Employee benefit liabilities behave like short-term credit exposure.

Obligations arise before payment and require estimation.

QuickBooks Online records transactions, not expected obligations.

CECL-style thinking improves accrual accuracy, predictability, and audit outcomes.

This is not CECL compliance. It is CECL discipline applied to benefits.

Executive Summary

Most accounting teams treat employee benefits as a payroll byproduct. Payroll runs. Entries post. Vendors get paid. End of story. That approach works only when timing, headcount, and benefit structures remain static. The moment any of those variables change, benefit accounting becomes noisy, unpredictable, and difficult to defend.

US GAAP does not allow benefit obligations to float between periods based on convenience. Expenses must follow service periods. Liabilities must reflect obligations incurred but not yet settled. Estimation is not optional.

This is where a CECL-style mindset becomes useful.

CECL, at its core, is about recognizing expected outcomes early, using reasonable information available today. That same discipline applies directly to employee benefit liabilities. Benefits are earned before they are paid. The amount is often known approximately but not precisely. Timing differences introduce risk. Ignoring that risk creates distortions.

This article reframes employee benefit accounting using CECL principles. It explains how to identify benefit exposure, estimate expected obligations, update assumptions, and document judgments in a way that aligns with US GAAP and works in QuickBooks Online Online environments.

Why CECL Thinking Belongs in Benefit Accounting

CECL did not invent estimation. It formalized a mindset that good accountants already use.

The mindset asks:

What obligation exists today?

What do we reasonably expect to pay?

What information should influence that estimate?

How often should the estimate change?

Employee benefit liabilities meet all four criteria.

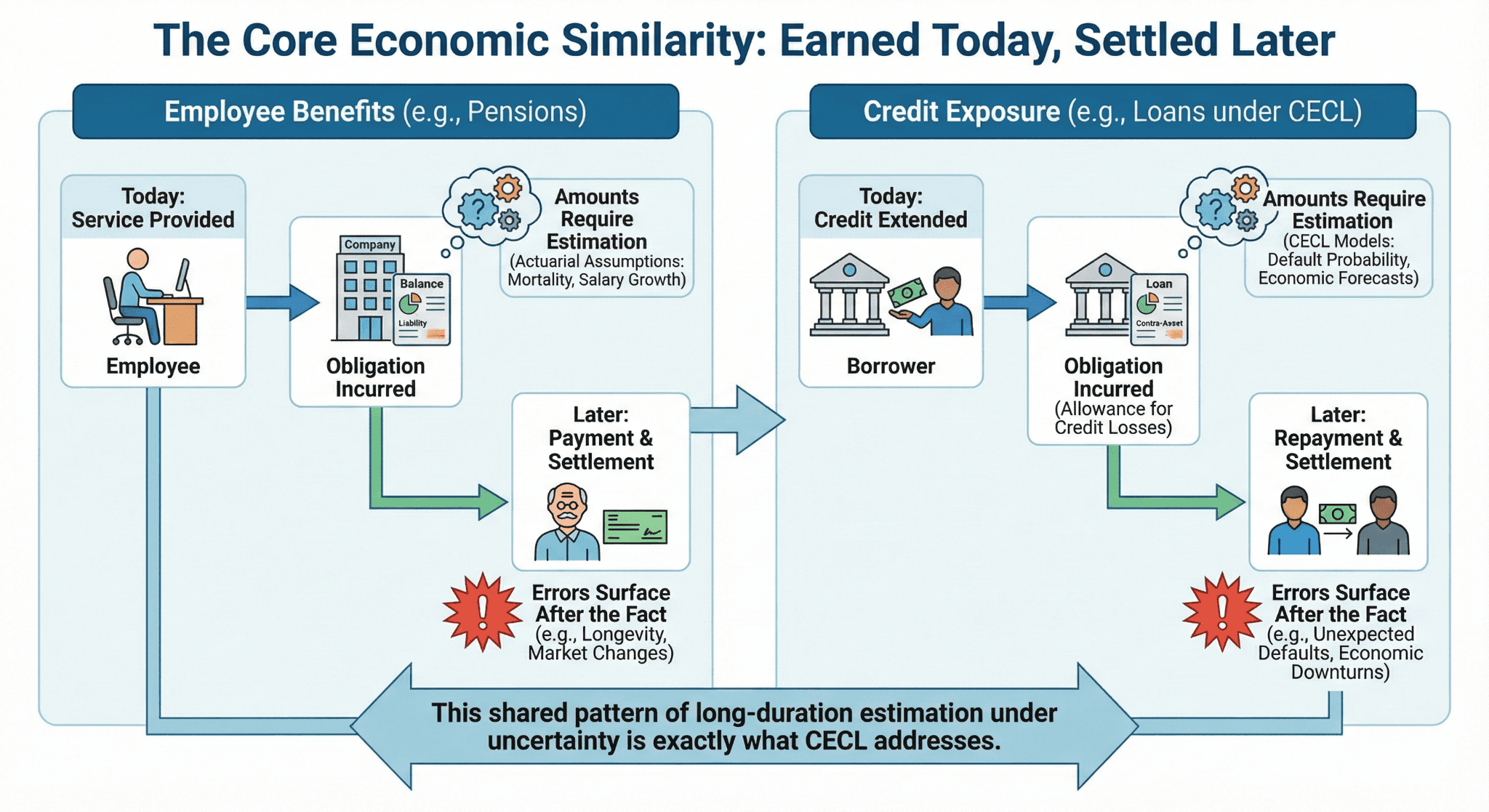

The Core Similarity: Earned Today, Settled Later

Employee benefits share the same economic structure as credit exposure.

Employees provide service today.

The company incurs an obligation today.

Payment happens later.

Amounts require estimation.

Errors surface after the fact.

This is exactly the pattern CECL addresses.

Traditional Benefit Accounting: The Incurred Model

Most QuickBooks Online users operate on an incurred-only model.

Characteristics:

Expense recorded on payroll date

Vendor bills expensed when paid

Accruals limited or nonexistent

Adjustments reactive, not planned

CECL-Style Benefit Accounting: The Expected Model

A CECL-style approach reframes the workflow.

Characteristics:

Identify benefit exposure continuously

Estimate employer obligation monthly

Recognize expense before payment

Update estimates as conditions change

Reconcile estimates to actuals

The difference is not accounting mechanics. It is timing discipline.

Mapping CECL Framework to Benefit Liabilities

CECL Component | Benefit Accounting Equivalent |

Financial asset | Earned benefit obligation |

Credit exposure | Employee service rendered |

Expected loss | Expected employer benefit cost |

Historical loss data | Prior benefit cost experience |

Current conditions | Headcount, payroll, plan terms |

Reasonable forecast | Hiring plans, benefit changes |

Allowance | Accrued benefit liability |

This mapping is not theoretical. It mirrors how auditors already think.

Identifying Benefit Exposure Pools

CECL requires segmentation. Benefits should be segmented too.

Common Benefit Exposure Pools

Health Insurance

Monthly premiums

Coverage-based

Often paid after coverage period

Retirement Match

Payroll-based

Earned when payroll is earned

Paid later, sometimes quarterly

Employer Payroll Taxes

Statutory

Accrue with wages

True-ups common

Life and Disability Insurance

Flat or tiered premiums

Coverage timing matters

Bonuses and Incentives

Service-based

Payment timing varies

Each pool has different estimation risk.

GAAP Foundation: What the Standards Actually Require

US GAAP does not require CECL for benefits. It does require:

Accrual accounting

Expense recognition when incurred

Reasonable estimation of liabilities

Consistent application of accounting policies

Relevant guidance includes:

ASC 710 (Compensation)

ASC 450 (Contingencies)

ASC 275 (Risks and uncertainties)

Together, they require recognition of obligations that are probable and reasonably estimable.

Employee benefits almost always meet that threshold.

Where Benefit Risk Actually Comes From

Benefit risk is not abstract. It is operational.

Primary drivers:

Payroll timing shifts

Mid-month hires and terminations

Waiting periods

Benefit elections changes

Vendor invoice delays

Manual overrides in payroll

Each introduces estimation error if not anticipated.

Case Scenario 1: Rapid Hiring and Under-Accrued Insurance

Company Profile

Marketing agency. 120 employees. QuickBooks Online Online Payroll.

Situation

Aggressive hiring over six months. Health insurance premiums billed monthly in arrears.

Traditional Treatment

Insurance expensed when bill paid.

Result

Monthly expenses lagged headcount growth. EBITDA looked inflated. Year-end audit proposed a large catch-up.

CECL-Style Fix

Estimated monthly employer insurance cost based on enrolled headcount at month-end. Accrued expected obligation regardless of invoice timing.

Outcome

Expenses aligned with service periods. Audit adjustment eliminated.

Case Scenario 2: Retirement Match Lag and Double Counting

Company Profile

Professional services firm. 80 employees.

Situation

Retirement match calculated with payroll but paid quarterly.

Problem

Payroll posted expense. Quarterly payment expensed again.

Root Cause

No liability tracking. Payment treated as new expense.

CECL-Style Fix

Payroll posted expense and liability. Quarterly payment cleared liability only.

Outcome

Eliminated duplicate expense. Clean liability rollforward.

Case Scenario 3: Headcount Reduction and Over-Accrued Benefits

Company Profile

SaaS startup. Workforce reduction mid-quarter.

Traditional Behavior

Continued accruing benefits based on prior headcount.

Issue

Over-accrued insurance and retirement benefits.

CECL-Style Update

Updated estimate based on reduced headcount and coverage end dates.

Outcome

Accruals reversed promptly. No surprise reversals later.

Estimation Techniques That Work in Practice

CECL does not require complexity. Benefits do not either.

Acceptable Estimation Methods

Per-employee monthly cost

Fixed premium per covered life

Percentage of payroll for retirement match

Blended historical average adjusted for forecast changes

What matters is consistency and rationale.

Incorporating Forward-Looking Information

CECL explicitly requires forward-looking consideration. Benefits should too.

Examples of reasonable forward-looking inputs:

Approved hiring plans

Known premium increases

Planned layoffs

Benefit plan changes

Contractual rate escalations

Ignoring known information is not conservative. It is inaccurate.

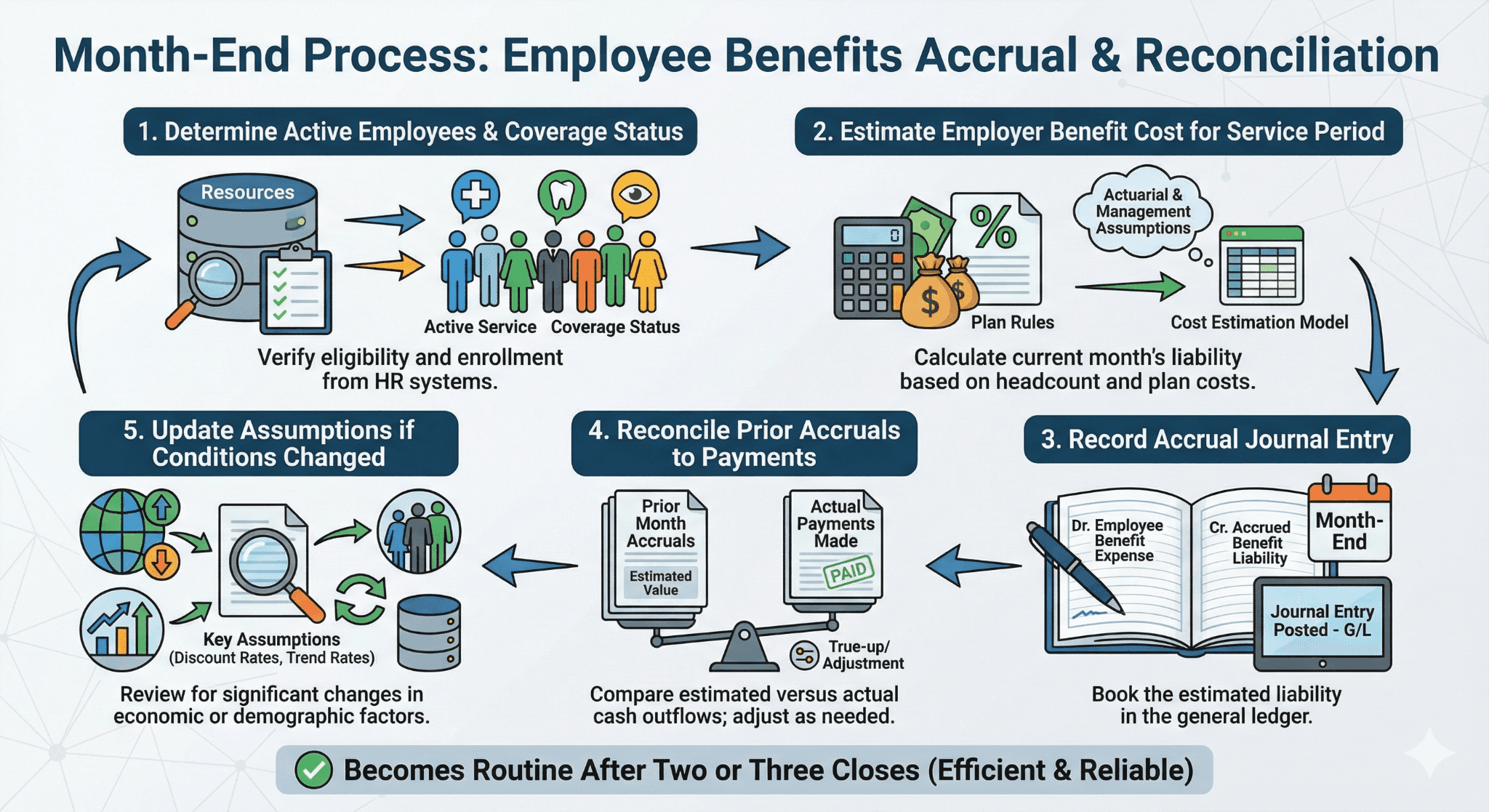

How This Works Month-End in QuickBooks Online

QuickBooks Online will not do this automatically. The workflow is manual but manageable.

Month-End Process

Determine active employees and coverage status.

Estimate employer benefit cost for the service period.

Record accrual journal entry.

Reconcile prior accruals to payments.

Update assumptions if conditions changed.

This becomes routine after two or three closes.

Journal Entries Explained

Accrual Entry

Debit: Benefit Expense

Credit: Accrued Benefit Liability

Payment Entry

Debit: Accrued Benefit Liability

Credit: Cash or Accounts Payable

No expense on payment if already accrued.

Reconciliation: The Control That Makes This Work

Each benefit pool should reconcile monthly.

Reconciliation structure:

Opening liability

Plus current period accrual

Minus payments

Equals closing liability

Unexplained differences indicate process failure.

Documentation: Turning Judgment Into Defense

Auditors do not reject estimates. They reject undocumented estimates.

Document:

Estimation methodology

Data sources

Update triggers

Review and approval

This converts judgment into policy.

Case Scenario 4: Private Equity Due Diligence

Company Profile

PE-backed manufacturing firm.

Issue Identified in QoE

Benefit accruals inconsistent and undocumented.

Impact

Normalized EBITDA adjustment proposed.

Remediation

Implemented CECL-style benefit accrual framework with documentation.

Result

Adjustment removed. Valuation preserved.

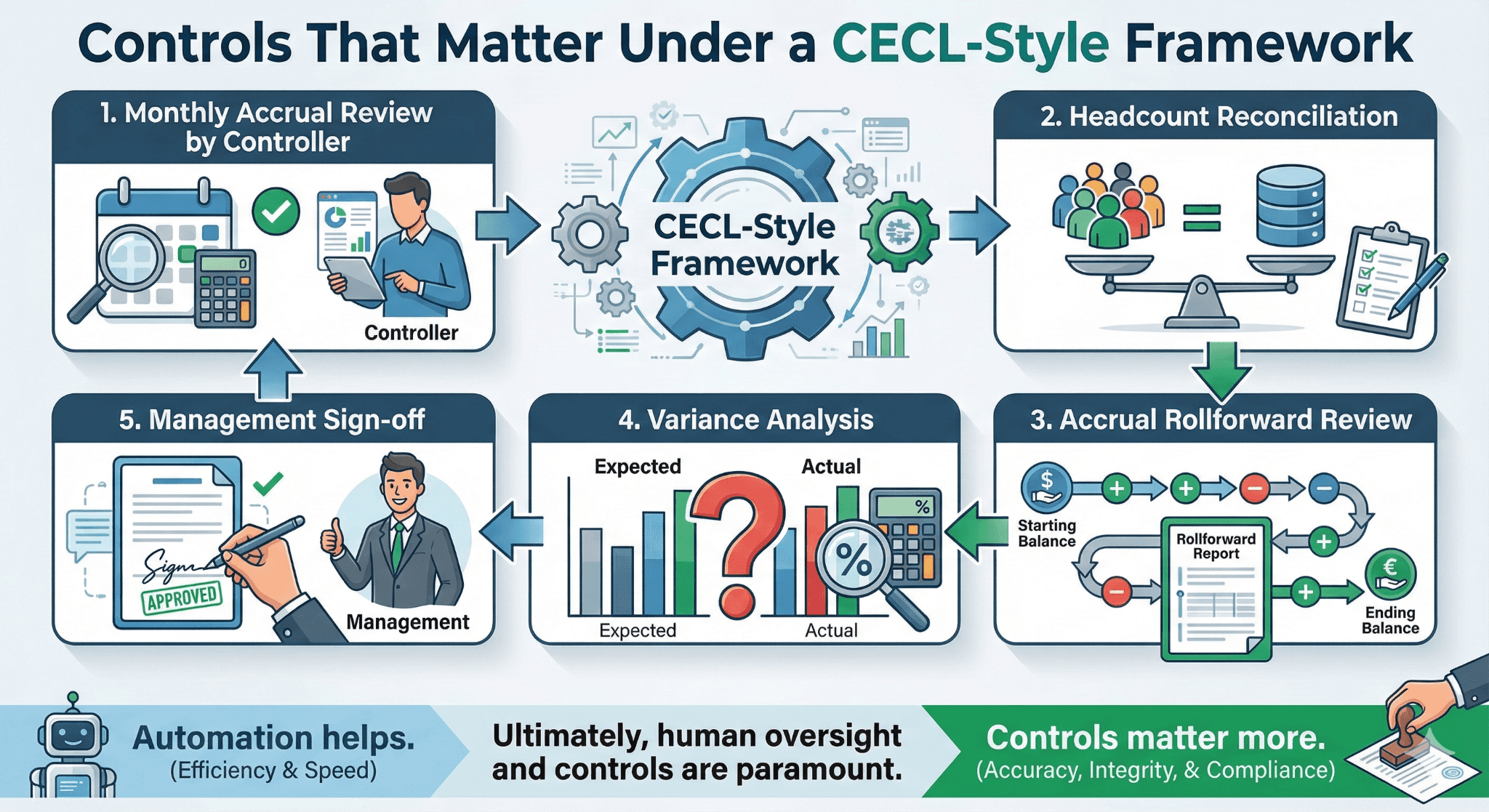

Controls That Matter Under a CECL-Style Framework

Key controls include:

Monthly accrual review by controller

Headcount reconciliation

Accrual rollforward review

Variance analysis

Management sign-off

Automation helps. Controls matter more.

Common Pushback and Practical Responses

“This is too complex.”

It replaces chaos with routine.

“Amounts are not material.”

Materiality changes quickly with growth.

“QuickBooks Online payroll already handles benefits.”

Payroll handles processing, not estimation.

Audit Perspective

Auditors increasingly expect:

Accrual methodology

Forward-looking consideration

Consistent application

Reconciliation support

They may not say “CECL,” but the logic is the same.

Tool Comparison: Incurred vs Expected

Approach | Predictability | Accuracy | Audit Risk |

Cash-based | Low | Low | High |

Incurred accrual | Medium | Medium | Medium |

CECL-style | High | High | Low |

When This Framework Is Most Valuable

Rapid growth or contraction

Material benefit costs

EBITDA-focused stakeholders

Recurring audits

Investor reporting

Stable, cash-basis entities feel less impact. Everyone else benefits.

Frequently Asked Questions

Is this required by GAAP?

The accrual is required. The mindset enables compliance.

Is this CECL compliance?

No. It is CECL-style reasoning.

Does this replace payroll accounting?

No. It complements payroll.

Can QuickBooks Online automate this?

Not fully. Judgment remains essential.

Will auditors support this?

Yes, when applied consistently and documented.

Glossary

Expected Obligation

Estimated benefit cost earned but unpaid.

Exposure Pool

Group of similar benefit liabilities.

Forward-Looking Adjustment

Estimate change based on known future conditions.

Accrued Benefit Liability

Balance sheet account representing expected obligation.