Executive Summary

A gain on bargain purchase is one of the most uncomfortable outcomes in acquisition accounting. It feels wrong at first glance. Management worries it looks aggressive. Auditors assume valuation errors. Accountants hesitate to book it at all. In practice, bargain purchases are legitimate, especially in SMB and mid-market transactions involving distressed sellers, forced exits, or time-constrained deals.

US GAAP under ASC 805 is explicit. When the fair value of identifiable assets acquired exceeds the consideration transferred, the acquirer must recognize the difference immediately in earnings. There is no concept of negative goodwill. There is no deferral mechanism. The only safeguard is a mandatory reassessment of every valuation input before recognition.

QuickBooks Online complicates this process. It was never designed for business combinations. There is no purchase price allocation workflow, no fair value engine, and no guardrails to prevent misclassification. As a result, bargain purchase gains are often buried, netted, misstated, or reversed during audit.

This article explains, in detail, how to account for a gain on bargain purchase in QuickBooks Online correctly, defensibly, and repeatably. It walks through real acquisition scenarios, journal mechanics, audit considerations, disclosure implications, and controller-level controls, with a focus on SaaS and mid-market environments.

1. Understanding the Concept Without the Textbook Noise

Let us strip this down.

A bargain purchase means one thing:

You paid less than what the acquired business was worth on the acquisition date.

That is it.

It does not mean:

You overvalued assets.

You are gaming earnings.

You discovered hidden goodwill.

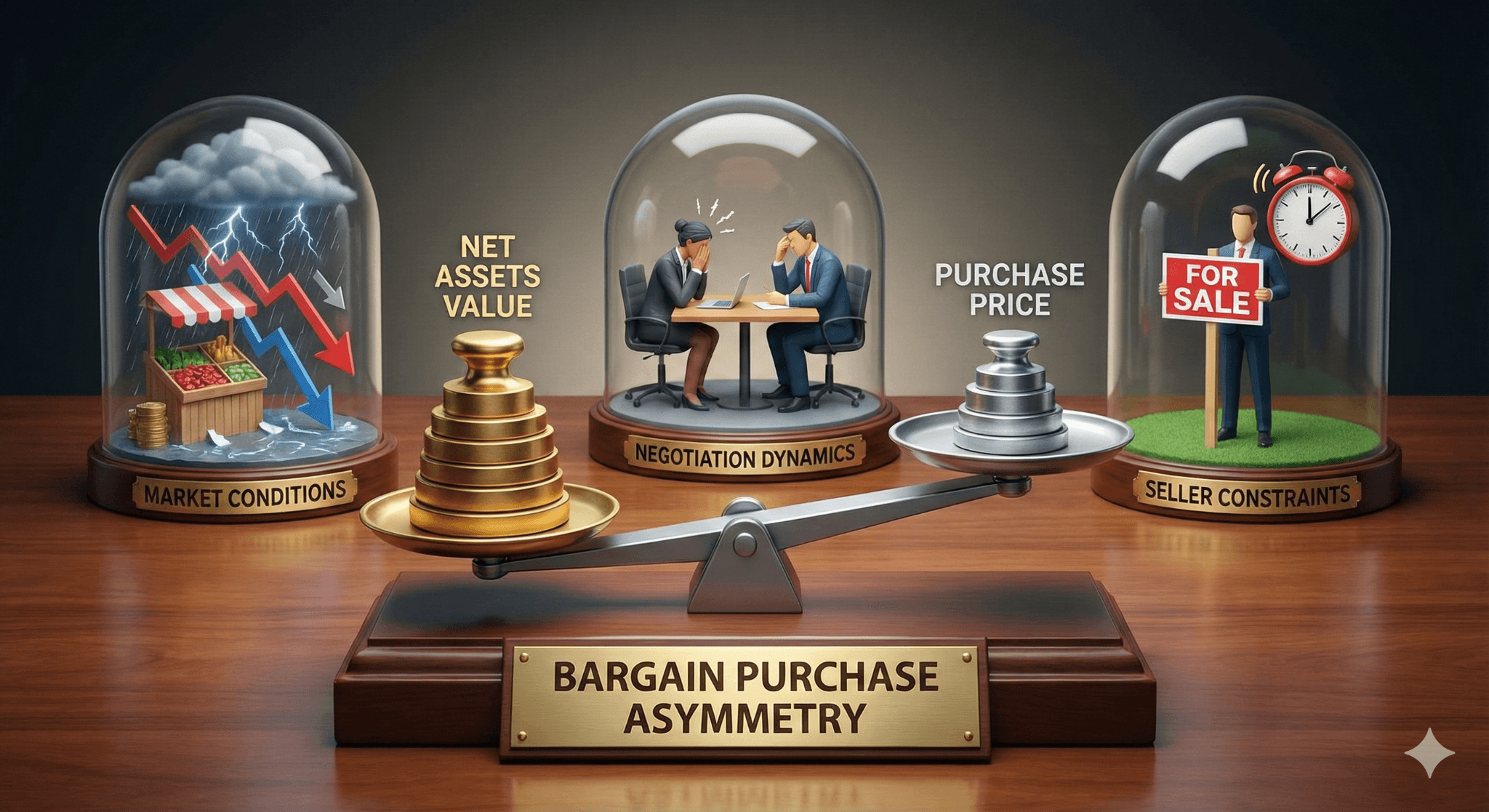

It means market conditions, negotiation dynamics, or seller constraints created an asymmetry.

Why This Happens More Often Than People Admit

In large public company deals, investment banks and competitive auctions usually eliminate bargain outcomes. In SMB and mid-market deals, those controls do not exist.

Common real-world drivers include:

Liquidity crises forcing sellers to accept lower prices.

Founders prioritizing speed over valuation.

Venture-backed companies exiting quietly after failed funding rounds.

Asset sales executed under legal or regulatory pressure.

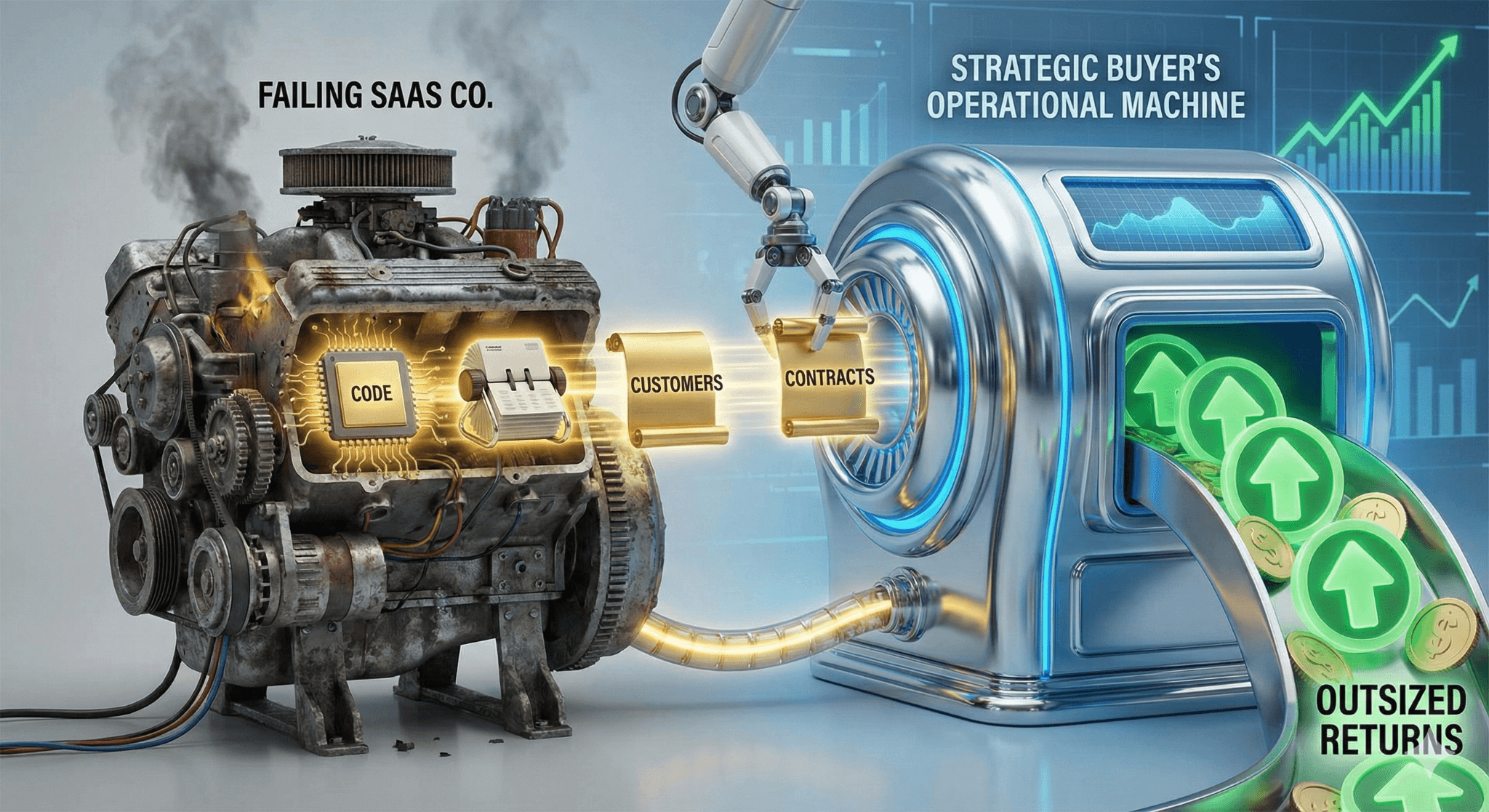

In SaaS acquisitions, this is amplified. Code, customers, and contracts retain value even when the company itself is failing operationally.In traditional mergers and acquisitions, the value proposition is often tied to the immediate operational health and profitability of the target company. However, in the realm of SaaS (Software as a Service) acquisitions, this dynamic is significantly amplified, creating a distinct investment thesis.

The core reason for this amplified value retention is the nature of the assets. Even when a SaaS company is demonstrably failing operationally—perhaps burdened by high churn, poor management, or inefficient marketing—three fundamental components can retain immense intrinsic value for a strategic acquirer:

Code and Intellectual Property (IP): The underlying codebase, proprietary algorithms, and unique technical architecture represent a significant sunk cost and a competitive advantage. An acquirer can instantly gain years of development work, intellectual property, and features, often referred to as an "acquihire" of the technology itself. This IP can be integrated into existing products, accelerating the acquirer's roadmap far faster and cheaper than building the features from scratch.

Customers and User Base: A paying or even an active free user base is a highly valuable asset, regardless of the target company's operational shortcomings. The hardest part of scaling a SaaS business is often the initial customer acquisition and proof-of-concept. An acquirer can instantly inherit an established user base, access a new market segment, and immediately begin cross-selling or upselling their own, more mature services. The customer base provides a clear, defensible path to revenue recovery through better account management, product improvement, and pricing optimization, assuming the acquirer has superior operational capabilities.

Contracts and Recurring Revenue: SaaS relies on subscription models, which generate highly predictable, recurring revenue (ARR/MRR). The existing customer contracts—even those at risk—represent an immediate revenue stream. For the acquirer, this provides a stable financial floor. Furthermore, the contract data (usage patterns, renewal cycles, and pricing tiers) offers invaluable insight into customer behavior, which can be leveraged to minimize churn and maximize customer lifetime value (CLV) post-acquisition. The contracts, therefore, are not just about present revenue, but about future, predictable cash flow under better management.

2. What US GAAP Actually Requires (Not What People Remember)

ASC 805 governs business combinations.

The sequence matters.

Step 1: Confirm It Is a Business

This sounds basic, but it is where many errors start.

If what you acquired does not meet the definition of a business, ASC 805 does not apply. No goodwill. No bargain gain. Different accounting model.

This distinction is often blurred in QuickBooks Onlineenvironments because everything looks like “an asset purchase.”

Step 2: Measure Consideration Transferred

This includes:

Cash paid

Equity issued

Fair value of assumed debt

It excludes:

Transaction costs

Future contingent consideration unless probable and measurable

Step 3: Measure Identifiable Assets and Liabilities at Fair Value

This is where bargain purchases emerge.

Assets often include:

Customer relationships

Developed technology

Trade names

Deferred revenue adjustments

Contractual rights

Liabilities include:

Deferred revenue at fair value

Litigation exposures

Contractual obligations

Step 4: Mandatory Reassessment (This Is Not Optional)

Before recognizing a gain, ASC 805 requires reassessment of:

Asset identification

Fair value measurements

Consideration transferred

This is the standard’s way of saying:

“If this looks too good to be true, check again.”

Only after reassessment can the gain be recorded.

Step 5: Immediate Recognition in Earnings

If the excess remains after reassessment, it must be recognized immediately in earnings.

Not deferred.

Not amortized.

Not parked in equity.

3. Why QuickBooks Online Makes This Harder Than It Should Be

QuickBooks Online assumes a simple world:

Assets equal cost.

Income is recurring.

Goodwill is positive.

None of that applies here.

There is:

No purchase price allocation module.

No fair value tracking.

No disclosure reminders.

No audit trail tying valuation to journals.

Everything depends on the accountant’s process discipline.

This is why bargain purchase gains often:

Get netted against assets.

Get recorded as “Other Income” with no explanation.

Get reversed during audit.

4. Core Journal Entry Mechanics (With Real Numbers)

Example Transaction

A SaaS company acquires a competitor.

Purchase price: $500,000

Fair value of assets acquired:

Cash: $80,000

Accounts receivable: $120,000

Developed technology: $300,000

Customer relationships: $220,000

Fair value of liabilities assumed:

Accounts payable: $70,000

Deferred revenue: $60,000

Net identifiable assets: $590,000

Bargain purchase gain: $90,000

Journal Entry in QuickBooks Online

Account | Debit | Credit |

Cash | 80,000 | |

Accounts Receivable | 120,000 | |

Developed Technology | 300,000 | |

Customer Relationships | 220,000 | |

Accounts Payable | 70,000 | |

Deferred Revenue | 60,000 | |

Cash (Purchase Price) | 500,000 | |

Gain on Bargain Purchase | 90,000 |

Key Observations

Assets are recorded at fair value, not cost.

No goodwill is recorded.

The gain is explicit and visible.

Nothing is netted.

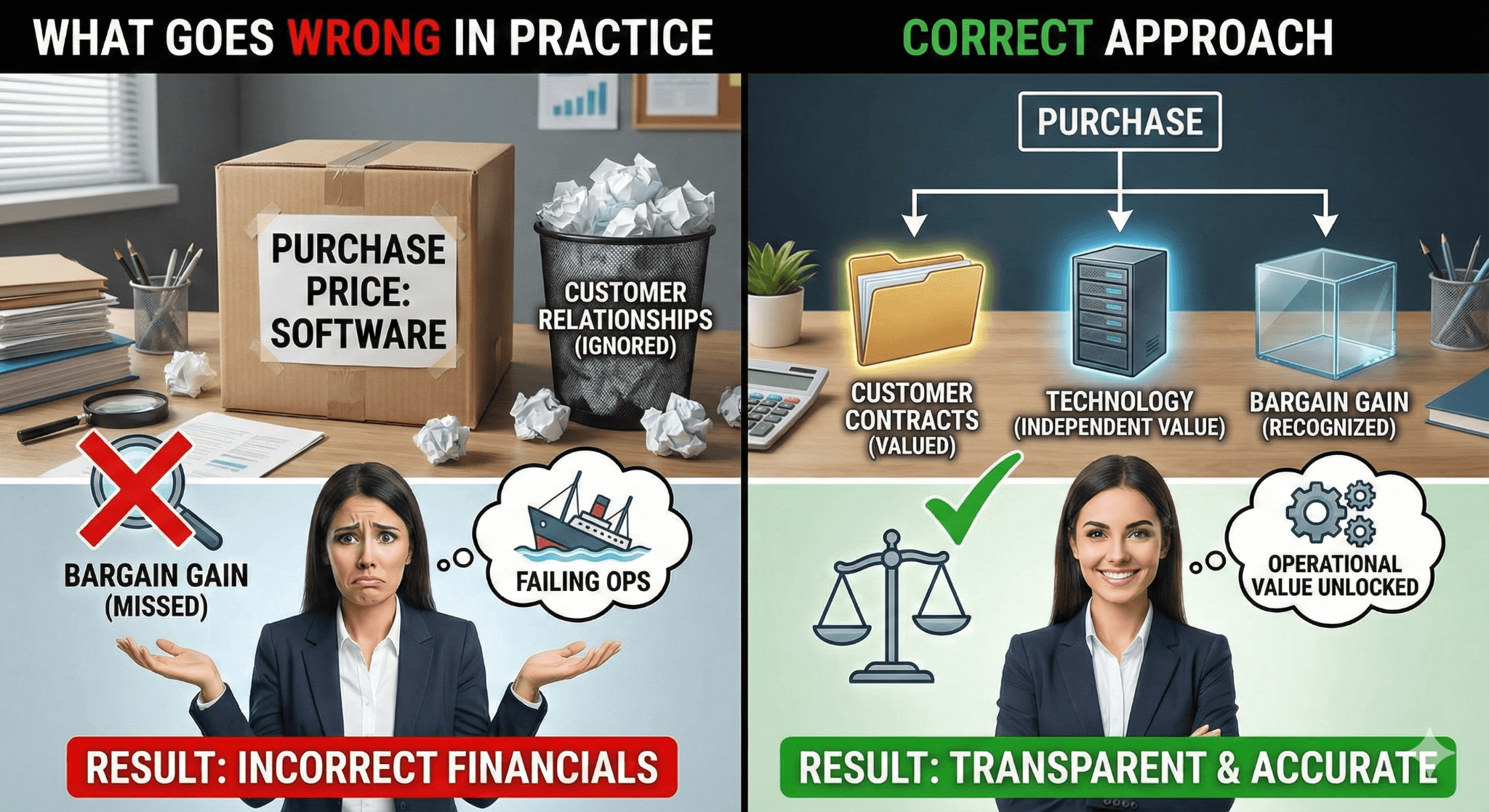

5. Case Scenario 1: Distressed SaaS Acquisition

A venture-backed SaaS company runs out of funding. Customer churn is high, but the technology remains solid. A competitor acquires the business quickly to absorb the customer base.

What Goes Wrong in Practice

The acquiring company records the purchase price as “Software.”

No customer relationships are recognized.

No bargain gain is identified.

Correct Approach

Identify the customer contracts.

Value the technology independently.

Record assets at fair value.

Recognize the gain transparently.

This often results in a bargain purchase even though the business was failing operationally.

6. Case Scenario 2: Asset Sale That Is Actually a Business

A founder sells “assets” including code, customer lists, and contracts. The buyer treats it as an asset purchase.

Under ASC 805, this can still qualify as a business if the inputs and processes are capable of producing outputs.

Failing to identify this correctly eliminates bargain purchase recognition entirely and misstates future amortization.

7. Case Scenario 3: Roll-Up Strategy Using QuickBooks Online

A holding company acquires five small SaaS companies over two years.

Each deal:

Is negotiated separately.

Has different valuation assumptions.

Results in either goodwill or bargain purchase.

QuickBooks Online requires:

Separate journal entries per acquisition.

External schedules for tracking balances.

Consistent classification across periods.

Controllers who do not standardize this process end up with inconsistent accounting and audit friction.

8. Presentation and Disclosure: Where Many Teams Fail

Income Statement Classification

The gain should be:

Clearly labeled.

Separated from operating income.

Treated as non-recurring in management reporting.

Disclosure Requirements

Disclosures should explain:

Why the gain occurred.

How fair value was determined.

That reassessment was performed.

In SMB audits, lack of disclosure often triggers reclassification or management letter comments.

9. KPI Distortion and Management Reporting

Bargain purchase gains inflate:

EBITDA

Net income

Gross margin (if misclassified)

Most CFOs adjust these out for:

Board reporting

Compensation metrics

Forecast comparability

The accounting remains GAAP-compliant, but operational metrics exclude the gain.

10. Audit Reality: What Auditors Actually Test

Auditors focus on:

Valuation support

Reassessment documentation

Classification consistency

Disclosure completeness

They do not assume fraud.

They assume error.

Teams that cannot reconstruct assumptions months later often face proposed adjustments.

11. Controls and Repeatability

Strong teams implement:

Acquisition accounting checklists

Standard journal templates

Centralized valuation documentation

Approval workflows for assumptions

This is where structured financial platforms quietly help by connecting schedules, assumptions, and entries without replacing accounting judgment.

Risks and How Teams Mitigate Them

Risk | Mitigation |

Auditor rejects gain | Reassessment memo |

Misclassification | Separate income line |

KPI distortion | Management adjustments |

Lost documentation | Central repository |

Inconsistent treatment | Standard templates |

Frequently Asked Questions

Can a bargain purchase be amortized?

No. It is recognized immediately.

Is this taxable?

Often no, but tax treatment differs.

Can this occur in asset deals?

Only if the asset set qualifies as a business.

Is this aggressive accounting?

No, when supported properly.

Why do auditors dislike these gains?

Because they are rare and judgment-heavy.

Glossary

Bargain Purchase: Fair value exceeds purchase price.

ASC 805: US GAAP business combinations standard.

Fair Value: Exit price under market participant assumptions.

Reassessment: Mandatory valuation review.

Negative Goodwill: Prohibited concept under US GAAP.

Final Thought

A gain on bargain purchase is not a loophole. It is not an accounting trick. It is a reflection of economic reality in imperfect markets. The problem is not the standard. The problem is execution, especially in systems like QuickBooks Online that were never designed for acquisitions.

Teams that approach this carefully, document assumptions clearly, and treat the gain with appropriate skepticism rarely face audit issues. Teams that rush or obscure the gain almost always do.