack |

FAQ

Is invoice date ever relevant?

Only for AP aging, not expense recognition.

Can accruals be immaterial?

Yes, based on defined thresholds.

Are emails sufficient support?

Only if retained and referenced.

Do accruals need approval?

Yes. They are judgmental entries.

Should accruals reverse automatically?

Yes, unless settled before reversal.

Glossary

Accrued Expense: Liability for incurred costs not yet invoiced.

Service Period: Time during which benefit is received.

Cutoff: Correct period recognition.

Rollforward: Balance movement analysis.

Reversal: Entry negating prior accrual.