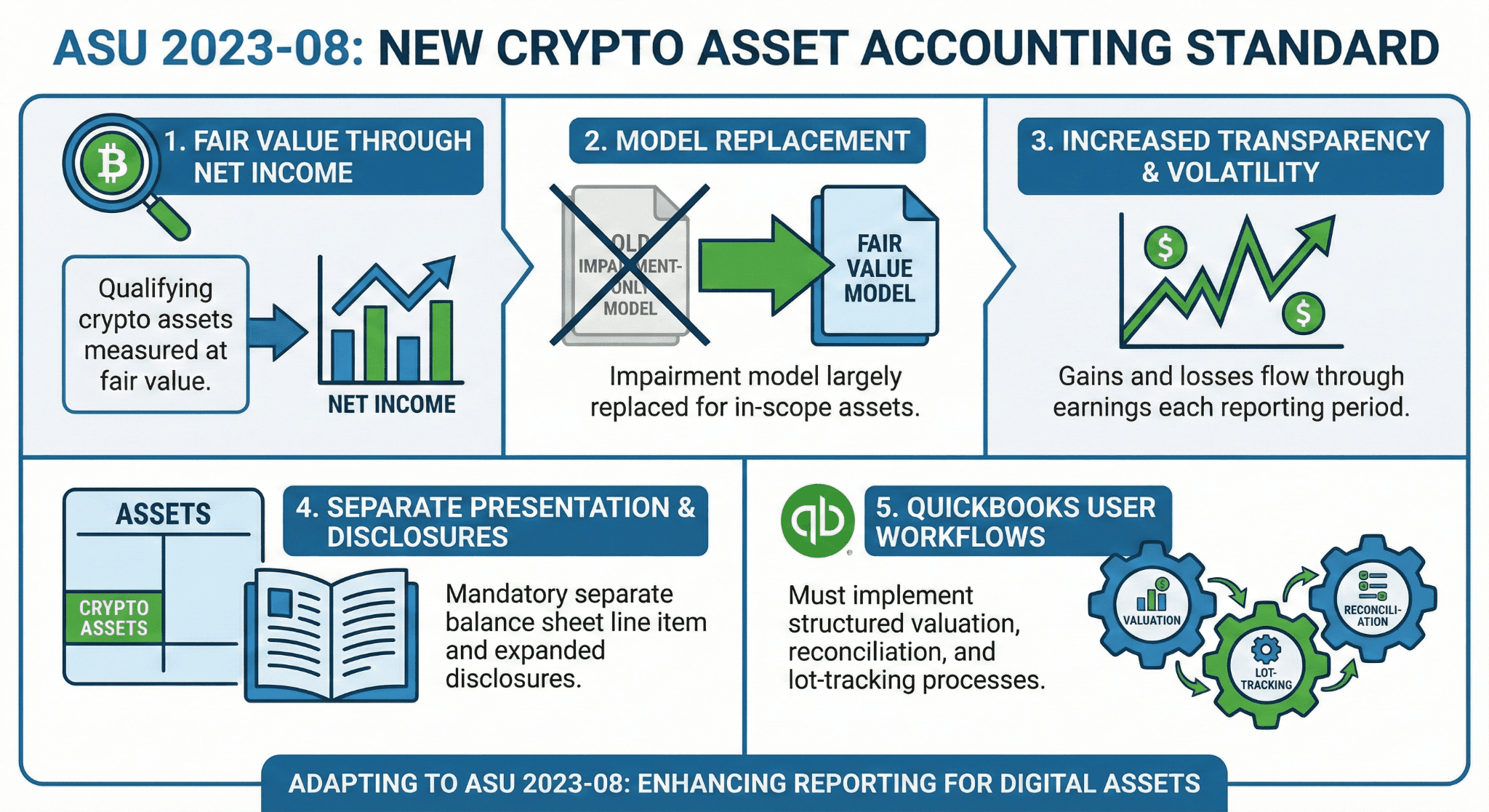

ASU 2023-08 requires qualifying crypto assets to be measured at fair value through net income.

The old impairment-only intangible model is largely replaced for in-scope crypto assets.

Gains and losses now flow through earnings each reporting period, increasing transparency and volatility.

Separate balance sheet presentation and expanded disclosures are mandatory.

QuickBooks Online users must implement structured valuation, reconciliation, and lot-tracking workflows.

Executive Summary

Cryptocurrency accounting under U.S. GAAP changed materially with the issuance of Accounting Standards Update (ASU) 2023-08 by the Financial Accounting Standards Board in December 2023. The update requires most qualifying crypto assets to be measured at fair value, with changes recognized in net income each reporting period.

Before this update, crypto assets were typically accounted for as indefinite-lived intangible assets under ASC 350, subject to impairment testing. That model allowed downward write-downs but prohibited upward reversals. Many preparers and investors criticized the asymmetry because it did not reflect economic performance.

ASU 2023-08 improves relevance and comparability. It applies to fiscal years beginning after December 15, 2024, including interim periods, with early adoption permitted.

For SMB and mid-market entities, the accounting principles are clear. The challenge lies in implementation: valuation methodology, wallet reconciliation, gain tracking, internal controls, and disclosure. This guide explains the rules and provides practical case scenarios tailored for QuickBooks-Online heavy environments.

1. Classification and Scope under US GAAP

1.1 When Does ASU 2023-08 Apply?

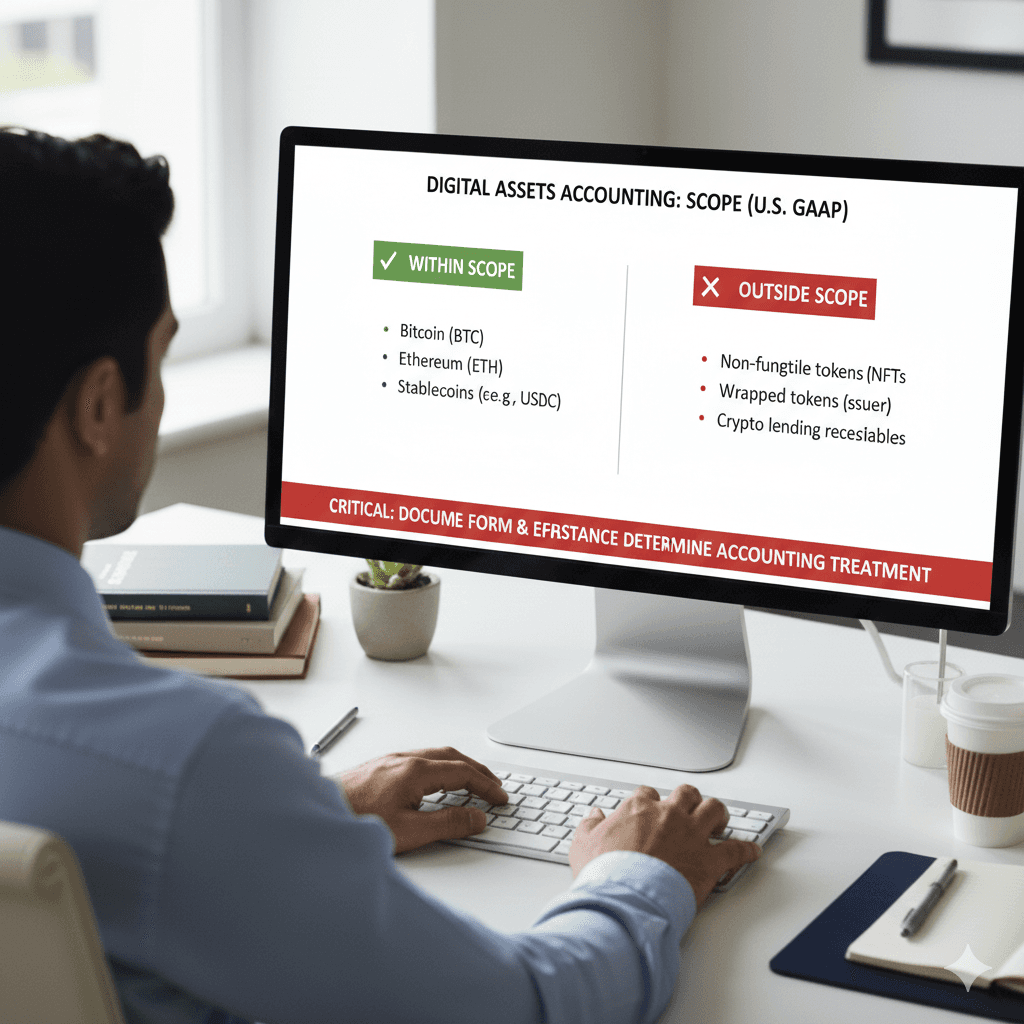

ASU 2023-08 applies to crypto assets that meet all of the following criteria: [1]

Meet the definition of an intangible asset.

Are created or reside on a distributed ledger.

Are secured through cryptography.

Are fungible (interchangeable units).

Are not issued by the reporting entity or related parties.

Examples Within Scope

Bitcoin (BTC)

Ethereum (ETH)

Stablecoins such as USDC, if criteria are met

Examples Outside Scope

Non-fungible tokens (NFTs)

Wrapped tokens issued by the reporting entity

Crypto lending receivables

Crypto assets are not cash because they are not legal tender. They are not financial instruments because they do not represent a contractual right to receive cash.

1.2 Balance Sheet Classification

Crypto assets must be presented separately from other intangible assets on the balance sheet.

Example presentation:

Asset Category | Amount |

Cash and Cash Equivalents | 500,000 |

Accounts Receivable | 320,000 |

Crypto Assets (Fair Value) | 140,000 |

Property and Equipment | 1,200,000 |

This separate presentation improves transparency and investor understanding.

2. Transition from Impairment Model to Fair Value Model

Before ASU 2023-08, crypto was generally accounted for under the indefinite-lived intangible asset model (ASC 350).

2.1 Old Model (Canonical – AICPA Practice Aid)

Initially recorded at cost.

Tested for impairment if fair value fell below carrying value.

Impairment losses recognized in earnings.

No upward reversals permitted.

This created distorted earnings. If Bitcoin dropped in Q1 and recovered in Q2, the recovery was ignored.

2.2 New Fair Value Model under ASU 2023-08

Under the new guidance: [1]

Crypto assets are measured at fair value at each reporting date.

Changes in fair value are recognized in net income.

Impairment testing is eliminated for qualifying assets.

Comparison Table

3. Practical Case Scenarios — Step-by-Step Accounting

Scenario 1: Purchasing Crypto for Investment

Facts

On March 1, Company A purchases 5 BTC at 30,000 each. Total cost: 150,000.

Initial Entry

Debit Crypto Assets 150,000

Credit Cash 150,000

At March 31, BTC trades at 34,000.

Fair value = 170,000

Gain = 20,000

Fair Value Adjustment

Debit Crypto Assets 20,000

Credit Unrealized Gain on Crypto 20,000

If at April 30 BTC falls to 28,000:

Fair value = 140,000

Loss = 30,000 from prior carrying value.

Debit Unrealized Loss on Crypto 30,000

Credit Crypto Assets 30,000

Under ASU 2023-08, both gains and losses flow through net income. [1]

Scenario 2: Accepting Crypto as Customer Payment

Facts

An agency invoices a client for 50,000. The client pays in Ethereum. ETH fair value at payment date equals 50,000.

Revenue Recognition

Revenue is recognized at fair value on receipt date. [6]

Debit Crypto Assets 50,000

Credit Revenue 50,000

At month end, ETH value increases to 55,000.

Debit Crypto Assets 5,000

Credit Unrealized Gain 5,000

If ETH later drops before conversion, losses must be recorded.

Key Control

Valuation must use a consistent principal market exchange. [1]

Scenario 3: Month-End Close — Multiple Lots

Company B holds:

Purchase Date | Units | Cost per Unit | Cost |

Jan 10 | 2 BTC | 28,000 | 56,000 |

Feb 5 | 1 BTC | 32,000 | 32,000 |

Total cost = 88,000.

March 31 fair value per BTC = 35,000.

Total fair value = 105,000.

Carrying amount prior = 88,000.

Adjustment = 17,000 gain.

Debit Crypto Assets 17,000

Credit Unrealized Gain 17,000

Lot tracking remains relevant for tax but not for GAAP fair value measurement.

Scenario 4: Selling Crypto Mid-Period

Company sells 1 BTC when market price is 36,000.

Carrying value per BTC at last valuation = 35,000.

Realized gain = 1,000.

Debit Cash 36,000

Credit Crypto Assets 35,000

Credit Realized Gain 1,000

Remaining crypto continues to be measured at fair value.

Scenario 5: Stablecoin Holdings (USDC)

Many SMBs hold stablecoins for operational liquidity.

If USDC trades at 1.00, minimal fair value adjustment occurs. However, if de-pegging occurs, fair value changes must be recognized immediately.

Example: USDC falls to 0.98 temporarily.

Holding: 100,000 USDC

Loss = 2,000

Debit Unrealized Loss 2,000

Credit Crypto Assets 2,000

Stablecoin risk is often underestimated.

Scenario 6: Impairment Model Legacy Transition

If transitioning from impairment model to fair value model, cumulative-effect adjustment may be required at adoption.

Example: Carrying amount under old model = 80,000

Fair value at adoption date = 100,000

Adjustment = 20,000 increase to retained earnings.

Debit Crypto Assets 20,000

Credit Retained Earnings 20,000

4. Disclosure Requirements

Entities must disclose:

Name of crypto assets held

Cost basis

Fair value

Gains and losses recognized

Restrictions on sale

Method of determining fair value

Sample Disclosure Table

Crypto Asset | Units Held | Cost Basis | Fair Value | Gain/(Loss) |

Transparency is a key objective of the update.

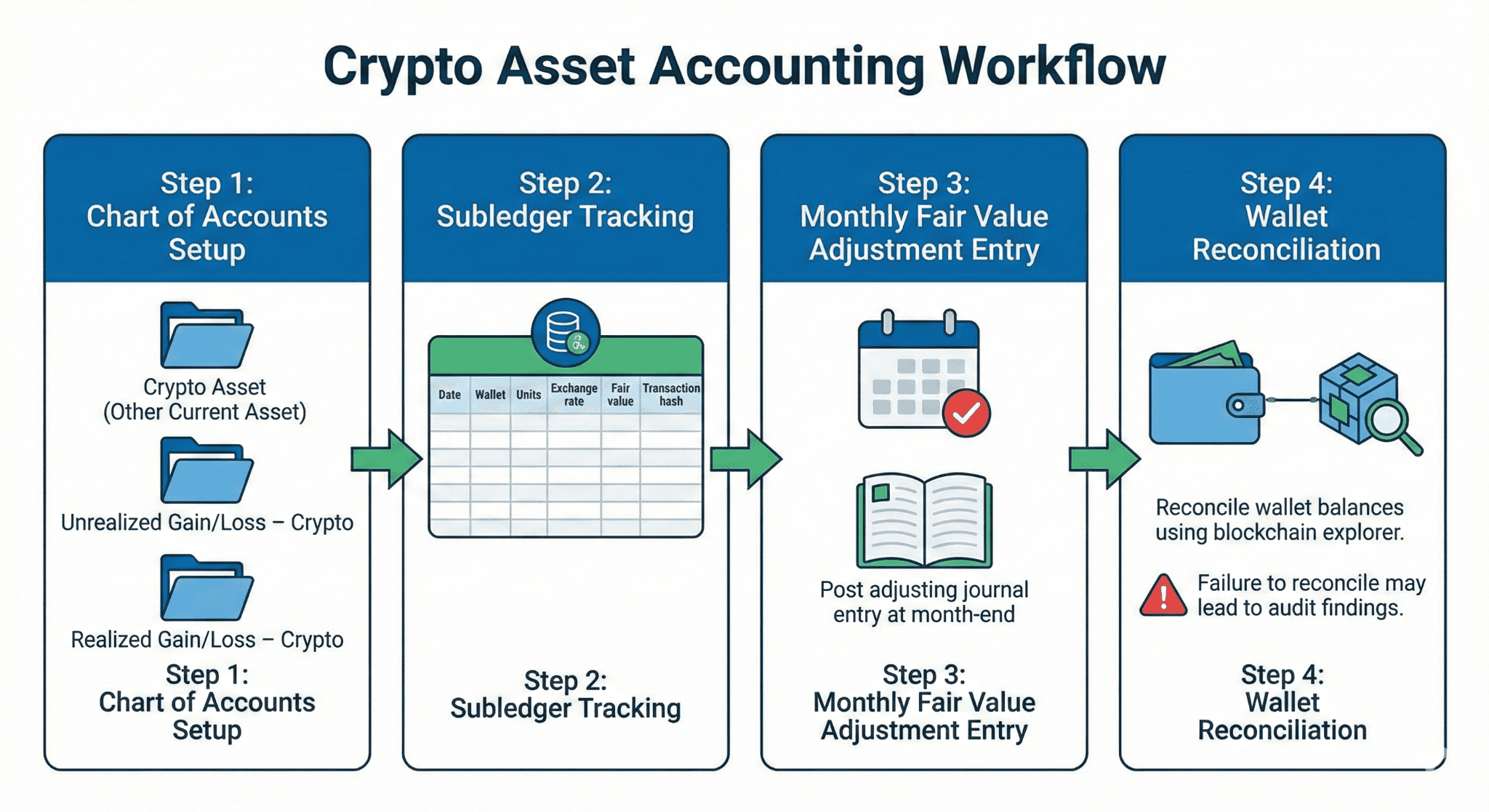

5. QuickBooks Online Implementation Guide

QuickBooks Online does not provide built-in crypto modules. Intuit guidance suggests creating “Other Current Asset” accounts. [4][7]

Step 1: Chart of Accounts Setup

Crypto Asset (Other Current Asset)

Unrealized Gain/Loss – Crypto

Realized Gain/Loss – Crypto

Step 2: Subledger Tracking

Maintain spreadsheet with:

Date

Wallet

Units

Exchange rate

Fair value

Transaction hash

Step 3: Monthly Fair Value Adjustment Entry

Post adjusting journal entry at month-end.

Step 4: Wallet Reconciliation

Reconcile wallet balances using blockchain explorer.

Failure to reconcile may lead to audit findings.

6. Internal Controls and Custody

Crypto presents unique custody risk.

EY emphasizes need for: [9]

Multi-signature wallets

Segregation of duties

Access approval matrix

Independent reconciliation

Cold storage for material balances

Control Matrix Example

Risk | Control | Frequency |

Unauthorized transfer | Multi-sig wallet | Ongoing |

Incorrect valuation | Independent review | Monthly |

Lost private key | Backup key storage | Annual test |

7. Tax vs GAAP Differences

IRS guidance treats crypto as property for tax purposes.

Key differences:

Area | GAAP | Tax |

Measurement | Fair value | Realization-based |

Unrealized gains | Recognized | Not taxed |

Lot selection | Not critical | Critical |

Deferred tax accounting may arise.

Tool / Workflow Comparison

Approach | Remarks |

Manual QuickBooks + Spreadsheet | Low cost |

Crypto Accounting Software Integration | Automated feeds |

FinBoard.ai digital Asset Module | Strong controls |

Additional Practical Scenarios

Scenario 8: Crypto Paid to Vendor

Company pays 0.5 BTC for equipment when BTC equals 40,000.

Debit Equipment 20,000

Credit Crypto Assets 20,000

If carrying value differs, recognize gain/loss.

Scenario 9: Crypto Held in Custody on Exchange

Assets held on exchange remain company assets if ownership retained.

No receivable classification unless legal control lost.

Scenario 10: Crypto Staking Income

If rewards received, recognize income at fair value upon receipt.

Debit Crypto Assets 3,000

Credit Staking Revenue 3,000

Subsequent fair value adjustments follow normal rules.

Risks and Mitigations

Risk | Impact | Mitigation |

Earnings volatility | High | Board communication |

Valuation inconsistency | Moderate | Policy selection |

Weak custody | Severe | Multi-layer security |

Regulatory change | Ongoing | Monitor FASB updates |

FAQ

1. Is crypto treated as cash?

No. It is an intangible asset.

2. When does ASU 2023-08 apply?

Fiscal years beginning after December 15, 2024.

3. Do unrealized gains hit OCI?

No. They hit net income.

4. Are NFTs included?

No. They are excluded from scope.

5. How often must fair value be measured?

At each reporting date.

Glossary

ASU 2023-08: FASB update requiring fair value measurement for qualifying crypto assets.

Distributed Ledger: Decentralized blockchain database.

Fair Value: Exit price in orderly transaction.

Fungible: Interchangeable units.

Principal Market: Market with greatest volume and activity.

Staking: Earning rewards for validating blockchain transactions.