A bargain purchase almost always creates deferred tax complexity.

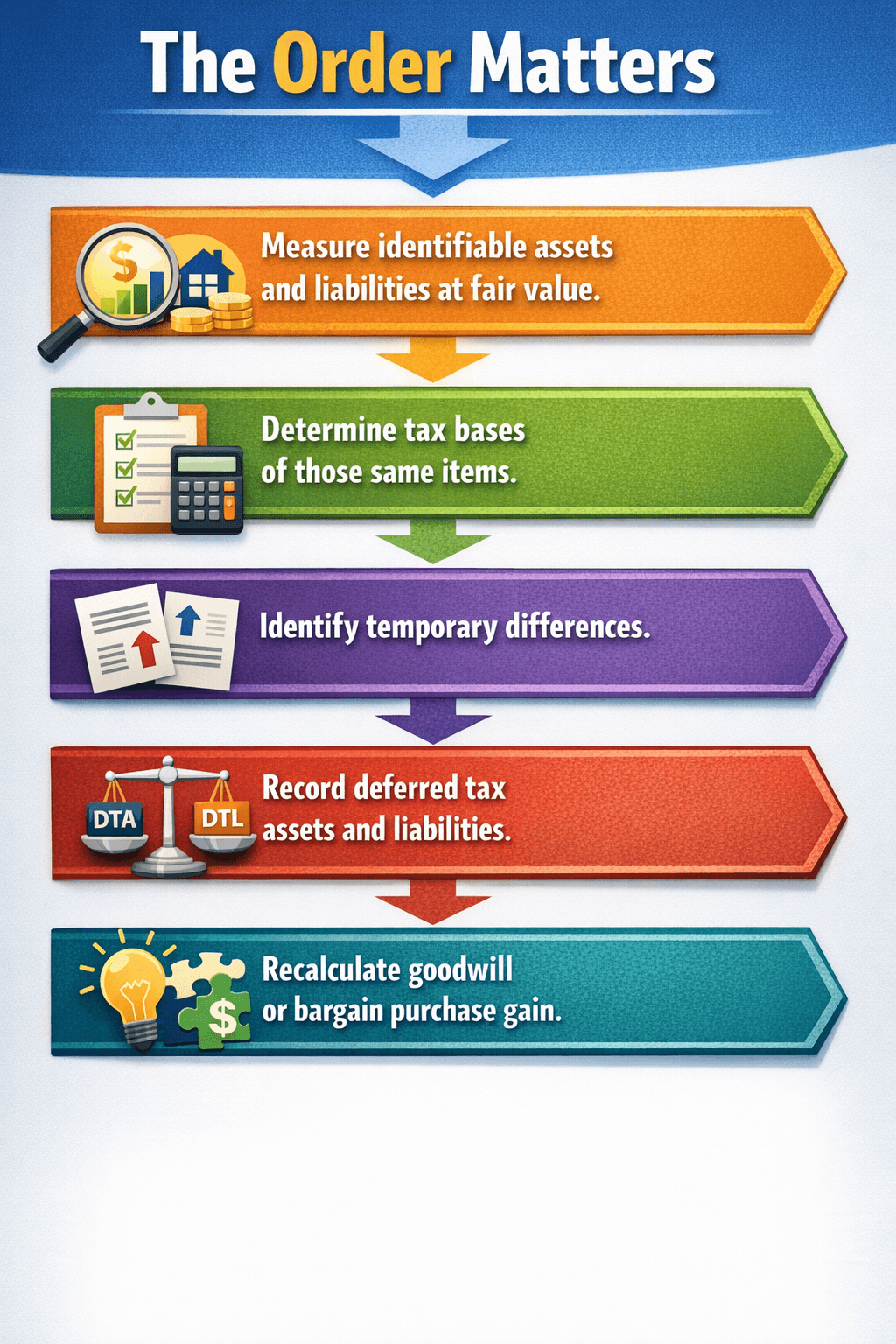

Deferred taxes are measured after fair value allocation, not before.

Deferred tax liabilities often reduce or eliminate the bargain gain.

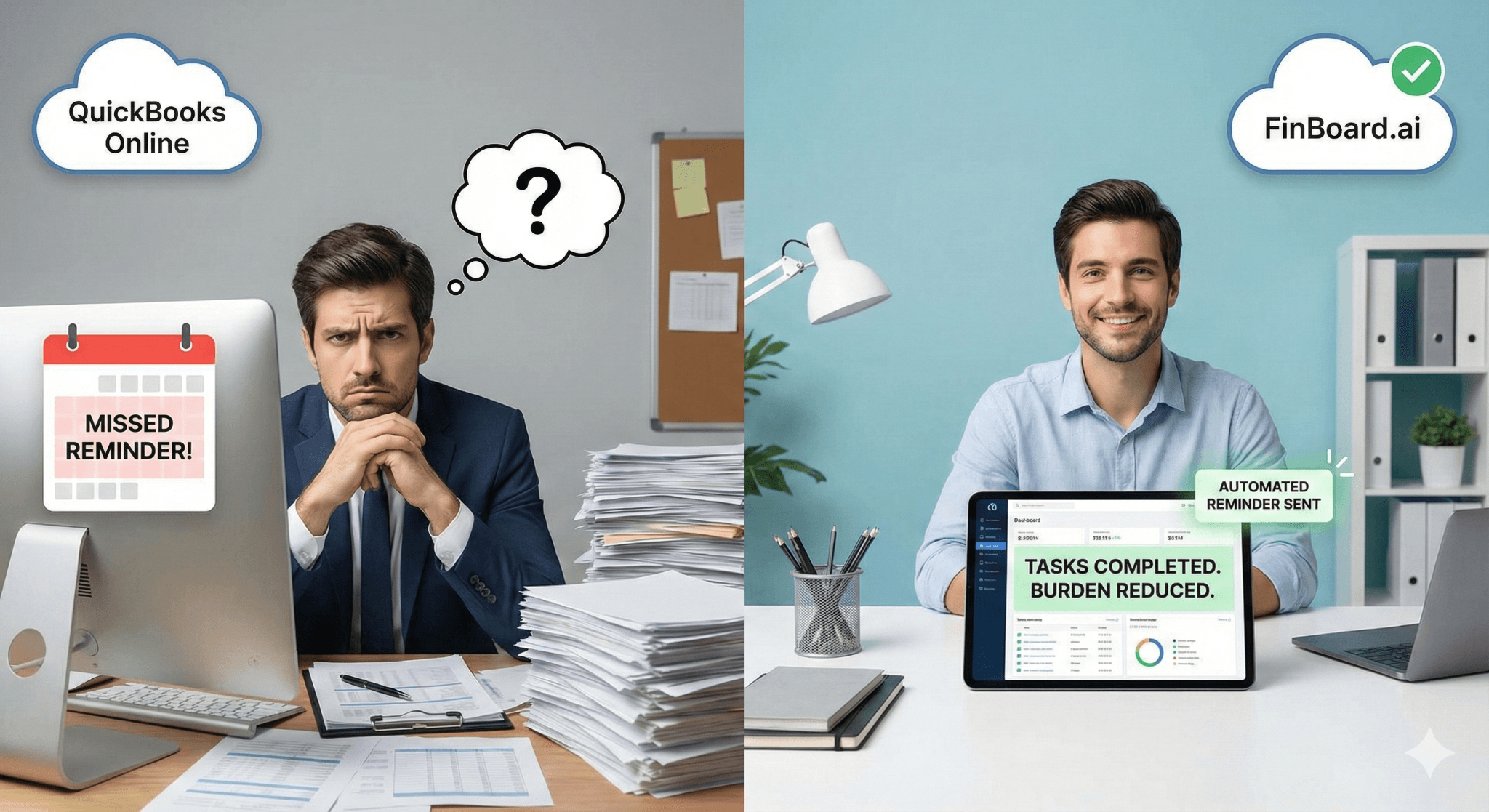

QuickBooks Online does not automate deferred tax logic.

Tools like FinBoard.ai has inbuilt drivers for it.

Missing deferred taxes is the most common audit adjustment in bargain purchases.

Documentation matters more than journal mechanics.

Executive Summary

A gain on bargain purchase rarely survives contact with deferred taxes.

Many accounting teams identify a bargain purchase correctly, record the gain, and move on. Months later, auditors revisit the transaction and ask a simple question: “Where are the deferred taxes?” At that point, the reported gain often shrinks or disappears entirely.

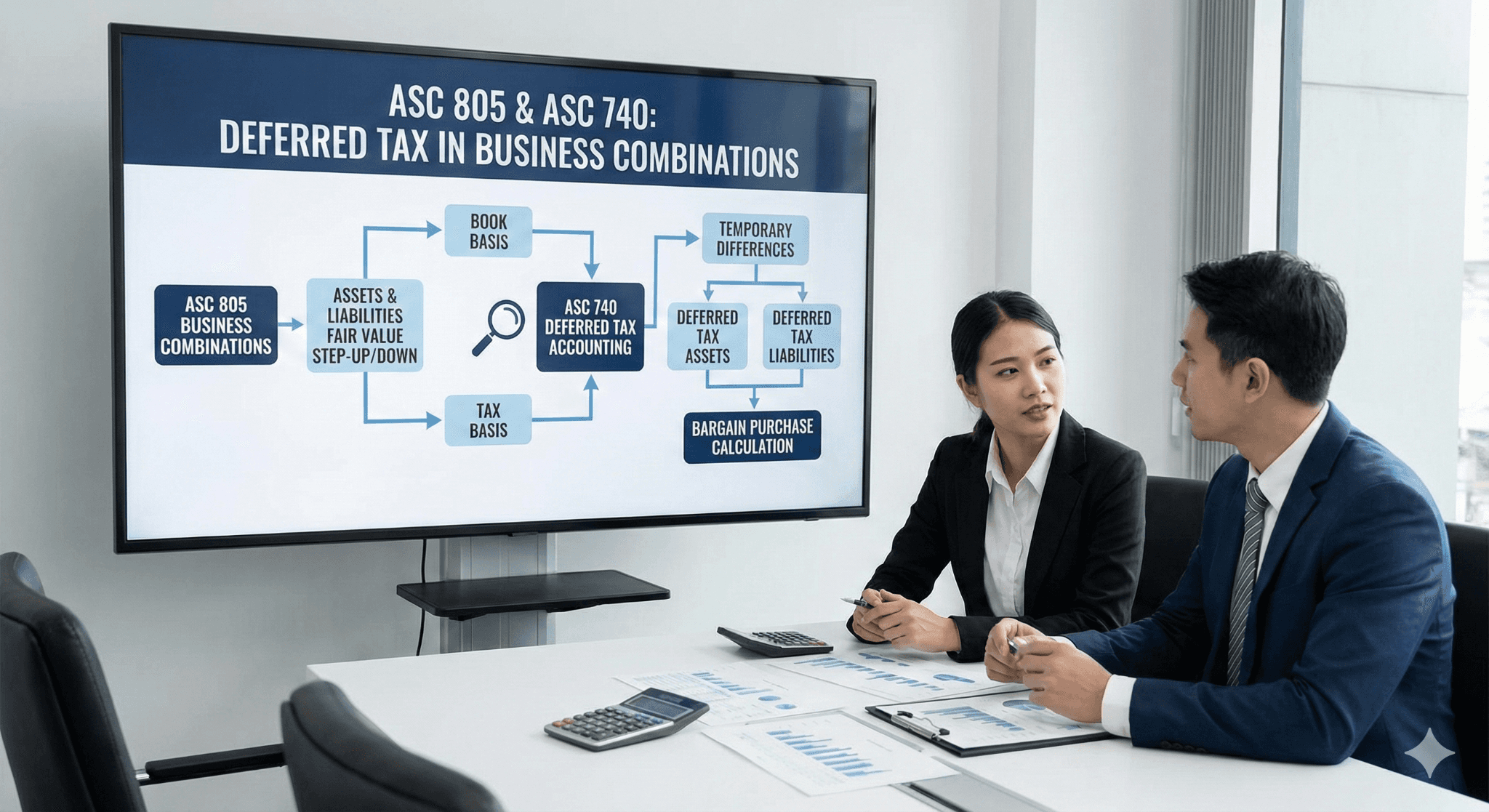

Deferred tax accounting under ASC 740 interacts directly with ASC 805 business combinations. When assets and liabilities are stepped up or down to fair value, temporary differences arise between book and tax bases. Those differences must be recognized immediately through deferred tax assets or liabilities. The impact flows straight into the bargain purchase calculation.

QuickBooks Online makes this harder than it should be. There is no deferred tax engine, no concept of tax basis, and no acquisition workflow. Deferred taxes exist only if the accountant explicitly calculates and records them.

This article explains, in detail, how deferred taxes arise in a bargain purchase, how they affect the gain calculation, how to record them properly in QuickBooks Online, and how auditors evaluate the results. It uses real SaaS-focused scenarios and highlights where teams commonly get it wrong.

1. Why Deferred Taxes Matter More in Bargain Purchases Than Goodwill Deals

In a typical acquisition with goodwill, deferred taxes are important, but they rarely change the headline narrative. Goodwill absorbs a lot of noise.

In a bargain purchase, there is no goodwill buffer.

Every dollar of deferred tax liability reduces the gain dollar-for-dollar.

This is why bargain purchase gains often look large initially and then collapse after proper tax accounting.

The Core Principle

Under US GAAP:

Assets and liabilities are recorded at fair value for book purposes.

Tax bases generally remain unchanged.

The difference creates temporary differences.

Temporary differences create deferred tax assets or liabilities.

Those deferred taxes are part of the net identifiable assets calculation.

2. The ASC 805 and ASC 740 Interaction (Without the Legalese)

ASC 805 tells you how to measure assets and liabilities in a business combination.

ASC 740 tells you how to account for the tax consequences of those measurements.

They operate sequentially.

Many teams reverse steps 2 and 3 or skip them entirely.

3. Why Deferred Taxes Are Often Missed in QuickBooks Online

QuickBooks Online was not designed for tax basis accounting.

There is:

No parallel tax ledger.

No deferred tax module.

No fair value tracking.

Deferred taxes exist only in:

Spreadsheets

Workpapers

The accountant’s head

If the accountant forgets, QuickBooks Online will not remind them.Hnnce users prefer tools like FinBoard.ai which reduces their burden.

4. Common Temporary Differences in SaaS Bargain Purchases

Let us get concrete.

4.1 Developed Technology

Book treatment:

Recorded at fair value.

Amortized over useful life.

Tax treatment:

Often zero basis if internally developed.

Or amortized differently under tax rules.

Result:

Deferred tax liability.

4.2 Customer Relationships

Book:

Recognized and amortized.

Tax:

Often no tax basis.

Result:

Deferred tax liability.

4.3 Deferred Revenue

Book:

Recorded at fair value, often discounted.

Revenue recognized post-acquisition.

Tax:

Revenue may already be taxed or taxed differently.

Result:

Deferred tax asset or liability depending on structure.

4.4 Net Operating Losses (NOLs)

Book:

Deferred tax asset if realizable.

Tax:

Subject to limitations.

Result:

Deferred tax asset, often with valuation allowance.

5. Case Scenario 1: Bargain Purchase That Disappears After Deferred Taxes

Facts

A SaaS acquirer purchases a distressed competitor.

Purchase price: $400,000

Fair value of identifiable assets:

Cash: $50,000

AR: $100,000

Developed technology: $300,000

Customer relationships: $250,000

Liabilities:

AP: $80,000

Deferred revenue: $70,000

Net identifiable assets: $550,000

Initial bargain gain: $150,000

Deferred Tax Analysis

Developed technology and customer relationships have no tax basis.

Temporary difference: $550,000

Assume 25% tax rate.

Deferred tax liability: $137,500

Revised Bargain Purchase Calculation

Net assets after deferred taxes:

$550,000 − $137,500 = $412,500

Purchase price: $400,000

Final bargain gain: $12,500

What Changed

The economics did not change.

The accounting became complete.

6. How to Record Deferred Taxes in QuickBooks Online

QuickBooks Online does not care why an entry exists.

You must build the logic outside and bring in clean journal entries.

Journal Entry Example

Account | Debit | Credit |

Deferred Tax Expense | 137,500 | |

Deferred Tax Liability | 137,500 |

This entry reduces net assets and flows into the bargain purchase calculation.

7. Case Scenario 2: Deferred Tax Asset from Deferred Revenue

Facts

Acquirer assumes deferred revenue with a book fair value of $60,000.

Tax basis: $100,000 (already taxed).

Temporary difference: $40,000

Tax rate: 25%

Deferred tax asset: $10,000

This increases net identifiable assets and may increase the bargain gain.

This surprises many teams.

8. Valuation Allowance Considerations

Deferred tax assets are not guaranteed.

ASC 740 requires evaluation of realizability.

In distressed acquisitions:

Loss history may require valuation allowances.

Auditors scrutinize optimism.

Valuation allowances reduce deferred tax assets and reduce bargain gains.

9. Case Scenario 3: NOLs and Section 382 Limitations

Acquired company has $2 million in NOLs.

Book DTA at 25%: $500,000

Section 382 limits usage to $50,000 per year.

Only a portion is realizable.

Deferred tax asset recorded: $125,000

Valuation allowance: $375,000

Net impact on bargain purchase is far smaller than expected.

10. Why Auditors Focus Heavily on Deferred Taxes in Bargain Purchases

Auditors assume:

Valuation bias.

Incomplete tax analysis.

Overstated gains.

They will ask:

Tax basis schedules.

Rate support.

Valuation allowance memos.

Lack of documentation almost guarantees adjustments.

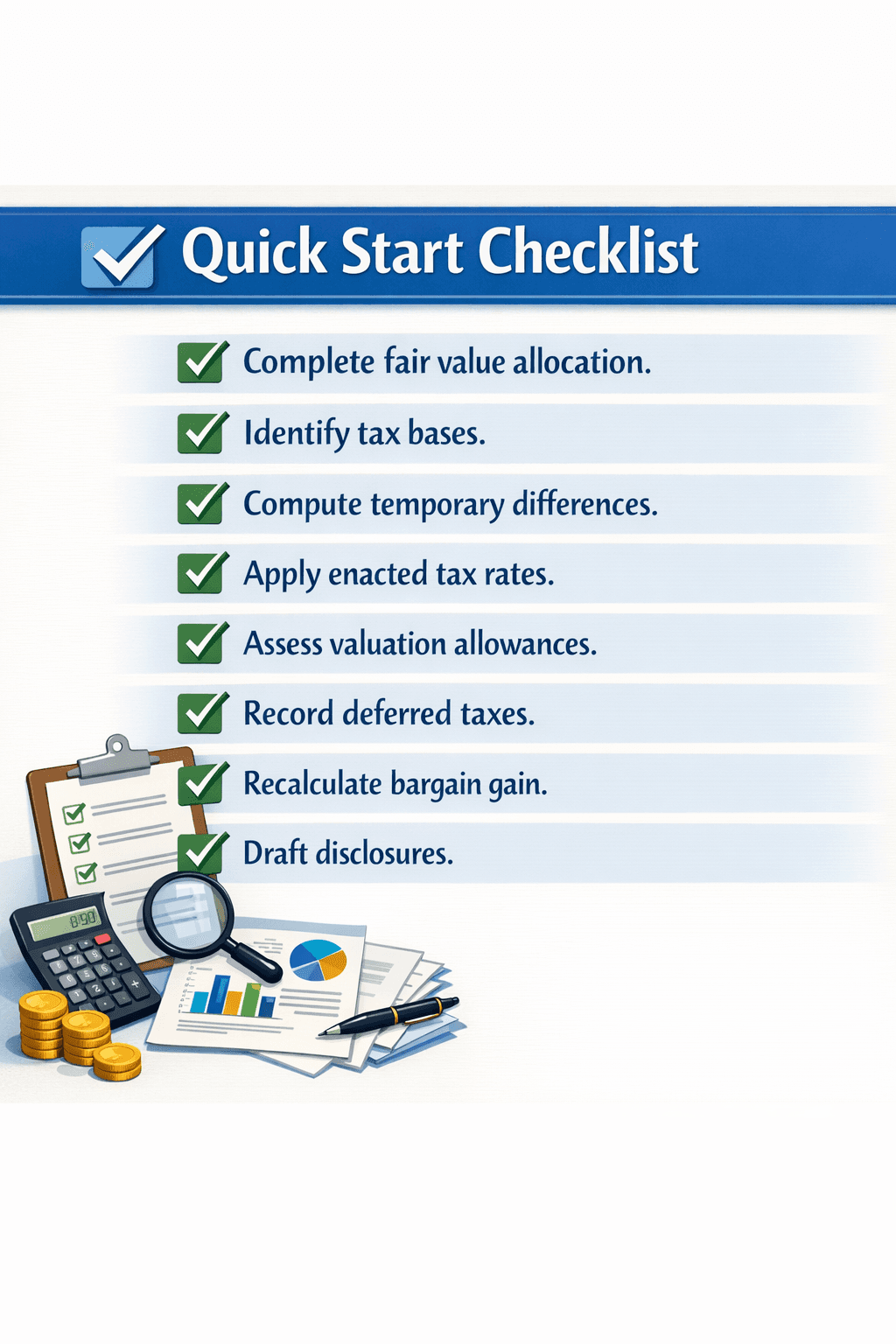

11. Disclosure Implications

Disclosures should explain:

Nature of temporary differences.

Impact on bargain gain.

Significant judgments.

Inadequate disclosures trigger comments even if numbers are correct.

12. Management Reporting vs GAAP Reporting

Many CFOs exclude:

Bargain gains

Deferred tax impacts

from operational metrics.

This is acceptable internally but GAAP numbers must remain intact.

13. Internal Controls That Prevent Surprises

Strong teams:

Build deferred tax schedules alongside valuation.

Reconcile book-tax differences early.

Review with tax advisors before close.

This prevents late-stage audit issues.

Risks and Mitigations

Risk | Mitigation |

Overstated gain | Deferred tax analysis |

Audit adjustments | Early documentation |

Misclassified DTAs | Valuation allowance review |

QuickBooks Online limitations | External schedules |

FAQ

Can deferred taxes eliminate a bargain gain entirely?

Yes, often.

Are deferred taxes optional?

No.

Do tax elections matter?

Yes, significantly.

Can QuickBooks Online handle this automatically?

No.

Should tax advisors be involved?

Almost always.

Glossary

ASC 740: Income taxes accounting standard.

Temporary Difference: Book-tax basis difference.

Deferred Tax Liability: Future taxable amount.

Deferred Tax Asset: Future tax benefit.

Valuation Allowance: Reduction of DTA for non-realizability.

Final Thought

Most bargain purchase gains look impressive until deferred taxes enter the picture. This is not a failure of valuation or negotiation. It is the natural result of reconciling book economics with tax reality.

Teams that understand this upfront avoid embarrassment later. Teams that ignore deferred taxes almost always restate the story during audit.

Deferred tax accounting is not optional, and in bargain purchases, it is decisive.