Executive Summary

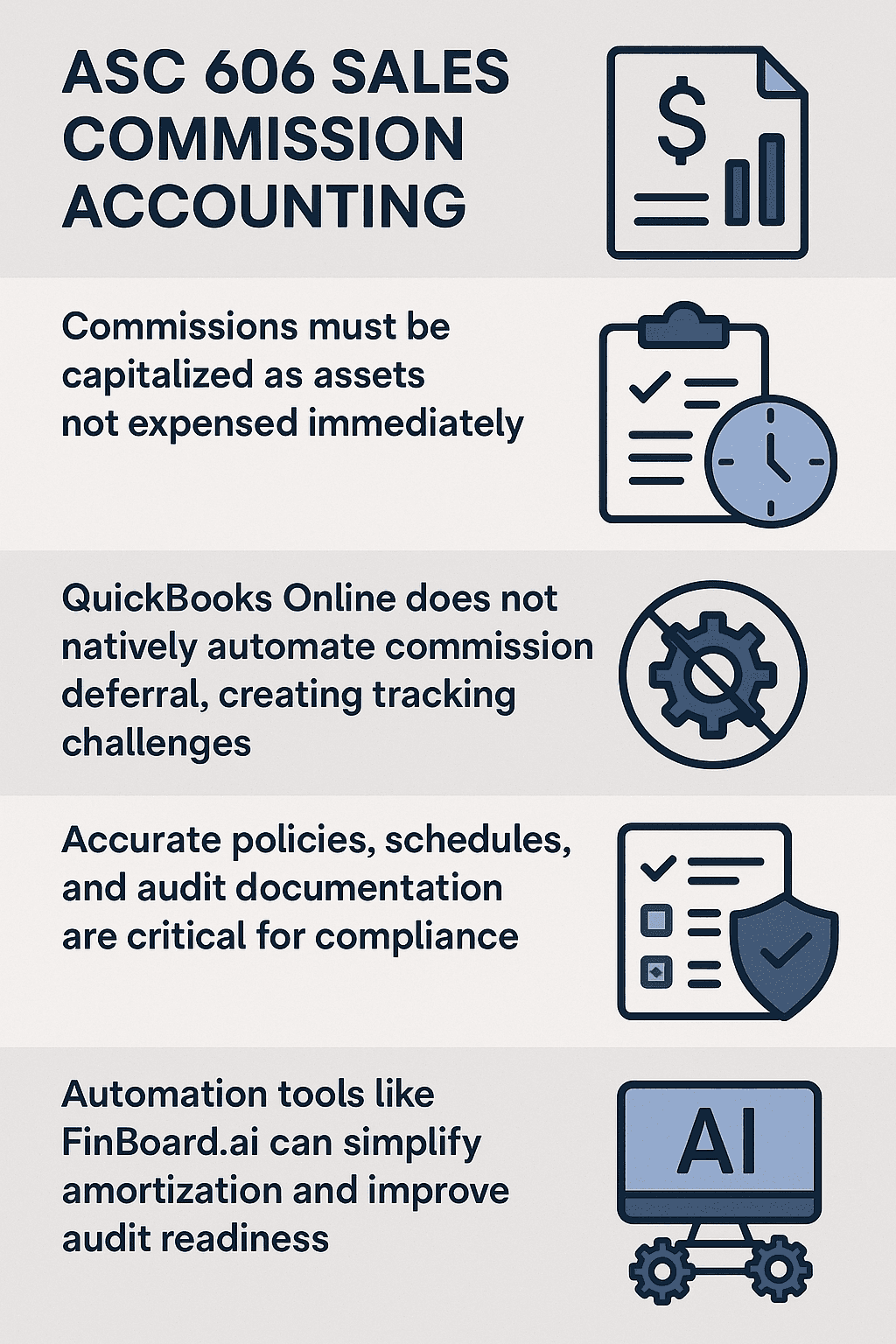

Sales commissions are often the largest variable expense in revenue-driven businesses. With the adoption of ASC 606 (Revenue from Contracts with Customers), these commissions can no longer be immediately expensed. Instead, companies must capitalize qualifying commissions as deferred contract costs and amortize them systematically over the life of the contract or expected customer relationship.

This shift improves financial accuracy and aligns expenses with revenue recognition. However, it also creates operational complexity. Many small and mid-sized businesses rely on QuickBooks Online, which does not provide native workflows for deferring commissions. Tracking manually through spreadsheets is prone to errors, particularly when dealing with multi-year contracts, renewals, or modifications.

In this article, we explain what deferred commissions are, why they matter under ASC 606, how to calculate and record them, common pitfalls, and how accountants using QuickBooks Online can design practical workflows. We also explore automation options, provide a SaaS-specific mini-case, and outline risks and mitigation strategies to stay compliant and audit-ready.

What Are Deferred Commissions under ASC 606?

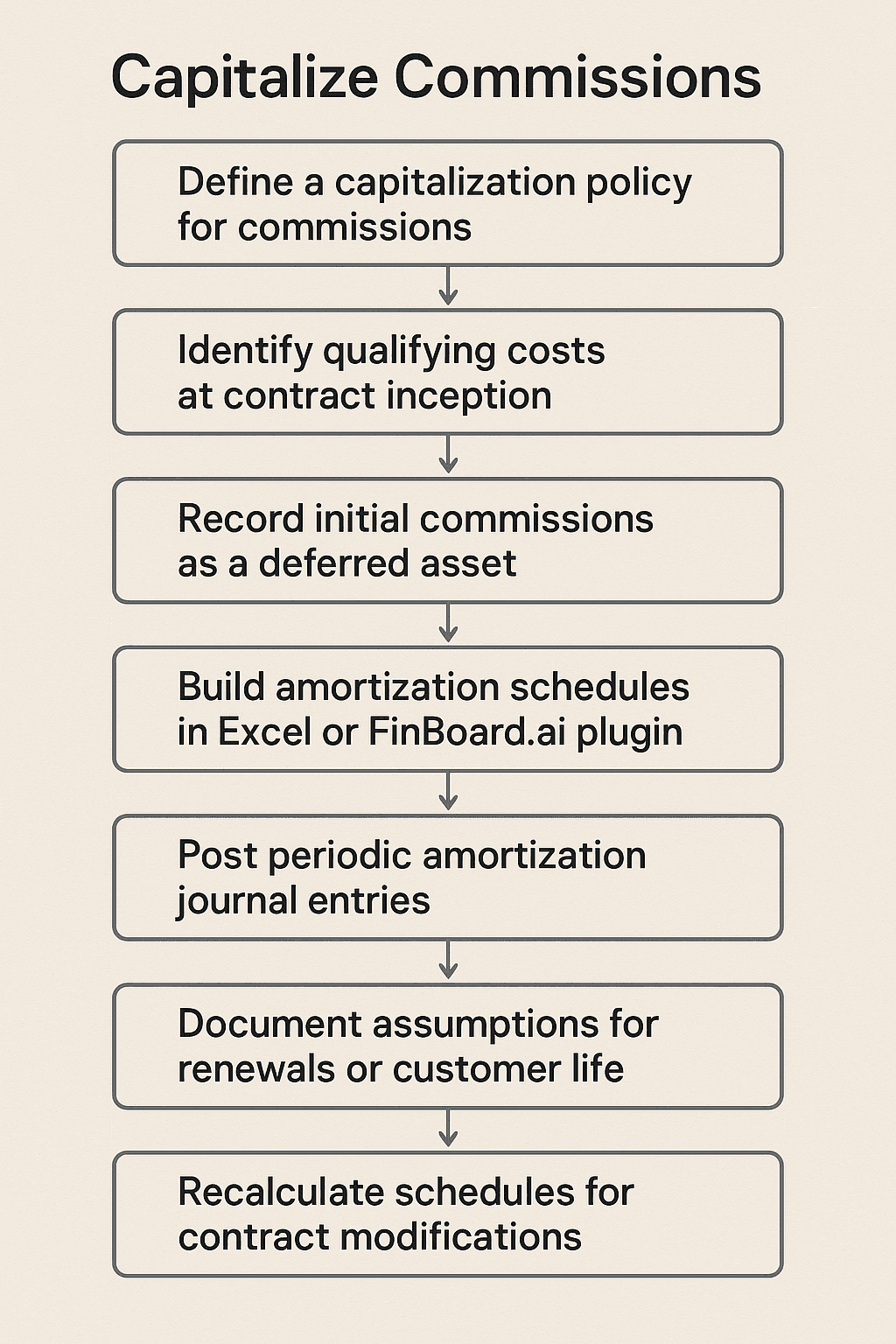

Deferred commissions represent incremental costs of obtaining a contract that must be capitalized as an asset and amortized over time.

Key Rules [1]:

Only direct costs tied to contract acquisition (e.g., sales commissions) qualify.

General marketing or indirect payroll costs do not qualify.

The amortization period is either the contract term or the anticipated customer life.

Example:

Contract: $180,000 over three years

Commission paid: $15,000

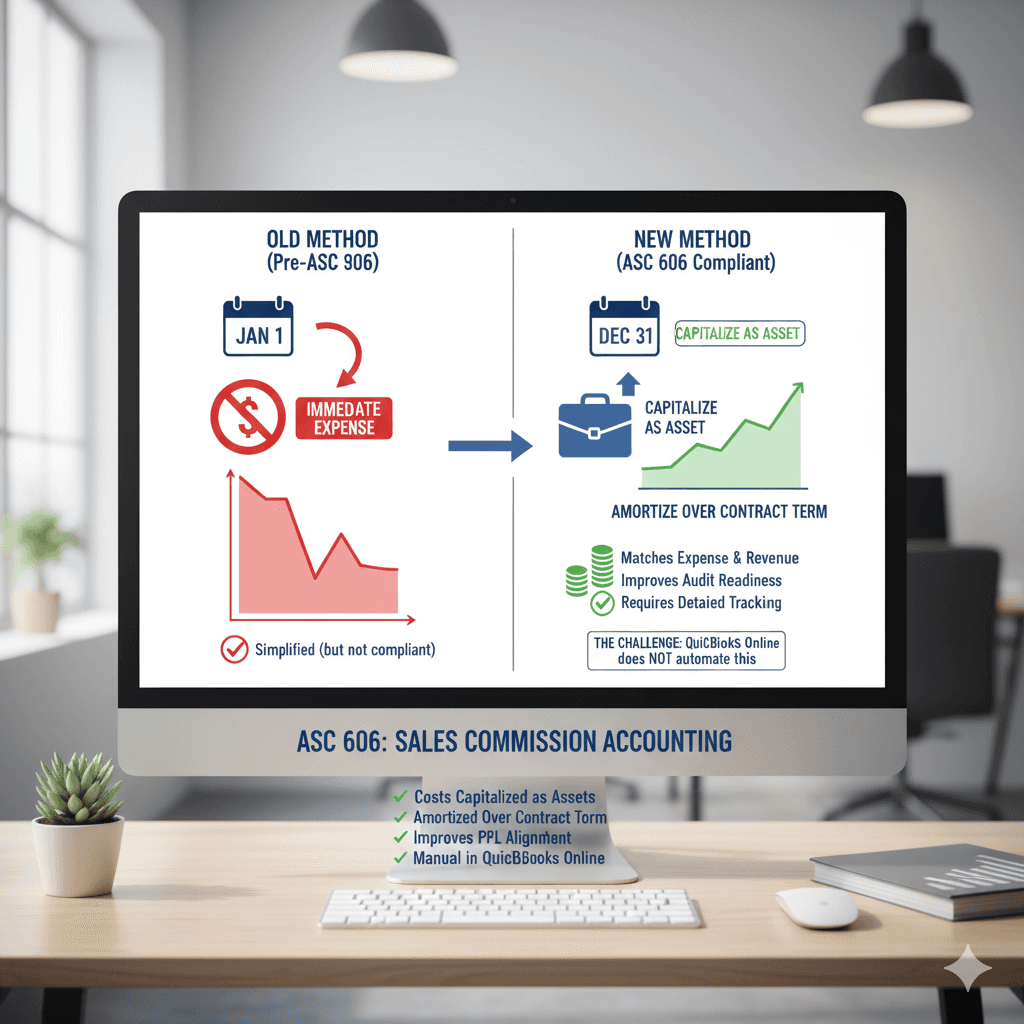

Old GAAP: Expense $15,000 in year one.

ASC 606: Record $15,000 as a Deferred Commission Asset, expense $5,000 per year over three years.

This treatment ensures costs are recognized in the same periods as the revenue they helped generate.

Why Deferring Commissions Matters

Compliance

ASC 606 requires compliance for public companies and most private firms; improper treatment risks audit adjustments [2].Accurate Profitability

Without deferral, year-one costs spike, making long-term contracts appear unprofitable.Stakeholder Confidence

Investors and auditors expect expense recognition that mirrors economic reality.Better Forecasting

Aligning costs with revenues enables more accurate forward-looking cash flow and margin projections.

How to Calculate Deferred Commissions

Formula:

Deferred Commission Expense per Period = Total Commission ÷ Contract Term

Example Calculation:

Commission = $12,000

Contract = 24 months

Amortization = $500 per month

Special Considerations [3]:

Renewals: If expected with no new commissions, extend amortization beyond initial term.

Modifications: Any change in term or pricing requires recalculating deferrals.

Early termination: Expense remaining unamortized balance immediately.

Journal Entry Examples

Initial Recognition

Debit: Deferred Commission Asset

Credit: Cash/Commission Payable

Monthly Amortization

Debit: Commission Expense

Credit: Deferred Commission Asset

Contract Modification

Debit/Credit: Deferred Commission Asset

Credit/Debit: Commission Expense

These entries ensure expenses are systematically recognized in line with contract revenue.

Common Challenges in QuickBooks Online which FinBoard.ai can address

No Native Deferral Module

QuickBooks online records expenses immediately; amortization requires manual schedules. FinBoard.ai with its inbuilt process for amortizaton helps to expense it over the period of time.Spreadsheet Dependency

Tracking amortization outside QuickBooks online creates reconciliation risks. FinBoard.ai uses Google sheet plugin with which spreadsheet dependency can be minimised.Contract Modifications

Adjustments for upsells or term changes are cumbersome without automation.All the contract modifications can be automated with specific inputs to the terms with FinBoard.ai.Audit Trail

Auditors require detailed schedules, which QuickBooks online alone cannot generate. FinBoard.ai with its plugin can act as a documentation tool which will be useful for audit trails.

Quick Start Checklist

Tool and Workflow Comparison

Workflow | Pros | Cons | Best Fit |

Manual in QuickBooks online + Excel / Google sheets | Low cost, flexible | High error risk, poor audit trail | Very small firms |

Automation add-ons via Google sheets (e.g., FinBoard.ai plugin) | Automates schedules, integrates with QuickBooks online | Setup cost, training needed | Growth SaaS/SMBs |

Expanded Mini-Case: Deferred Commissions in SaaS with QuickBooks Online

Case 1: SaaS Company with Domestic USD Contracts

Background:

CloudMetrics, a mid-market SaaS provider based in California, signs 200 new 3-year SaaS contracts in FY2025. Each contract:

ARR = $60,000 ($180,000 TCV)

Commission = 10% upfront ($18,000 per contract)

Total commissions = $3.6M in year one

Challenge:

QuickBooks Online would normally expense $3.6M in Year 1.

This wipes out apparent profitability, while actual revenue accrues evenly across 3 years.

CFO must comply with ASC 606 and show expenses spread out over the contract term.

Approach:

Initial Recording (Contract Signing)

Dr. Deferred Commissions (Asset) $3,600,000

Cr. Cash/Commission Payable $3,600,000

Monthly Amortization (36 months)

Per contract: $18,000 ÷ 36 = $500 per month

Across 200 contracts: $100,000 per month

Dr. Commission Expense $100,000

Cr. Deferred Commissions $100,000

Operational Complexity:

QuickBooks online has no deferral module → finance team creates a master Excel amortization schedule.

Each new contract adds rows in Excel, with contract ID, start date, term, total commission, and amortization stream.

Monthly recurring journal entries uploaded into QuickBooks online.

Result:

P&L now shows ~$1.2M annual expense instead of a $3.6M spike in year one.

Margins better reflect SaaS unit economics.

Auditors satisfied because workpapers show tie-out from contract → Excel → QuickBooks online journal entries.

Case 2: SaaS Company with Multi-Currency Contracts (US + India Subsidiary)

Background:

CloudMetrics expands into India. Contracts are priced in INR, commissions paid locally, but consolidated reporting is in USD.

Contract Example:

Indian customer contract: ₹90,00,000 over 3 years (~$108,000 at INR 83/USD).

Commission paid in India: 8% = ₹7,20,000 (~$8,675).

Exchange rates fluctuate between 81–85 INR/USD over the term.

Challenge:

Under ASC 606, commission must be deferred.

But consolidation requires recording the amortization in INR locally and translating at the quarter-end RBI reference rate for US GAAP reporting.

Approach:

Local (India books in INR):

Initial recognition:

Dr. Deferred Commissions (Asset) ₹7,20,000

Cr. Cash/Commission Payable ₹7,20,000

Monthly amortization over 36 months:

Dr. Commission Expense ₹20,000

Cr. Deferred Commissions ₹20,000

US Consolidation (in USD):

Each quarter, the unamortized INR balance is translated at quarter-end rate.

FX gain/loss recorded separately in OCI (or P&L depending on policy).

Example: After 12 months, deferred balance = ₹4,80,000. If exchange rate shifts from 83 to 85 INR/USD:

At 83: $5,783

At 85: $5,647

FX difference ($136) booked as currency translation adjustment.

Result:

Local team sees smooth amortization in INR.

Group reporting reflects USD volatility transparently.

CFO can explain variances in consolidated expense due purely to FX, not operational performance.

Case 3: Multi-Currency + Renewal + Churn Complications

Background:

CloudMetrics closes a Pan-Europe SaaS deal with a global client, spanning offices in Germany, France, and India.

Total Contract: €600,000 (3 years) + ₹30,00,000 India license (~$36,000).

Commission structure:

Europe sales rep: 10% of €600,000 = €60,000

India rep: 5% of ₹30,00,000 = ₹1,50,000

Global consolidation currency: USD.

Complications:

Renewal option in Year 3 → amortization period may extend beyond initial contract.

Partial churn in India (customer downgrades) → unamortized commissions must be accelerated.

Cross-currency reporting → EUR, INR, and USD rates fluctuate, requiring constant translation.

Workflow:

Europe (EUR):

Initial recognition:Dr. Deferred Commissions (Asset) €60,000

Cr. Cash/Commission Payable €60,000

Amortization: €1,667/month over 36 months.

India (INR):

Initial recognition:

Dr. Deferred Commissions (Asset) ₹1,50,000

Cr. Cash/Commission Payable ₹1,50,000

Amortization: ₹4,167/month.

Consolidation in USD:

Quarterly FX translation for unamortized balances.

Example: At Q1 close, EUR/USD = 1.10, INR/USD = 83.

Group reporting shows:

Europe deferred balance: €55,000 → $60,500

India deferred balance: ₹1,37,500 → $1,657

Total consolidated deferred asset: $62,157.

Renewal in Year 3:

If renewal is likely (per historical churn), amortization period extended to 5 years.

Europe rep commission extended, reducing monthly expense.

Churn Adjustment (India):

Customer downgrades in month 18, cutting contract in half.

Remaining unamortized commission: ₹75,000 must be expensed immediately:

Dr. Commission Expense ₹75,000

Cr. Deferred Commissions ₹75,000

Result:

CFO presents consolidated financials in USD with transparent FX, renewal, and churn impacts.

QuickBooks online alone cannot track this → team maintains detailed Excel + uploads monthly amortization entries.

Auditors satisfied because reconciliation shows: Contract → Local Books → Consolidated USD.

Risks & Mitigations

Risk | Impact | Mitigation |

Misclassifying non-qualifying costs | Overstated assets | Clear capitalization policy |

Spreadsheet dependency | Errors, audit issues | Automate deferrals or reconcile often |

Missed contract modifications | Misstated expenses | Review schedules quarterly |

Poor documentation | Audit deficiencies | Maintain workpapers and approvals |

FAQ

1. How are commissions treated under ASC 606?

They are capitalized as assets and amortized systematically over the contract period.

2. Are deferred commissions assets or liabilities?

They are assets, representing future economic benefit from contract revenue.

3. How are early terminations handled?

Unamortized balances are expensed immediately unless replaced by new contracts.

4. Can marketing or lead-gen costs be deferred?

No, only direct incremental costs such as commissions qualify.

5. Does QuickBooks Online support automated deferred commissions?

No. QuickBooks online requires manual schedules or third-party integrations for compliance.

Glossary

ASC 606: Revenue recognition standard covering contracts with customers.

Deferred Commission Asset: Capitalized sales commissions recorded on the balance sheet.

Amortization: Systematic allocation of deferred costs over time.

Contract Acquisition Costs: Direct, incremental costs of securing a customer contract.

Deferred Revenue: Cash received for undelivered services, recorded as a liability.