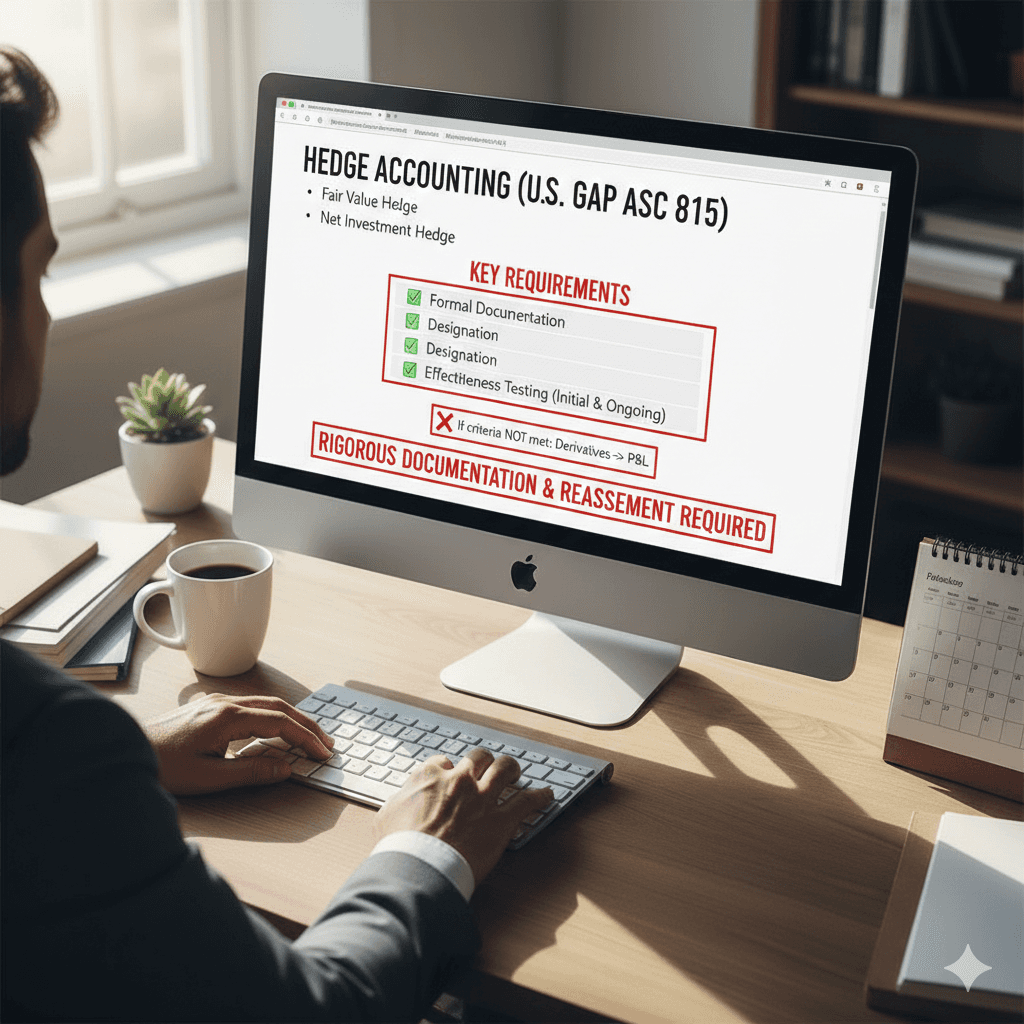

Hedge accounting aligns the financial reporting of derivatives with the economic purpose of risk mitigation.

Under U.S. GAAP (ASC 815), entities can apply fair value, cash flow, or net investment hedge accounting.

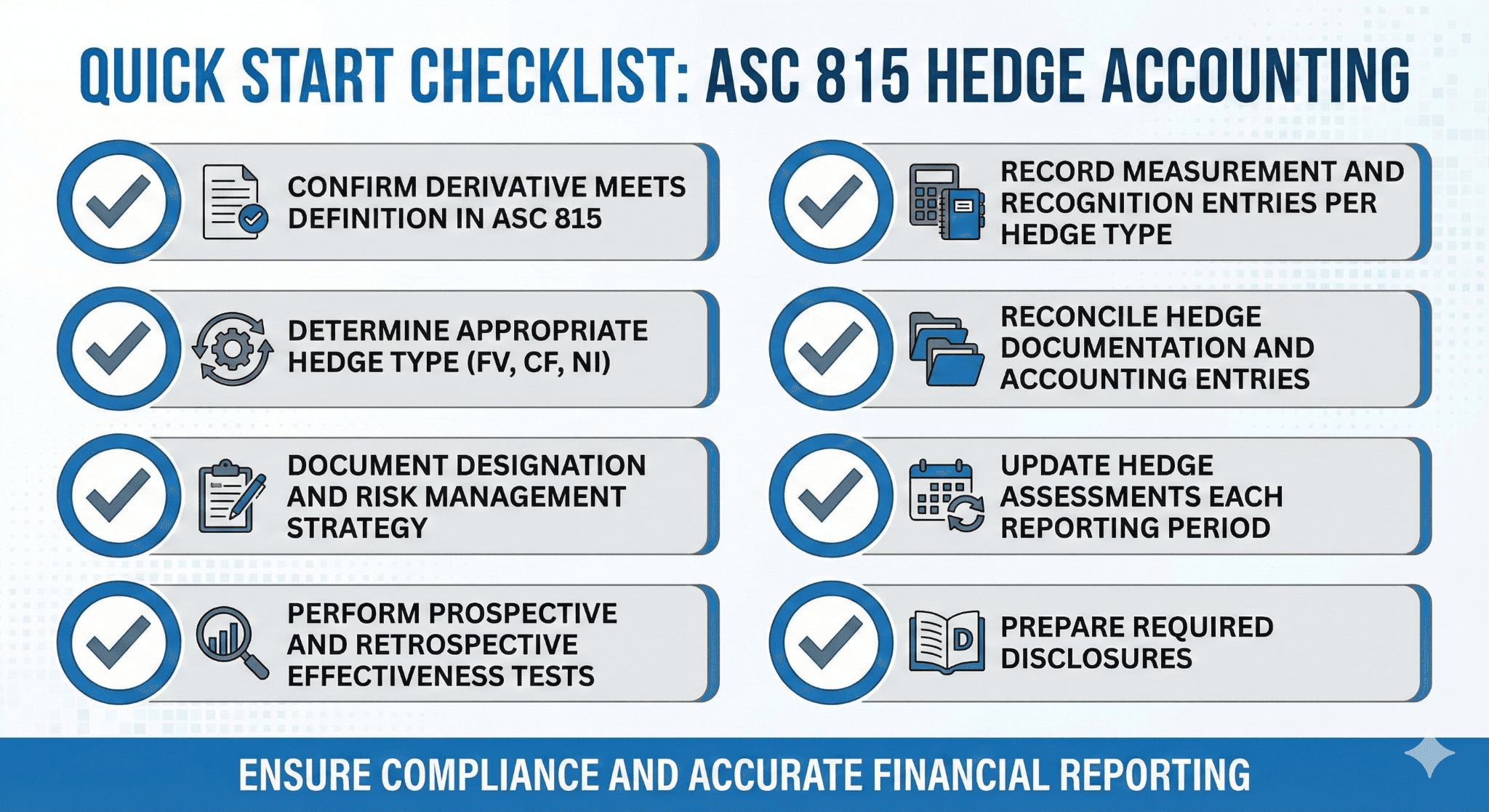

Hedge relationships must be formally documented, designated, and tested for effectiveness.

If hedge accounting criteria are not met, derivatives are recorded at fair value through profit and loss.

Practical application requires rigorous documentation and periodic reassessment

.

Executive Summary

Hedge accounting is a specialized set of accounting principles under US GAAP designed to link the timing of gains and losses on hedging instruments with the period in which the gains and losses of the hedged item affect earnings. The core guidance resides in Accounting Standards Codification Topic 815. Hedge accounting is optional, not mandatory. Entities elect hedge accounting only when specific criteria are satisfied.

Without hedge accounting, changes in the fair value of derivatives are recognized immediately in profit and loss each reporting period, which can cause significant volatility that does not align with an entity’s economic risk management activities. To qualify for hedge accounting, a formal designation and documentation of the hedging relationship must exist at inception. The hedging relationship must be highly effective in offsetting changes in the fair value or cash flows of a hedged item.

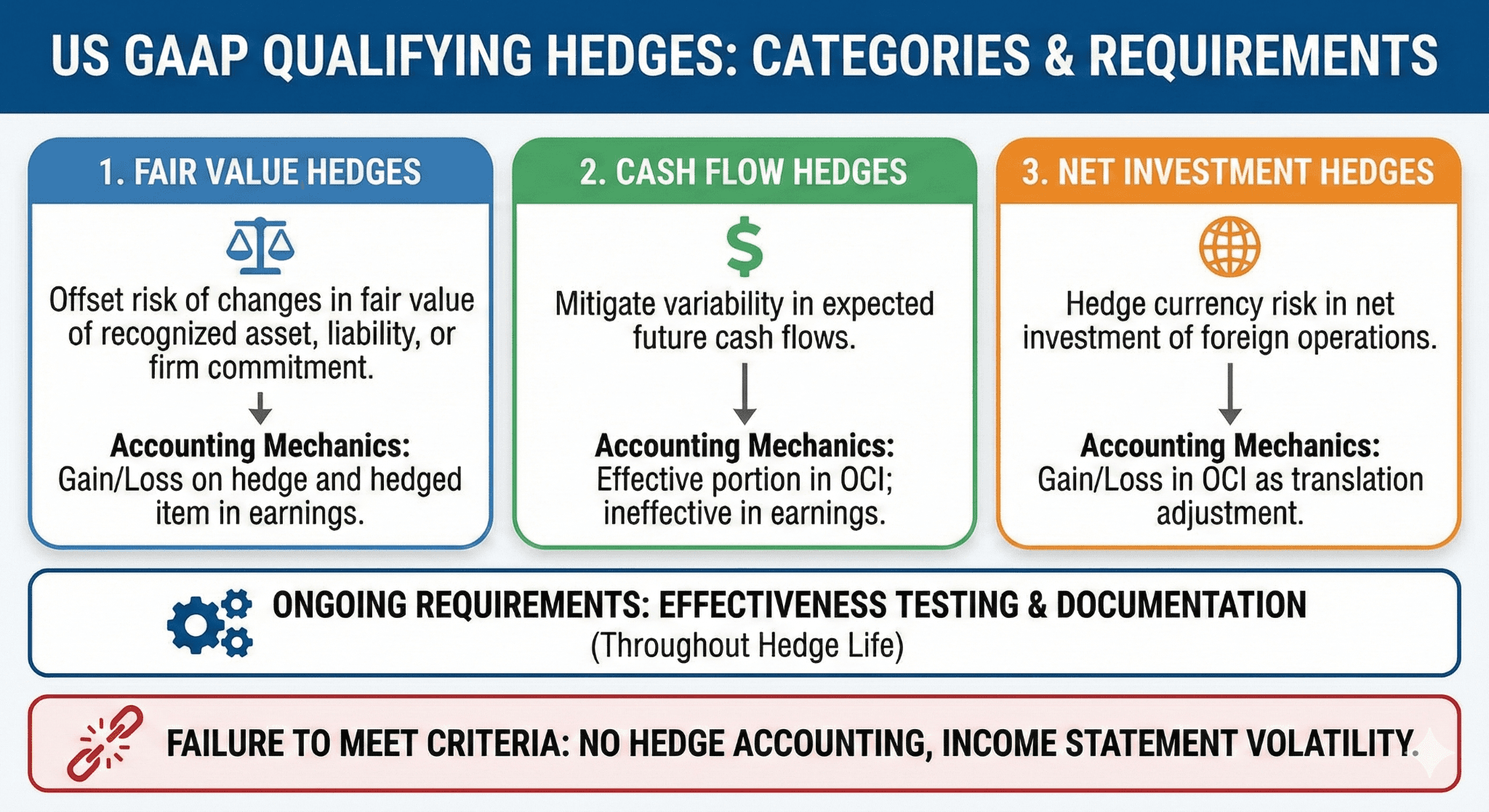

Under US GAAP, qualifying hedges generally fall into three categories: fair value hedges, cash flow hedges, and net investment hedges. Each type has distinct accounting mechanics and presentation requirements. Entities must perform ongoing effectiveness testing and maintain documentation to support eligibility throughout the hedge life. Failure to meet the qualifying criteria will preclude hedge accounting and expose an entity to income statement volatility unrelated to its core business performance.

1. What is Hedge Accounting?

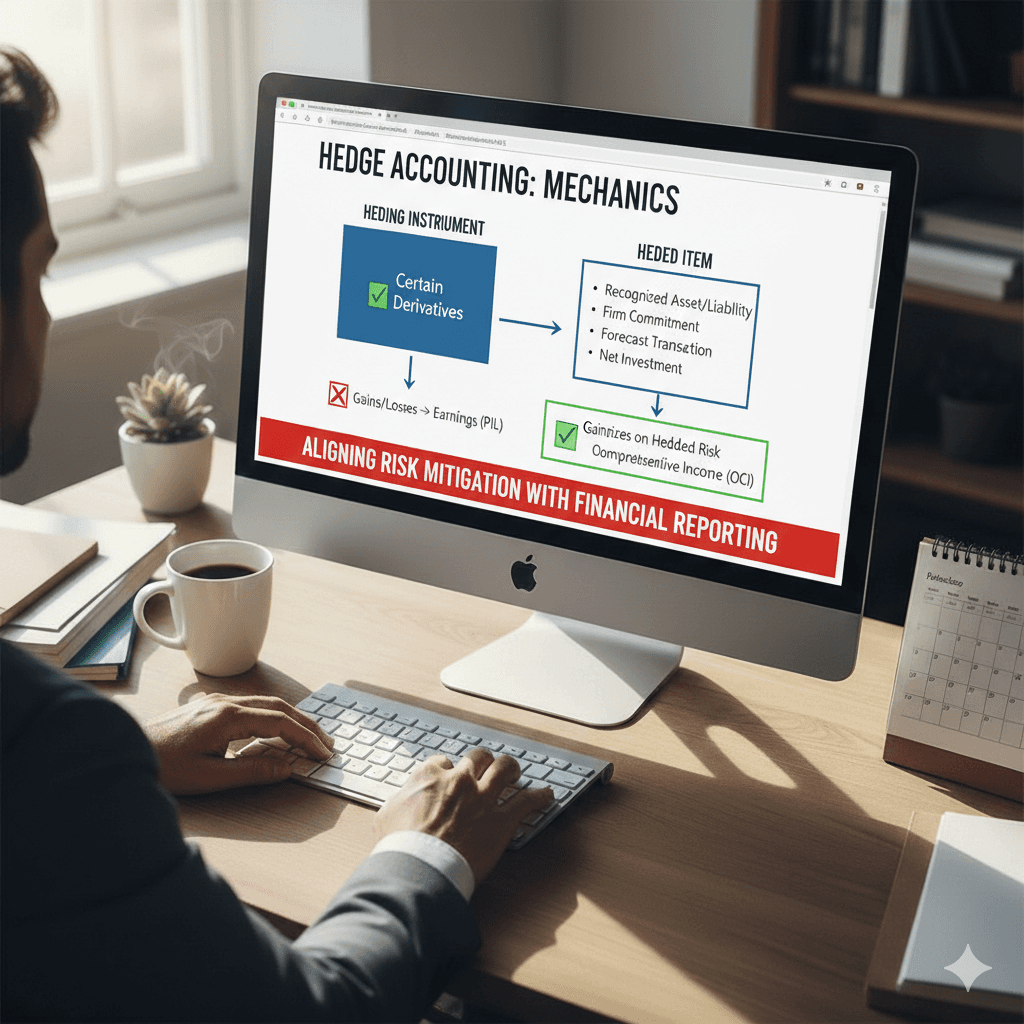

Hedge accounting is a measurement and presentation approach that synchronizes the accounting effects of an entity’s risk management strategy with the timing of the economic effects of the hedged exposures. Hedge accounting is necessary because derivatives, such as forwards, futures, swaps, and options, must be recorded at fair value under U.S. GAAP. Without special accounting treatment, these fair value gains or losses often produce periodic income statement volatility that does not reflect an entity’s economic risk mitigation.

Under Hedge Accounting:

Certain derivatives are designated as hedging instruments.

The hedged item is a recognized asset, liability, firm commitment, forecast transaction, or net investment.

Gains and losses on hedging instruments and the hedged risk are recognized in earnings or other comprehensive income (OCI) depending on hedge type.

If hedge accounting is not designated or fails the qualifying criteria, all changes in derivatives’ fair value are recognized immediately in profit and loss.

2. Why Hedge Accounting Matters: The Economic and Reporting Case

In practice, entities use derivatives to manage exposures such as interest rate risk, foreign currency risk, commodity price risk, and credit risk. Hedge accounting helps ensure that accounting results mirror an entity’s economic risk management activities.

For example:

A company hedging its forecasted cash flows with a derivative would prefer changes in the derivative’s fair value to be recognized in the same periods the hedged sales or costs affect earnings.

A firm hedging the fair value of a fixed-rate debt instrument wants the derivative’s gain or loss to offset the changes in the carrying amount of that debt.

Without hedge accounting, entities would show disproportionate income statement volatility in periods where derivative fair values change, regardless of whether the hedged exposure impacts earnings in those periods.

3. US GAAP Hedge Models

Under ASC 815, there are three principal hedge types:

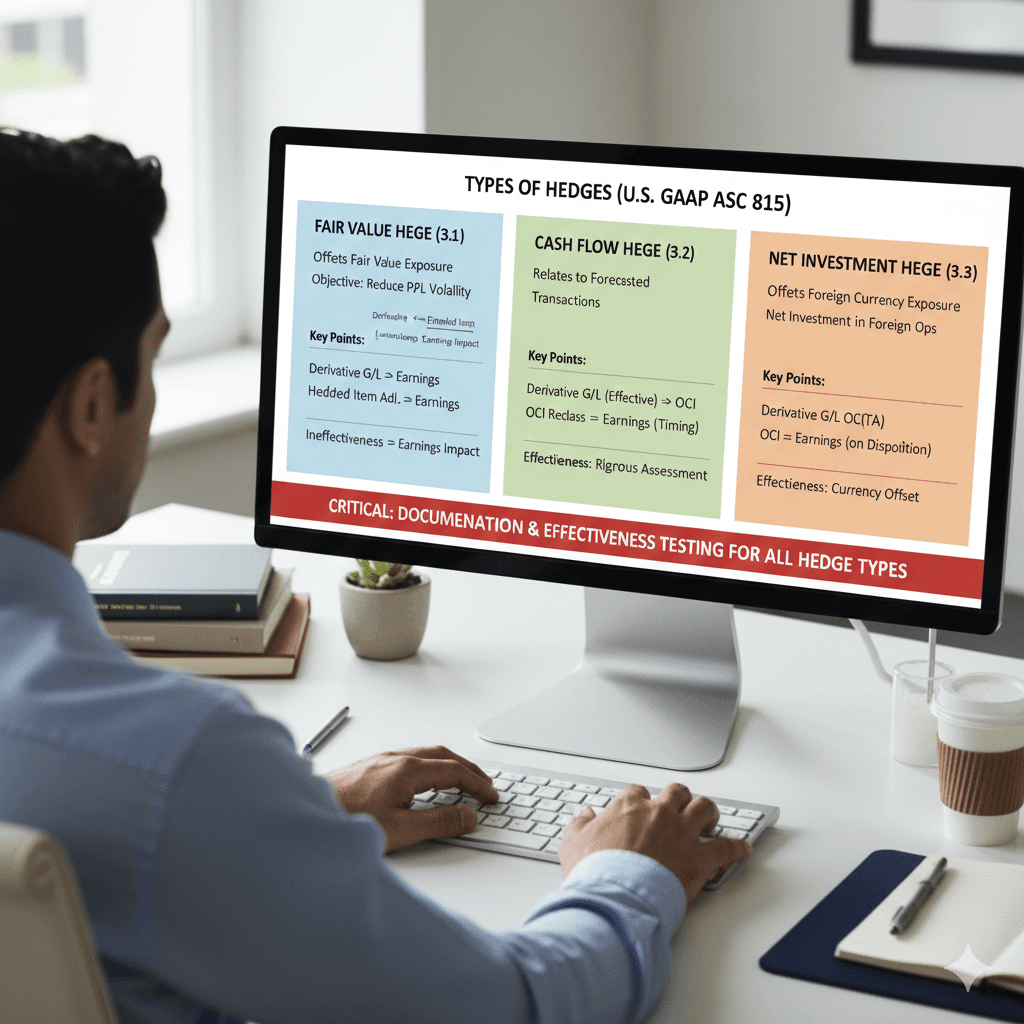

3.1 Fair Value Hedges

A fair value hedge offsets exposure to changes in the fair value of a recognized asset, liability, or firm commitment related to a particular risk (such as interest rate risk). The objective is to reduce income statement volatility by adjusting the carrying value of the hedged item for the change attributable to the hedged risk.

Key Points

Changes in fair value of both the hedging instrument and the hedged item attributable to the hedged risk are recognized in earnings.

The carrying amount of the hedged item is adjusted for the fair value changes related to the hedged risk.

Ineffectiveness (difference between derivative gains/losses and hedged item changes) is also recorded in current-period earnings.

3.2 Cash Flow Hedges

A cash flow hedge offsets variability in cash flows of an existing asset or liability or a highly probable forecast transaction (such as future interest payments or foreign revenue).

Key Points

Changes in fair value of the hedging instrument that are effective are initially reported in OCI.

Amounts in OCI are reclassified into earnings in the same period in which the hedged item affects earnings.

Hedge effectiveness must be assessed conclusively.

3.3 Net Investment Hedges

A net investment hedge mitigates foreign currency exposure in a net investment in a foreign operation (e.g., a subsidiary with a foreign functional currency).

Key Points

Changes in fair value of the hedging instrument are recorded in the cumulative translation adjustment (CTA) component of OCI until disposition of the foreign operation.

Assessment of effectiveness similarly must demonstrate that the derivative offsets the net investment currency exposure.

4. Hedge Effectiveness: Criteria and Testing Procedures

For hedge accounting to apply, entities must demonstrate that the derivative and hedged item have a high degree of offset. Under US GAAP, hedge effectiveness generally requires that the cumulative change in the value of the hedging instrument offsets between 80 percent and 125 percent of the cumulative change in the value of the hedged item.

4.1 Prospective Testing

Prospective testing evaluates the expectation that the hedge will be effective for the remaining term. Methods include the dollar-offset or regression analysis. If the hedge does not meet criteria, hedge accounting cannot be designated or must be rebalanced or dedesignated.

4.2 Retrospective Testing

Retrospective testing assesses how effective the hedge was during the period just concluded. If effectiveness falls outside the range, documentation and reassessment are required.

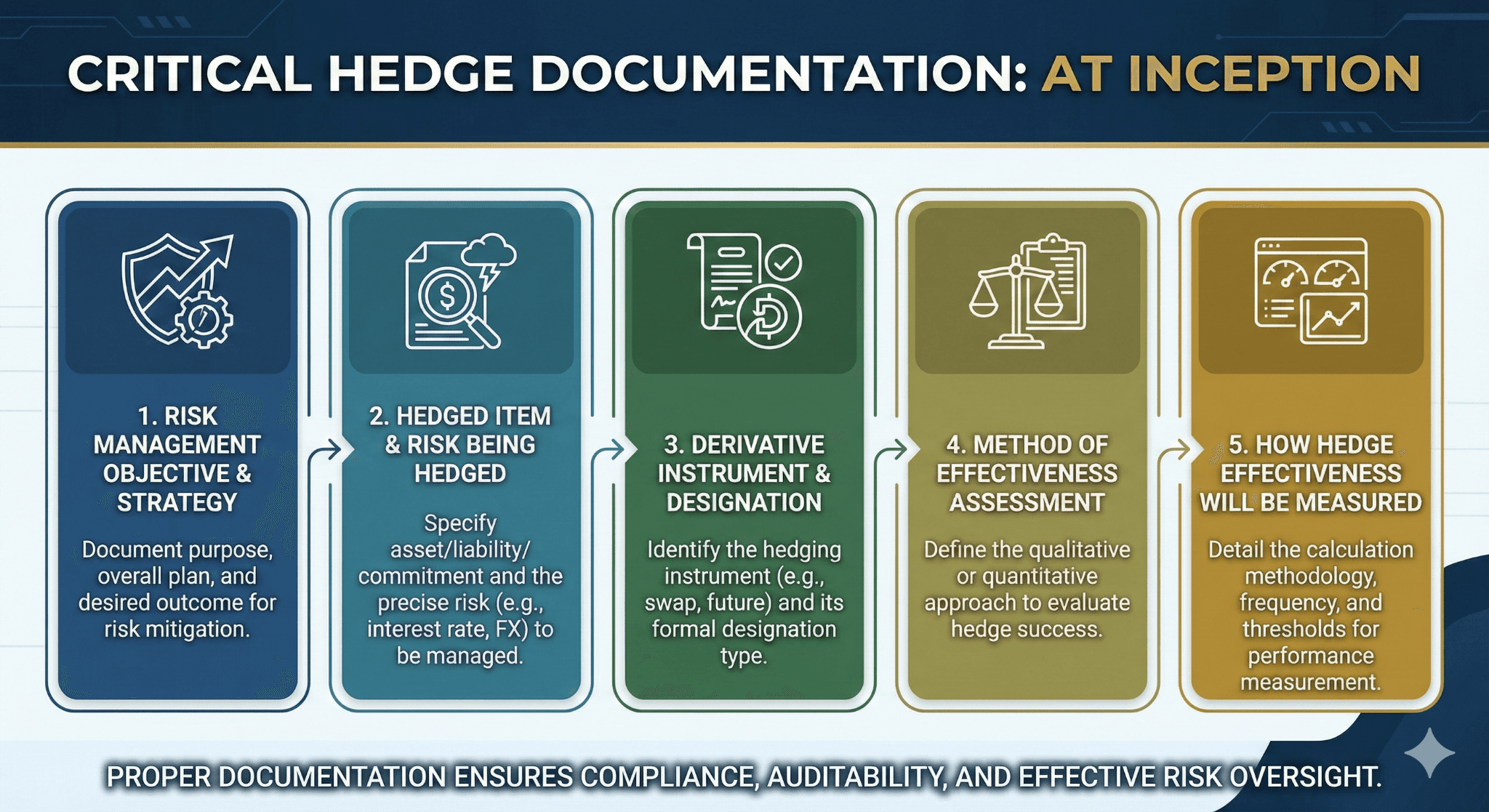

5. Documentation and Qualification Requirements

Proper documentation is critical. At hedge inception, entities must document:

Risk management objective and strategy.

Hedged item and risk being hedged.

Derivative instrument and designation.

Method of effectiveness assessment.

How hedge effectiveness will be measured.

Documentation must be completed before or at the time the hedge designation occurs. Periodic updated effectiveness assessments and results must be retained to support continuing qualification.

6. Practical Application and Journal Entries

Practical hedge accounting requires precise accounting entries based on the type of hedge.

Fair Value Hedge Example (Interest Rate Risk)

Hedge: Fixed-rate debt instrument hedged with an interest rate swap.

Derivative fair value gain: $120,000.

Hedged item fair value loss: $118,000 (risk attributable).

Entries

Recognize derivative gain:Debit Derivative Asset 120,000

Credit Gain on Hedging Instrument 120,000

Adjust hedged item carrying value:Debit Loss on Hedged Item 118,000

Credit Debt Carrying Amount 118,000

Net ineffectiveness ($2,000) in income:Debit Loss on Hedged Instrument 2,000

Credit Gain on Hedge 2,000

Cash Flow Hedge Example (Forecast Transaction)

Hedge instrument changes fair value: $50,000 effective portion.

Effective portion recorded in OCI and reclassified when hedged cash flow affects earnings.

Entry at Measurement Date

Debit OCI – Effective Portion 50,000

Credit Derivative Liability 50,000

Later reclassification to earnings when forecast transaction occurs is required.

7. Operating and Disclosure Considerations

Entities must consider:

Ongoing effectiveness testing frequency (at least quarterly).

Rebalancing or dedesignation triggers.

Required disclosures including risk management strategy, types of hedges, and effectiveness results.

Tool / Workflow Comparison

Item | Hedge Accounting | No Hedge Accounting |

Derivative fair value changes | Matched to hedged risk | Recognized in P&L immediately |

Income volatility | Reduced | Potentially volatile |

OCI usage | Yes (CF and NI) | No |

Complexity | High | Low |

Mini-Case: Foreign Currency Forecast Hedges

A U.S. importer expects EUR-denominated purchases of €1M over next 6 months. To hedge EUR/USD risk, the company enters into a forward contract.

Hedge Strategy

Designate a cash flow hedge.

Document forecast transaction, risk management strategy, and testing method.

Changes in fair value of the forward contract recognized in OCI.

On purchase, reclassify OCI to expense.

Without hedge accounting, all fair value changes would hit income immediately, distorting margins unrelated to core business results.

Risks & Mitigations

Risk | Mitigation |

Hedge ineffectiveness | Robust testing and documentation |

Misclassification of hedge type | Detailed initial assessment |

Missing disclosures | Hedge accounting disclosure checklist |

Failing effectiveness range | Rebalance or redesignate quickly |

FAQ

Is hedge accounting mandatory?

No. Entities elect it when they meet qualifying criteria.

Can a hedge be designated after inception?

Documentation must occur at or before designation.

Do all derivatives qualify?

Only if the hedging relationship meets eligibility and effectiveness criteria.

What happens if a hedge fails effectiveness testing?

Hedge accounting cannot be applied until it meets criteria again.

Glossary

Derivative Instrument: A financial contract whose value is derived from underlying price changes.

Fair Value Hedge: Hedge that offsets exposure to fair value changes of an item.

Cash Flow Hedge: Hedge that offsets variability in forecast cash flows.

Net Investment Hedge: Hedge of foreign currency exposure of a net investment.

Other Comprehensive Income (OCI): Portion of equity where certain gains/losses are temporarily recorded.