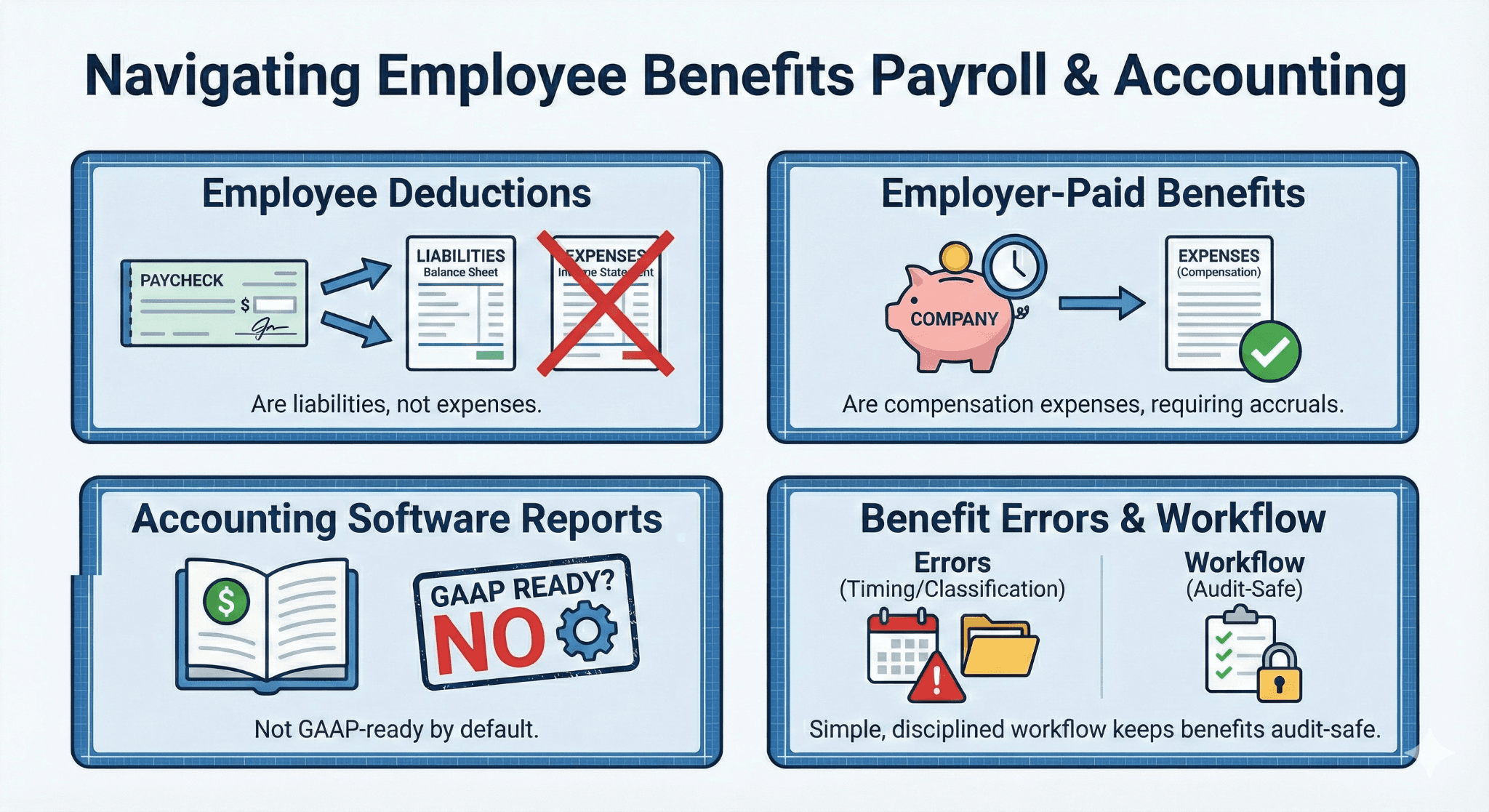

Employee benefit deductions are liabilities, not expenses.

Employer-paid benefits are compensation expenses, often requiring accruals.

QuickBooks payroll reports are not GAAP-ready by default.

Most benefit errors come from timing and classification, not math.

A simple, disciplined workflow keeps benefits audit-safe.

Executive Summary

Employee benefits accounting is where otherwise clean QuickBooks files quietly go wrong. Payroll runs correctly, paychecks are accurate, and vendors get paid. Yet the financial statements tell a different story. Expenses are overstated. Liabilities drift. Controllers lose confidence in payroll numbers.

The root cause is simple. QuickBooks Online payroll is built for payroll compliance, not US GAAP financial presentation. Payroll reports mix employee deductions with employer costs. The system does not explain which amounts are expenses and which are liabilities. Accountants are expected to know the difference and fix it.

.

This article explains how benefit accounting should work, how QuickBooks actually posts benefits, where users go wrong, and how to fix it without overcomplicating the books.

Why Employee Benefits Are a Problem Area in QuickBooks

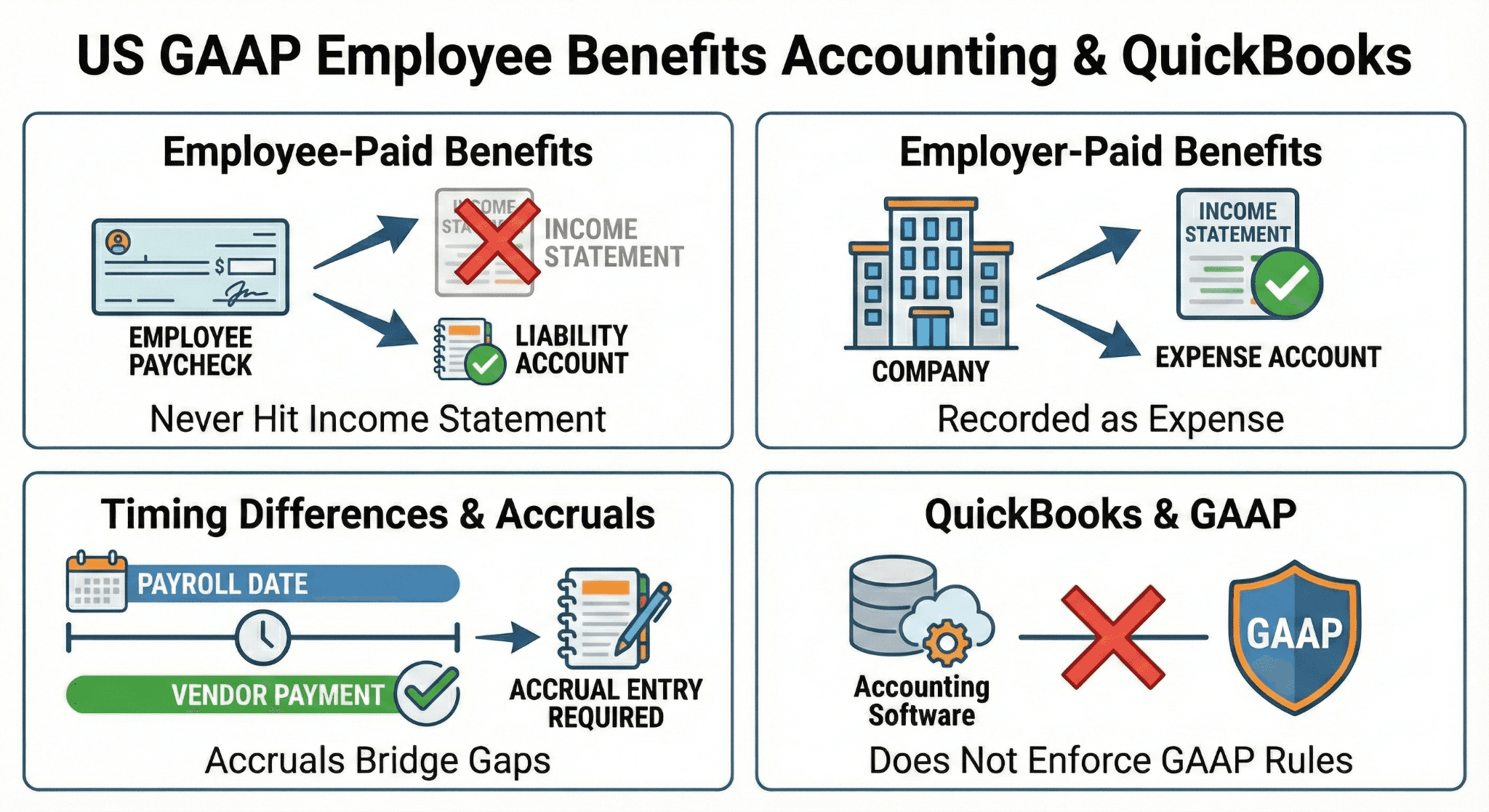

QuickBooks Online does many things well. Payroll calculations, tax filings, and payment workflows are strong. Financial reporting for complex payroll items is not the focus.

Payroll screens answer operational questions:

What is the net pay?

What taxes are owed?

What deductions were taken?

US GAAP answers different questions:

What costs belong to the company?

What amounts are owed to third parties?

Which period should recognize the expense?

QuickBooks does not bridge that gap. It assumes accountants will.

The danger is subtle. Payroll reports look authoritative. Totals look like expenses. Many users assume posting them directly to the general ledger is correct. That assumption is the source of most benefit accounting errors.

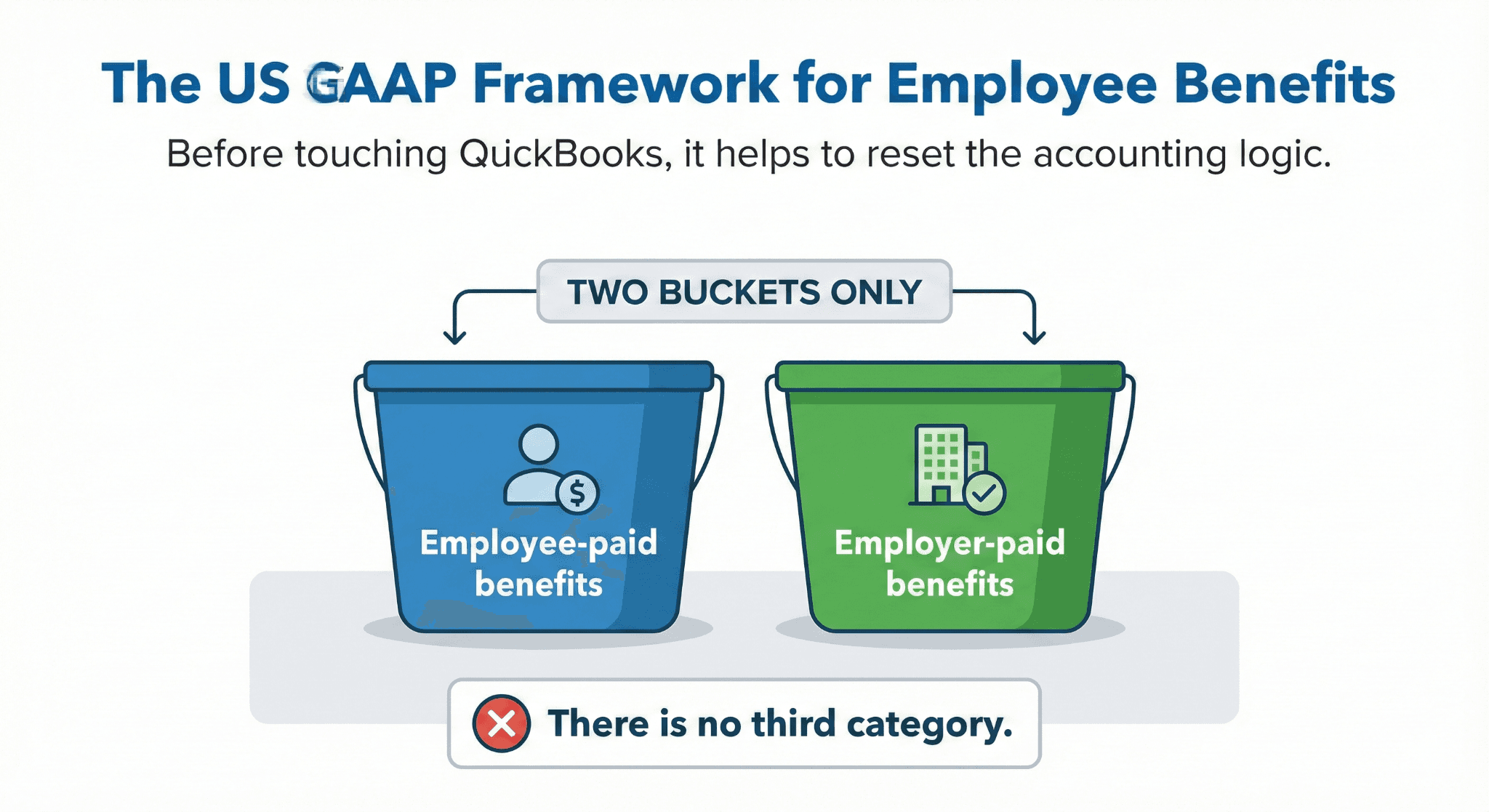

The US GAAP Framework for Employee Benefits

Before touching QuickBooks, it helps to reset the accounting logic.

Two Buckets Only

Every benefit-related amount falls into one of two categories:

Employee-paid benefits

Employer-paid benefits

There is no third category.

Employee-Paid Benefits (Not an Expense)

Examples include:

Employee health insurance deductions

Employee retirement contributions

Voluntary benefit deductions

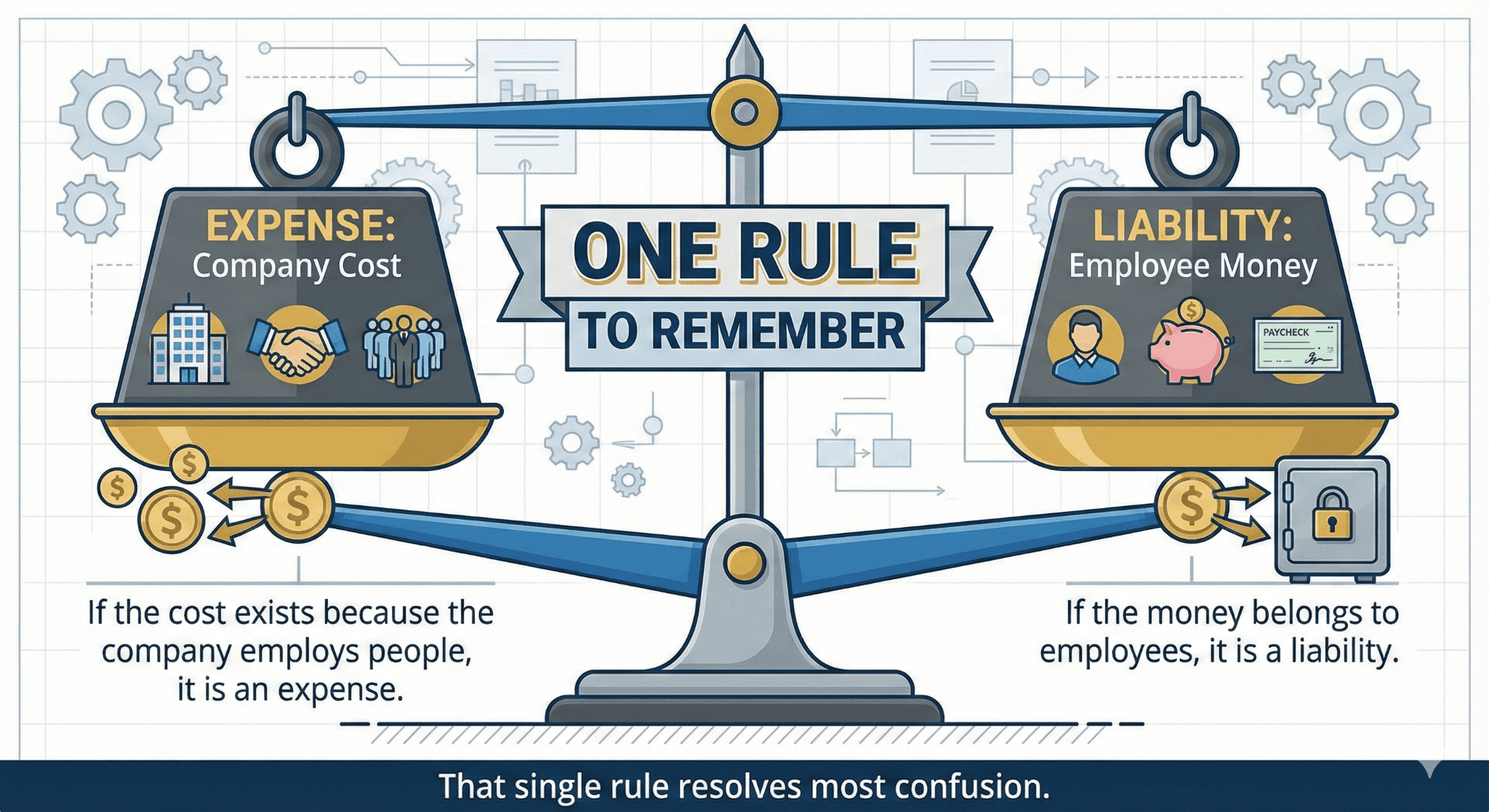

From a GAAP perspective, this money never belongs to the company. The company is temporarily holding it before remitting it to a provider.

Correct treatment:

Credit a liability account when deducted from payroll

Debit the liability when paid to the provider

These amounts should never touch the income statement.

Employer-Paid Benefits (An Expense)

Examples include:

Employer portion of health insurance

Employer retirement match

Employer-paid life or disability insurance

These are part of total employee compensation.

Correct treatment:

Debit benefit expense

Credit cash or a liability, depending on payment timing

If the benefit relates to services already rendered, the expense belongs in that period, even if paid later.

How QuickBooks Payroll Actually Posts Benefits

QuickBooks payroll processes benefits correctly for paychecks and tax filings. Accounting classification is secondary.

Common QuickBooks behaviors include:

Combining employee and employer amounts in summary reports

Posting payroll items directly to expense accounts

Paying benefit providers outside the payroll transaction

None of these violate payroll rules. All of them can violate GAAP presentation if left unadjusted.

QuickBooks does not stop you from misclassifying benefits. It assumes you will review the output.

The Most Common Mistake: Expensing Everything

The most frequent error looks like this:

Export payroll summary.

See total benefits number.

Post the entire amount to benefit expenses.

This overstates expenses and understates liabilities.

Auditors see this immediately. Controllers feel it when payroll costs fluctuate inexplicably.

The fix is not complicated. It just requires separating what belongs to whom.

Setting Up the Right Accounts in QuickBooks

You do not need a complex chart of accounts. You need clear separation.

Minimum Accounts

At a minimum, set up:

Employee Benefits Payable (liability)

Employer Benefits Expense (expense)

Optional, but helpful:

Health Insurance Payable

Retirement Contributions Payable

Clarity beats granularity.

Reviewing Payroll Item Mapping

Payroll items drive how QuickBooks posts transactions.

Key checks:

Employee deductions should credit liability accounts.

Employer contributions should debit expense accounts.

Default mappings should not be trusted blindly.

Many payroll items default to expense accounts for convenience. That convenience often conflicts with GAAP.

Spend time here once. It saves time every month.

Timing Differences: Where Accruals Matter

Benefits are often paid after payroll.

Example:

Payroll date: March 28

Health insurance payment date: April 5

Under GAAP, the expense belongs in March.

Correct treatment at March close:

Debit benefit expense

Credit benefit payable

When payment occurs in April:

Debit payable

Credit cash

QuickBooks payroll does not do this automatically. Month-end review must.

Reconciling Benefit Liabilities Each Month

If benefit liabilities are not reconciled, errors compound quietly.

Best practice:

Run payroll liability reports

Compare to general ledger liability balances.

Investigate differences monthly.

Unreconciled benefit liabilities are a red flag in audits and due diligence.

Why Payroll Reports Are Not GAAP Schedules

Payroll reports are operational documents. They answer payroll questions, not financial reporting questions.

Problems with using payroll reports as-is:

Employee deductions included in totals

No separation by accounting treatment

Cash basis presentation by default

Payroll reports are inputs. Accounting entries are outputs. Confusing the two leads to misstatements.

Mini-Case: Manufacturing Company With Rising Benefit Costs

Background

A 75-employee manufacturer saw benefit expense increase faster than headcount.

Investigation

Payroll summaries were posted directly to expenses.

Finding

Employee deductions were included in benefit expense.

Fix

Reclassified employee portion to liability. Adjusted prior periods.

Result

Benefit expense aligned with expectations. Controller confidence restored.

Nothing about payroll changed. Only accounting treatment did.

Handling Employer Benefits Paid Outside Payroll

Some employers pay benefits directly, not through payroll.

Examples:

Annual insurance premiums

One-off wellness programs

Correct approach:

Record expense in the period incurred

Accrue if payment timing differs

Do not route through payroll if no payroll deduction exists

QuickBooks support often suggests consulting an accountant here. This is why.

Avoiding Double Counting of Employer Contributions

A subtle but common issue:

Payroll posts employer benefit expense.

Payment to provider is coded to expense again.

This doubles the cost.

Correct approach:

Payroll posts expense and liability.

Provider payment clears the liability.

Expense should occur once.

Controller-Level View: What Matters Most

Controllers care about three things:

Accuracy

Consistency

Defensibility

Benefit accounting affects all three.

A clean benefit workflow:

Stabilizes operating margins

Prevents audit adjustments

Improves forecasting accuracy

Payroll accuracy alone is not enough.

Tool and Workflow Comparison

Workflow | Setup Effort | Accuracy | Audit Readiness |

Payroll totals only | Low | Low | Low |

Payroll + journal entries | Medium | High | High |

Spreadsheet tracking | Medium | Medium | Low |

The middle option wins in most SMB environments.

Risks and Mitigations

Risk: Overengineering

Some SMBs do not need detailed benefit schedules.

Mitigation:

Match complexity to reporting needs.

Risk: Treating Payroll as Accounting

Payroll systems process payments. They do not decide GAAP treatment.

Mitigation:

Always review payroll output through an accounting lens.

Risk: Ignoring Timing

Benefits paid later still belong in the service period.

Mitigation:

Accrue consistently.

Frequently Asked Questions

Are employee benefit deductions ever expenses?

No. They are liabilities until remitted.

Does QuickBooks Online enforce GAAP rules?

No. It provides flexibility, not enforcement.

Do small companies need to do this?

Yes, if they issue GAAP financials.

Will auditors check benefit accounting?

Almost always.

Can this be automated fully?

Not today. Review is required.

Glossary

Employee Withholding

Amounts deducted from employee pay and owed to third parties.

Employer Contribution

Benefit cost borne by the company as compensation.

Accrual Accounting

Recognizing expenses when incurred, not when paid.

Payroll Liability

Amounts owed but not yet remitted.