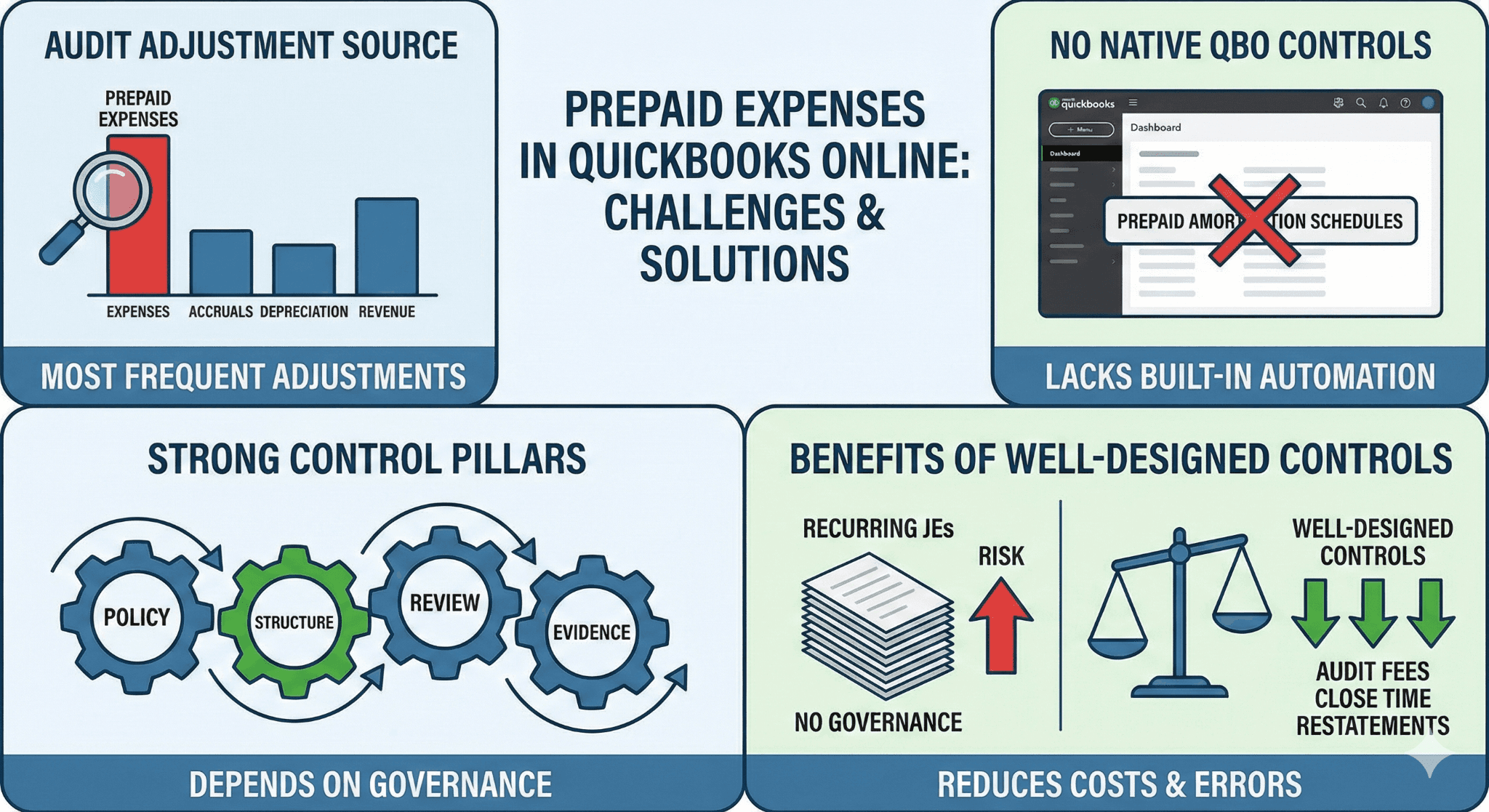

Prepaid expenses are one of the most frequent sources of audit adjustments in QuickBooks Online environments.

QuickBooks Online does not provide native prepaid amortization controls.

Strong prepaid controls depend on policy, structure, review, and evidence.

Recurring journal entries without governance increases risk.

Well-designed controls reduce audit fees, close time, and restatements.

Executive Summary

Prepaid expenses sit at an uncomfortable intersection of cash accounting behavior and accrual accounting requirements. The transaction feels complete when cash leaves the bank. The accounting is not.

For small and mid-market companies using QuickBooks Online, prepaid expense amortization is consistently under-controlled. Teams rely on memory, spreadsheets, and periodic clean-up entries. These practices create silent misstatements that surface during audits, diligence reviews, or board reporting.

The root problem is not technical capability. It is a control design. QuickBooks Online prioritizes speed and simplicity. It does not enforce accounting discipline. As a result, prepaid expense controls must be intentionally designed and operationalized.

This article presents a comprehensive, practical framework to design and implement internal control procedures for prepaid expenses amortization in QuickBooks Online-centric environments. The focus is execution. Each control is tied to a specific risk, mapped to QuickBooks Online functionality, and supported with real-world case studies drawn from SMB and mid-market operations.

1. Why Prepaid Expenses Are a High-Risk Area

Prepaid expenses fail for predictable reasons.

1.1 Cash Bias at Entry

Most prepaid expenses originate from vendor bills or credit card charges. The natural instinct is to record the cost as an expense. This bias is reinforced by QuickBooks Online default account mappings and bank feed automation.

Once misclassified at entry, the error compounds.

1.2 Judgment-Based Amortization

Unlike depreciation, prepaid amortization is rarely system-driven. Contract terms vary. Service periods differ. Some benefits are front-loaded. Others are uniform.

Without explicit rules, two accountants will amortize the same prepaid differently.

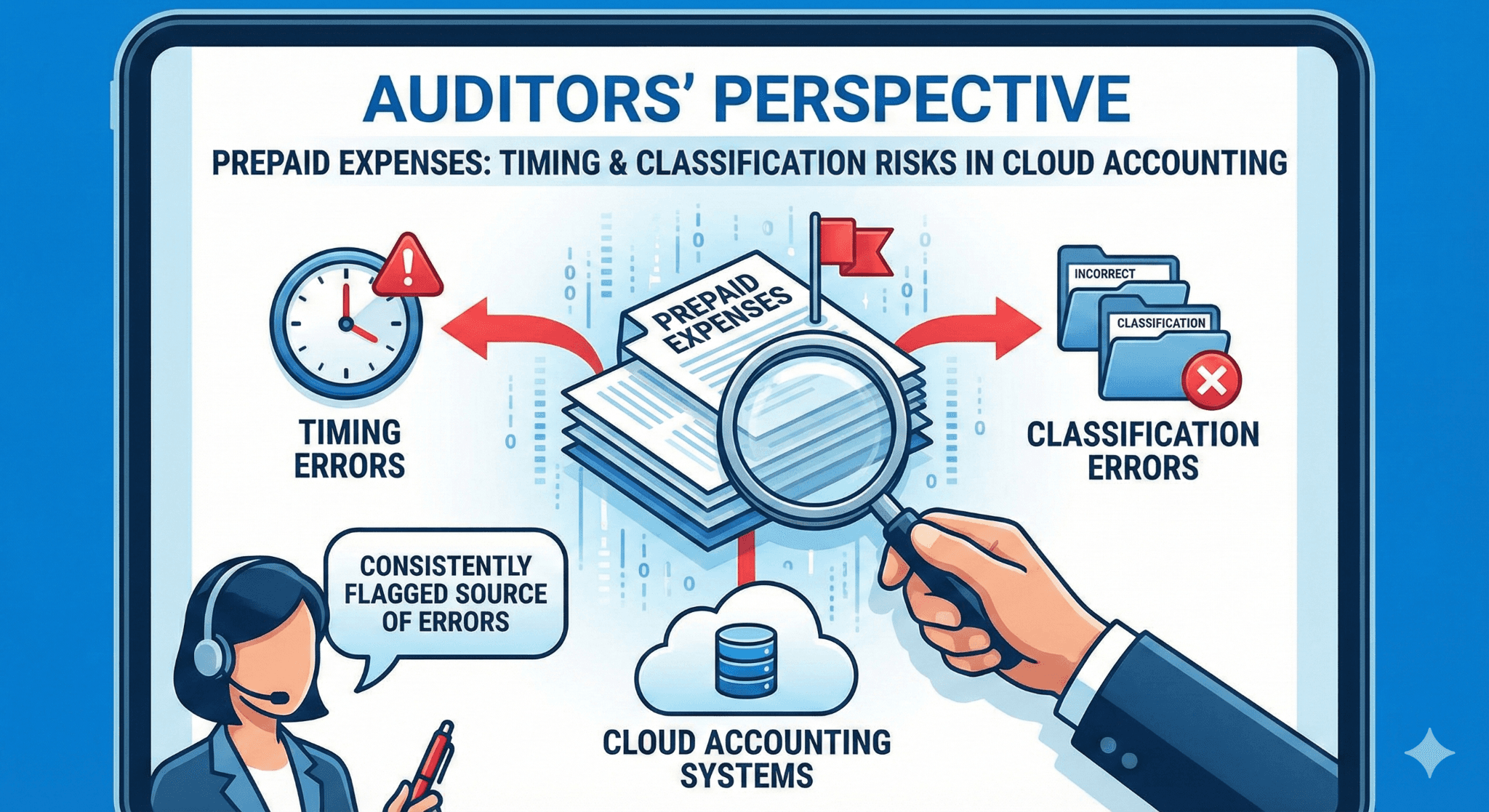

1.3 Lack of Native System Controls

QuickBooks Online lacks:

A prepaid expense module

Automated amortization schedules

Required approvals for journal entries

A prepaid subledger

Auditors consistently flag prepaid expenses as a source of timing and classification errors in cloud accounting systems

.

2. Control Objectives and Risk Mapping

Effective internal controls start with clarity of purposeEffective internal controls start with clarity of purpose. This foundational principle dictates that for any set of controls—whether financial, operational, or compliance-related—to be truly effective, their objectives must be unambiguously defined, understood, and communicated across the organization.

The Role of Clarity:

Defines 'Success': A clear purpose establishes the benchmark against which the control's success or failure can be measured. Without it, controls can become arbitrary compliance exercises rather than tools for risk mitigation.

Guides Design: The purpose directly influences the design and scope of the controls. For instance, a control meant to prevent fraud will look very different from one designed to ensure the accuracy of inventory counts. Ambiguity leads to controls that are either over-engineered (resource-intensive) or under-designed (leaving critical risks unaddressed).

Fosters Accountability: When employees understand why a control exists—to safeguard assets, ensure reliable reporting, or comply with regulations—they are more likely to take ownership of its execution. Clarity of purpose shifts the perception of controls from bureaucratic hurdles to essential business practices.

Ensures Alignment: Clear purpose ensures that individual controls align with the organization's overarching strategic goals and risk appetite. Controls should not operate in a vacuum; they must support the business objectives they are designed to protect.

Essential Components for a Clear Purpose:

Specific Risk Identification: The control must be tied to a specific, well-articulated risk it is intended to mitigate. (e.g., Risk: Unauthorized financial commitments; Purpose: To ensure all expenditures exceeding $5,000 are approved by two designated managers.)

Stated Objective: A concise statement of what the control is intended to achieve. (e.g., Objective: Reliability of financial reporting, or Objective: Compliance with environmental regulations.)

Scope and Boundaries: Defining what the control covers (and what it doesn't) prevents confusion and scope creep.

Defined Ownership: Assigning clear responsibility for the design, execution, monitoring, and maintenance of the control.

In summary, internal controls are not simply a checklist of tasks. They are deliberate mechanisms to manage risk. Their efficacy is directly proportional to the clarity of the underlying objective. A well-defined purpose is the cornerstone upon which robust, efficient, and sustainable internal control systems are built..

2.1 Key Risks

Risk Category | Description |

Classification Risk | Prepaid recorded as expense |

Timing Risk | Expense recognized in wrong period |

Authorization Risk | Unapproved journal entries |

Completeness Risk | Missing amortization entries |

Accuracy Risk | Incorrect amortization amount |

Documentation Risk | Inadequate audit support |

2.2 Control Objectives

Each risk maps to a control objective.

Risk | Control Objective |

Misclassification | Enforce prepaid identification at entry |

Timing errors | Align amortization to benefit period |

Unauthorized entries | Require documented approval |

Missed amortization | Automate with oversight |

Calculation errors | Standardize formulas |

Audit gaps | Retain evidence |

This mapping anchors the entire control framework.

3. Entry-Level Controls: Where Most Errors Begin

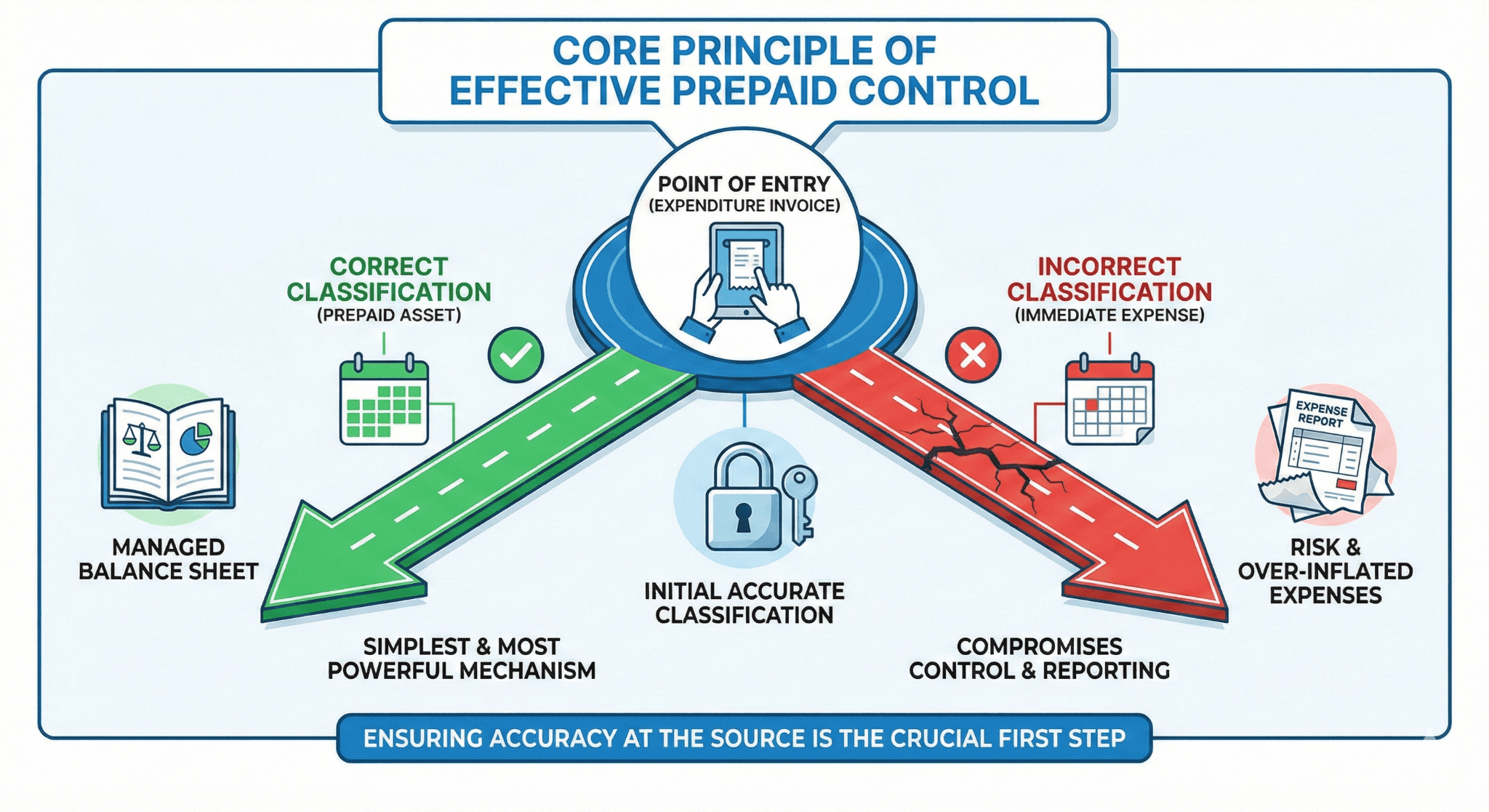

The most effective prepaid control is the simplest: correct classification at entry.

The core principle of effective prepaid control hinges on the most elementary yet crucial step: ensuring correct classification at the point of entry. This initial, accurate classification of an expenditure as a prepaid asset, rather than an immediate expense, is the simplest and most powerful mechanism for managing this balance sheet item.

Why Initial Classification is Paramount:

Foundation for Subsequent Accounting: A correct initial classification sets the entire accounting process in motion accurately. If an expenditure, such as an insurance premium or a rent payment covering multiple future periods, is mistakenly expensed immediately, the financial statements will be distorted—Net Income will be understated, and Assets will be understated. Conversely, if it is incorrectly classified as a prepaid asset, it creates an ongoing correction burden.

Streamlining Amortization: Prepaid assets must be systematically amortized (recognized as an expense) over the benefit period. Correct classification at entry provides the necessary data—the total prepaid amount, the start date, and the end date of the benefit—to create a proper amortization schedule. This eliminates manual calculation errors and ensures adherence to the matching principle.

Audit Trail and Compliance: A clean, well-defined entry classification provides a clear, defensible audit trail. It documents the business purpose of the payment, the period it covers, and the systematic method by which it will be recognized as an expense, satisfying regulatory and internal control requirements.

Preventing "Leakage": Prepaid assets, if not correctly logged and tracked, are susceptible to "leakage," where a future expense is prematurely or redundantly recognized. By enforcing strict initial classification and requiring supporting documentation (contracts, invoices), the company ensures that value is not lost and the asset is systematically converted to an expense as the benefit is consumed.

In essence, the simplicity of "correct classification at entry" is what makes it the most effective control, transforming a potentially complex tracking process into a structured, automated, and auditable accounting procedure.

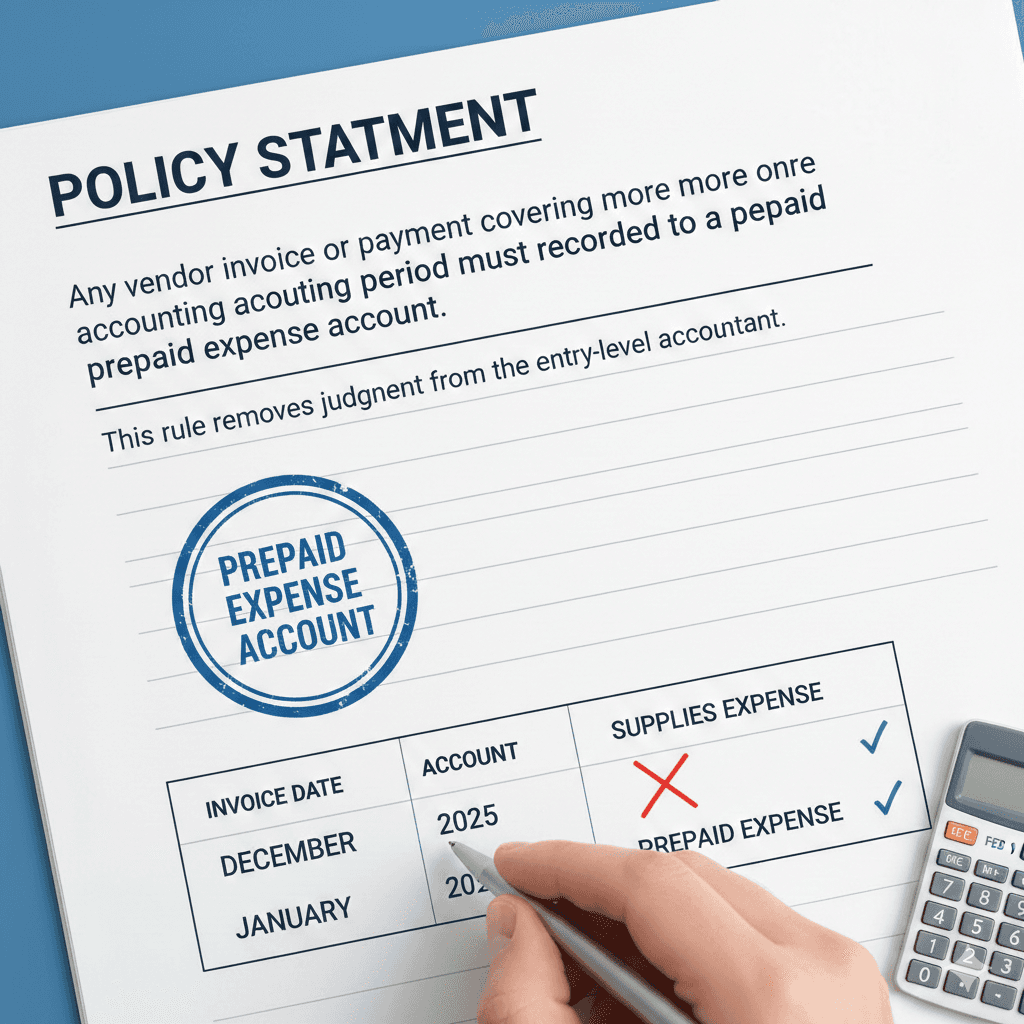

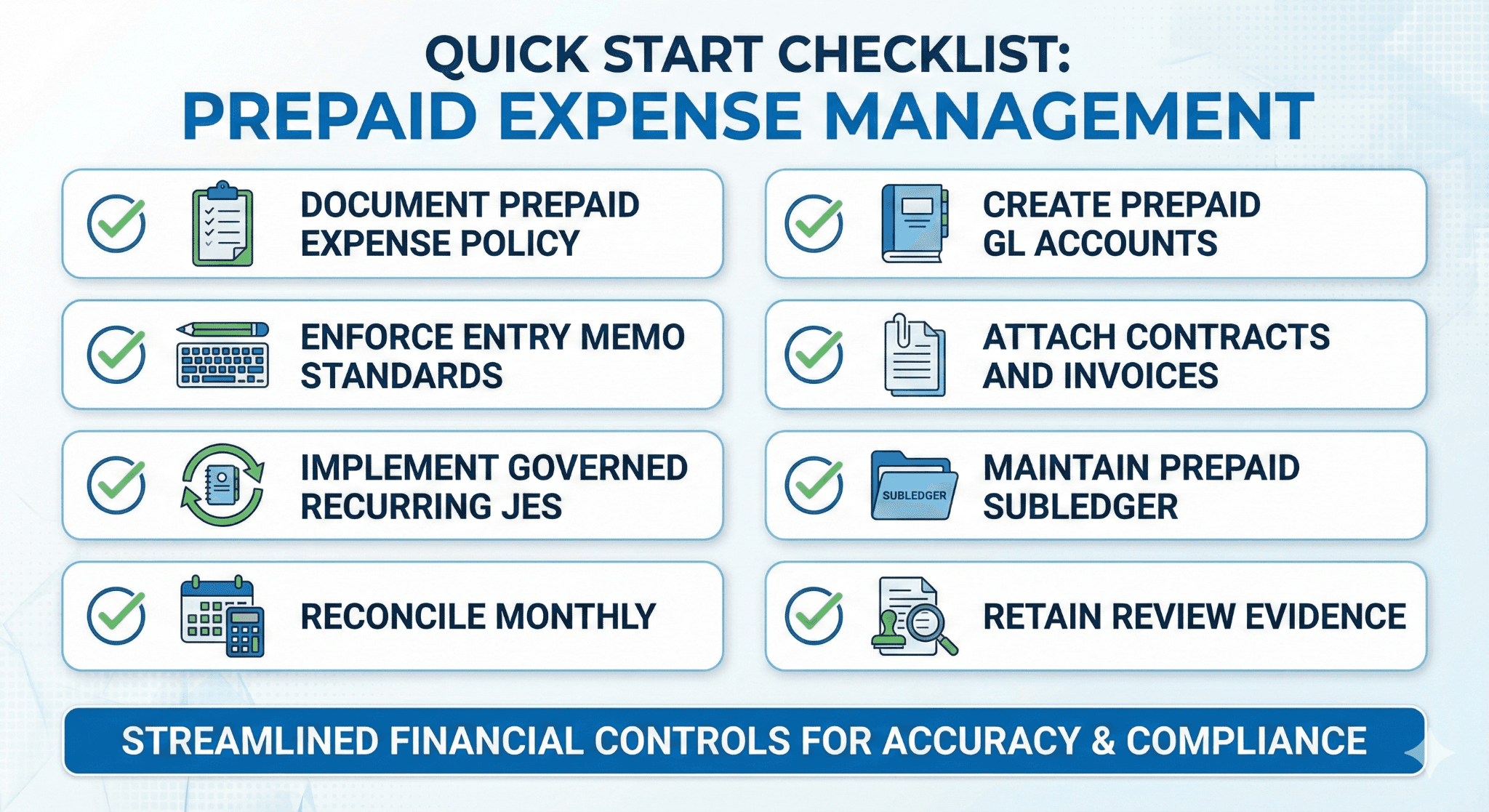

3.1 Policy Design

Policy Statement

Any vendor invoice or payment covering more than one accounting period must be recorded to a prepaid expense account.

This rule removes judgment from the entry-level accountant.

3.2 QuickBooks Online Implementation

Create dedicated prepaid accounts by category if material

Disable direct posting to expense accounts for prepaid vendors where possible

Enforce standardized memo fields:

Vendor name

Coverage period

Contract reference

Attachments are mandatory. Invoices and contracts must be stored within QuickBooks Online [1].

Case Study 1: Marketing Agency with Chronic Expense Spikes

Background

A 25-employee marketing agency prepaid annual advertising platforms.

Problem

Expenses spiked in January. Monthly profitability looked volatile. The board questioned forecasting credibility.

Root Cause

All annual subscriptions were expensed immediately.

Control Implemented

Prepaid advertising account

Mandatory memo format

Invoice attachment requirement

Result

Monthly expense volatility disappeared. Forecast accuracy improved. No system changes required.

4. Amortization Controls: Automation with Discipline

Automation without governance increases risk.

4.1 Recurring Journal Entries as the Amortization Engine

Recurring journal entries are the most common amortization tool in QuickBooks Online.

They must be controlled.

4.2 Required Governance Controls

Control | Purpose |

One JE per prepaid | Prevent aggregation errors |

Fixed end date | Avoid perpetual postings |

Naming convention | Enable review |

Independent approval | Prevent self-review |

Monthly JE report review | Detect anomalies |

Recurring entries must never be copied without review. Recurring entries must never be copied without thorough and critical review. This imperative is crucial for maintaining data integrity and accuracy within any system, especially those involving financial, logistical, or sensitive information. Blindly duplicating previous entries, even those that seem routine, carries a significant risk of propagating errors, perpetuating outdated information, or failing to account for necessary changes specific to the current period or transaction.

A comprehensive review process should involve several key steps:

Verification of Relevancy: Ensure that the underlying reason for the recurring entry still exists and is applicable to the current context. Changes in business operations, regulatory requirements, or project scope may render a previous entry obsolete or incorrect.

Confirmation of Data Accuracy: Scrutinize the core data points—such as amounts, dates, accounts, recipients, or quantities—against the most current source documents or operational realities. A rate change, a new vendor, or a corrected address are common reasons for necessary adjustments.

Cross-Reference with External Factors: Review any external variables that might impact the entry, such as exchange rates, tax laws, contract terms, or budget constraints. These factors are frequently dynamic and require real-time updates.

The practice of routinely copying recurring entries without this diligent review undermines the reliability of records and can lead to serious consequences, including financial misstatements, compliance failures, or operational inefficiencies. Therefore, every seemingly repetitive entry must be treated as a fresh, unique transaction requiring individual validation.

Case Study 2: SaaS Company with Audit Adjustments

Background

A venture-backed SaaS company prepaid cloud infrastructure annually.

Problem

Audit adjustments every year. Recurring entries continued after contract termination.

Root Cause

Recurring JEs lacked end dates and review.

Controls Added

End-date enforcement

Monthly recurring JE review

Prepaid register reconciliation

Result

Zero audit adjustments for prepaid expenses over two audit cycles.

5. Prepaid Subledger: The Missing Control Layer

QuickBooks Online does not provide a prepaid subledger. One must exist externally.

5.1 Minimum Subledger Requirements

Field | Purpose |

Vendor | Identification |

Original amount | Baseline |

Start date | Timing |

End date | Termination |

Monthly amortization | Accuracy |

Remaining balance | Reconciliation |

5.2 Reconciliation Control

Monthly reconciliation is non-negotiable.

Tie subledger total to GL balance

Investigate variances

Retain evidence [4][14]

Case Study 3: Professional Services Firm with Restatement Risk

Background

A consulting firm prepaid software licenses across departments.

Problem

Prepaid balance drifted from GL by six figures.

Root Cause

No centralized register. Multiple spreadsheets.

Control Implemented

Single master subledger

Monthly reconciliation sign-off

Result

Balance integrity restored within two months.

6. Review and Approval Controls

Journal entries are the highest-risk transactions in QuickBooks Online.

6.1 Approval Design

QuickBooks Online does not enforce JE approval. Compensating controls are required.

Preparer and reviewer segregation

Email or workflow tool approval

Approval evidence retained [13]

6.2 Evidence Expectations

Auditors expect:

Policy documentation

Subledger

JE approval proof

Reconciliation sign-offs

Case Study 4: Acquisition Due Diligence Failure Avoided

Background

A mid-market distributor entered acquisition talks.

Risk

Buy-side diligence focused on prepaid expenses.

Controls in Place

Documented prepaid policy

Monthly reconciliation

Complete audit trail

Outcome

No purchase price adjustment related to prepaid expenses.

7. Operating Model for SMBs and Mid-Market Companies

7.1 Roles and Responsibilities

Role | Responsibility |

Bookkeeper | Entry and documentation |

Accountant | Amortization and subledger |

Controller | Review and approval |

7.2 Close Checklist Integration

Prepaid controls must be embedded into the monthly close checklist, not treated as an afterthought.

Tool and Workflow Comparison

Approach | Control Strength | Audit Acceptance |

Manual monthly JEs | Low | Weak |

Recurring JEs only | Medium | Moderate |

Recurring JEs + subledger | High | Strong |

FinBoard.ai module | Very High | Very Strong |

Risks and Mitigations

Risk | Mitigation |

Human error | Standardized templates |

Staff turnover | Written policies |

Reviewer fatigue | Exception-based review |

Tool limitations | Compensating controls |

FAQ

Are prepaid expenses assets?

Yes. They represent future economic benefit until consumed.

Is a spreadsheet acceptable for audit?

Yes, if reconciled, reviewed, and retained.

Should small companies bother with this?

Yes. Smaller teams experience higher error concentration.

Can automation replace review?

No. Review remains essential.

How long should evidence be retained?

At least the audit look-back period.

Glossary

Prepaid Expense: Payment made before receiving benefit.

Amortization: Systematic expense recognition over time.

Subledger: Detailed support for a GL balance.

Recurring Journal Entry: Automated periodic posting.

Compensating Control: Manual control replacing system limitation.