Self-funded insurance breaks QuickBooks Online’ default payroll logic.

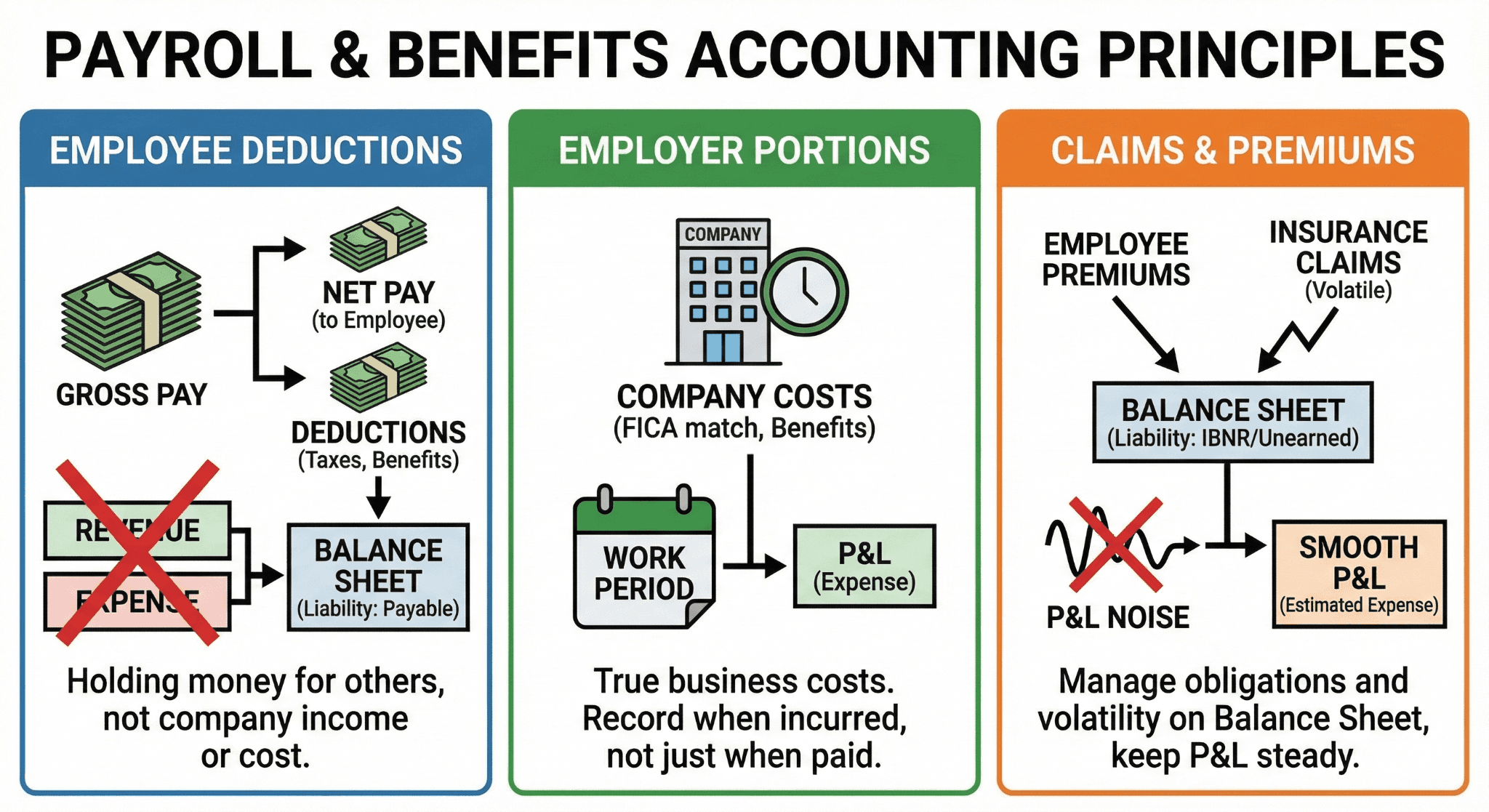

Employee deductions are not revenue and not expenses.

Employer portions are expenses, but timing matters.

Claims and employee premiums create liabilities, not P&L noise.

Correct mapping is the foundation for GAAP-compliant self-funded accounting.

Executive Summary

QuickBooks Online payroll was built for fully insured plans. Self-funded insurance turns that design assumption upside down. Instead of paying fixed premiums to an insurer, the employer pays claims, admin fees, and stop-loss premiums while temporarily holding employee contributions.

That distinction matters.

Under US GAAP, employee payroll deductions for self-funded insurance are plan assets or plan liabilities, not income. Employer portions are compensation expense, but only to the extent benefits are earned during the period. Claims paid are settlements of liabilities, not new expenses if already accrued.

QuickBooks Online does not enforce any of this. It posts based on payroll items, default expense mappings, and cash activity. Unless mappings are designed intentionally, financials will be wrong even if payroll is processed correctly.

This article explains, step by step, how to map employee and employer portions of self-funded insurance in QuickBooks Online so the balance sheet, income statement, and payroll reports remain US GAAP compliant and audit-defensible.

What Makes Self-Funded Insurance Different

Before touching QuickBooks Online, the accounting model must be clear.

Fully Insured Plan (QuickBooks Online Friendly)

Employer pays a fixed premium

Insurance company bears claim risk

Payroll deductions reduce premium

Expense equals premium

Self-Funded Plan (QuickBooks Online Hostile)

Employer bears claim risk

Employer pays claims as they arise

Employee deductions fund part of claims

Employer holds money temporarily

Liabilities accumulate and reverse

QuickBooks Online treats both as “insurance.” US GAAP does not.

The Core Accounting Question

For every payroll run, ask two questions:

Who owns the money?

Is this an expense, a liability, or a settlement?

If you answer those correctly, mapping becomes obvious.

Employee Contributions: Not Revenue, Not Expense

This is the most common error.

What Users Often Do

Map employee deductions to “Insurance Expense”

Let payroll reduce net pay and post expense

Ignore the balance sheet impact

Why That Is Wrong

Employee contributions for self-funded insurance:

Belong to the plan, not the employer

Are withheld amounts

Create a liability until claims or refunds occur

Recognizing them as expense inflates costs and distorts margins.

Employer Portion: Expense With Timing Discipline

Employer contributions are compensation cost.

However:

Expense follows service period

Payment timing does not control recognition

Claims paid are not automatically expense

The employer portion must be separated from cash movements.

The Three Buckets You Must Create in QuickBooks Online

To map correctly, QuickBooks Online needs structure.

Minimum Required Accounts

Employee Insurance Payable (Liability)

Self-Funded Insurance Expense (Expense)

Self-Funded Claims Payable (Liability)

Optional but recommended:

Prepaid Claims

Stop-Loss Insurance Expense

Plan Administrative Fees

Without these, everything collapses into one number.

Payroll Item Mapping: Where Things Usually Break

QuickBooks Online payroll lets you map deductions and contributions, but defaults are misleading.

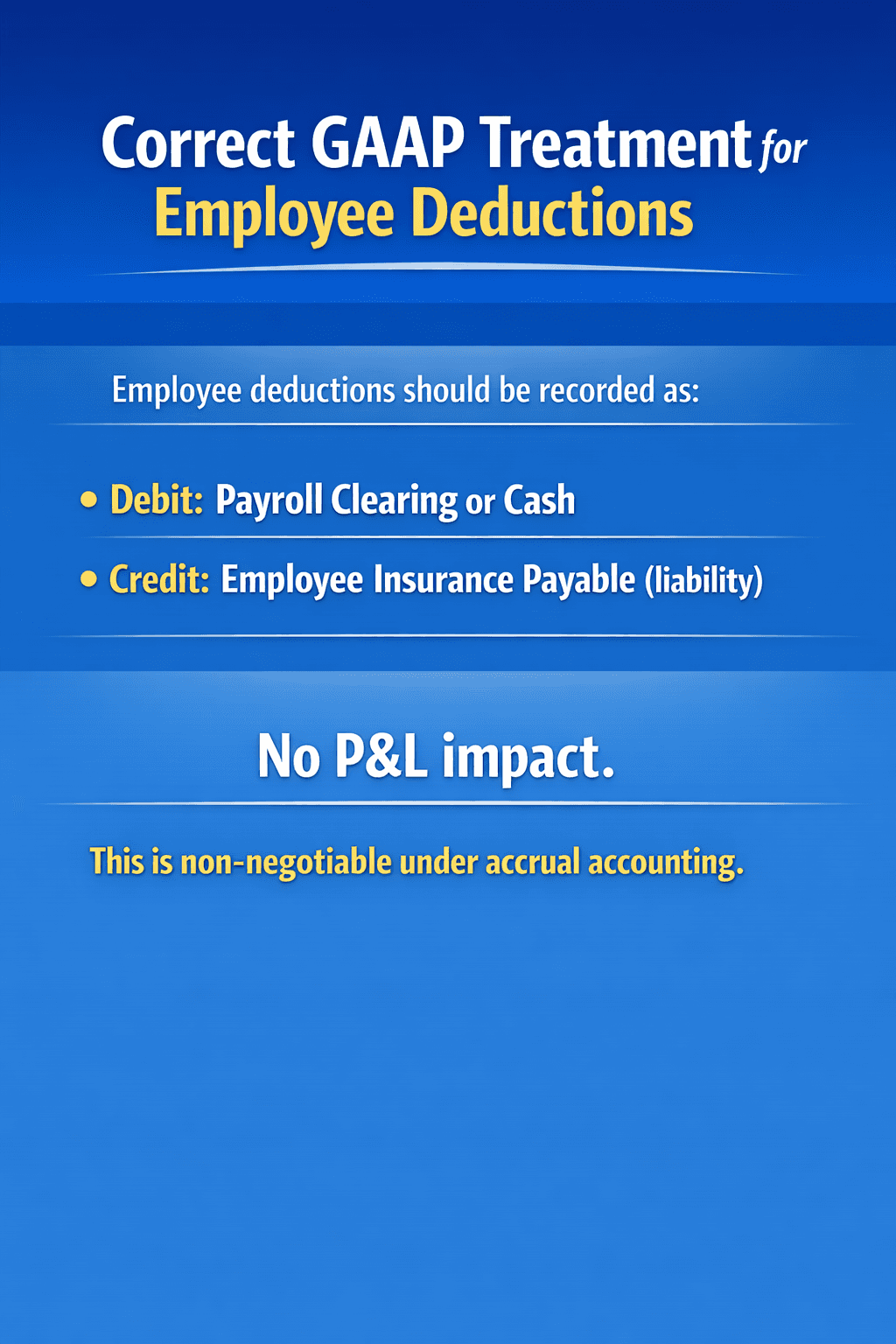

Employee Deduction Mapping

Correct mapping:

Payroll item → Liability account

Incorrect mapping:

Payroll item → Insurance expense

The incorrect option looks “reasonable” and is wrong.

Employer Contribution Mapping

Employer contributions should map to:

Expense account (for accrual recognition)

Or liability account if you accrue separately

What matters is consistency and reconciliation.

Practical QuickBooks Online Setup: Step by Step

Step 1: Create Liability Accounts

Create these under Chart of Accounts:

Employee Insurance Payable

Self-Funded Claims Payable

Account type: Other Current Liability

Step 2: Configure Payroll Deductions

For employee deductions:

Go to Payroll Settings

Edit insurance deduction

Set posting account to Employee Insurance Payable

Do not map to expense.

Step 3: Configure Employer Contributions

Two acceptable methods:

Method A: Expense on Payroll Date

Employer contribution → Insurance Expense

Use if accrual timing closely matches payroll.

Method B: Accrual First, Expense via Journal Entry

Employer contribution → Liability

Monthly accrual → Expense

Preferred for GAAP consistency.

Claims Payments: Settlement, Not Expense

This is where self-funded plans confuse everyone.

Common Mistake

Pay medical claim

Code to Insurance Expense

Correct Treatment

If claims were accrued:

Debit Claims Payable

Credit Cash

No new expense.

If not accrued:

Expense only the portion earned in period

Accrue remaining exposure

Case Scenario 1: Employee Deductions Misclassified as Expense

Company Profile

Manufacturing company, 180 employees.

Issue

Employee deductions posted to insurance expense.

Impact

Expenses overstated

EBITDA understated

Liabilities understated

Fix

Reclassify historical deductions

Correct payroll mapping

Implement liability reconciliation

Result

Margins normalized. Audit adjustment avoided.

Case Scenario 2: Employer Contributions Paid Through Claims

Company Profile

Tech company with TPA-administered self-funded plan.

Issue

Employer portion implicitly paid through claim reimbursements.

Problem

Expense recognition tied to cash claims, not service period.

Fix

Accrue employer portion monthly

Use claims payable to clear cash

Outcome

Predictable monthly expense. Reduced volatility.

Why Self-Funded Plans Require Liability Thinking

Self-funded insurance behaves like a short-term obligation pool.

Claims incurred but not reported

Employee money held temporarily

Employer exposure fluctuates

Treating this as “just insurance expense” hides risk.

GAAP Anchors You Must Respect

Relevant guidance includes:

ASC 710 – Compensation

ASC 450 – Loss contingencies

ASC 405 – Liabilities

Together they require recognition of obligations when probable and estimable.

Claims exposure qualifies.

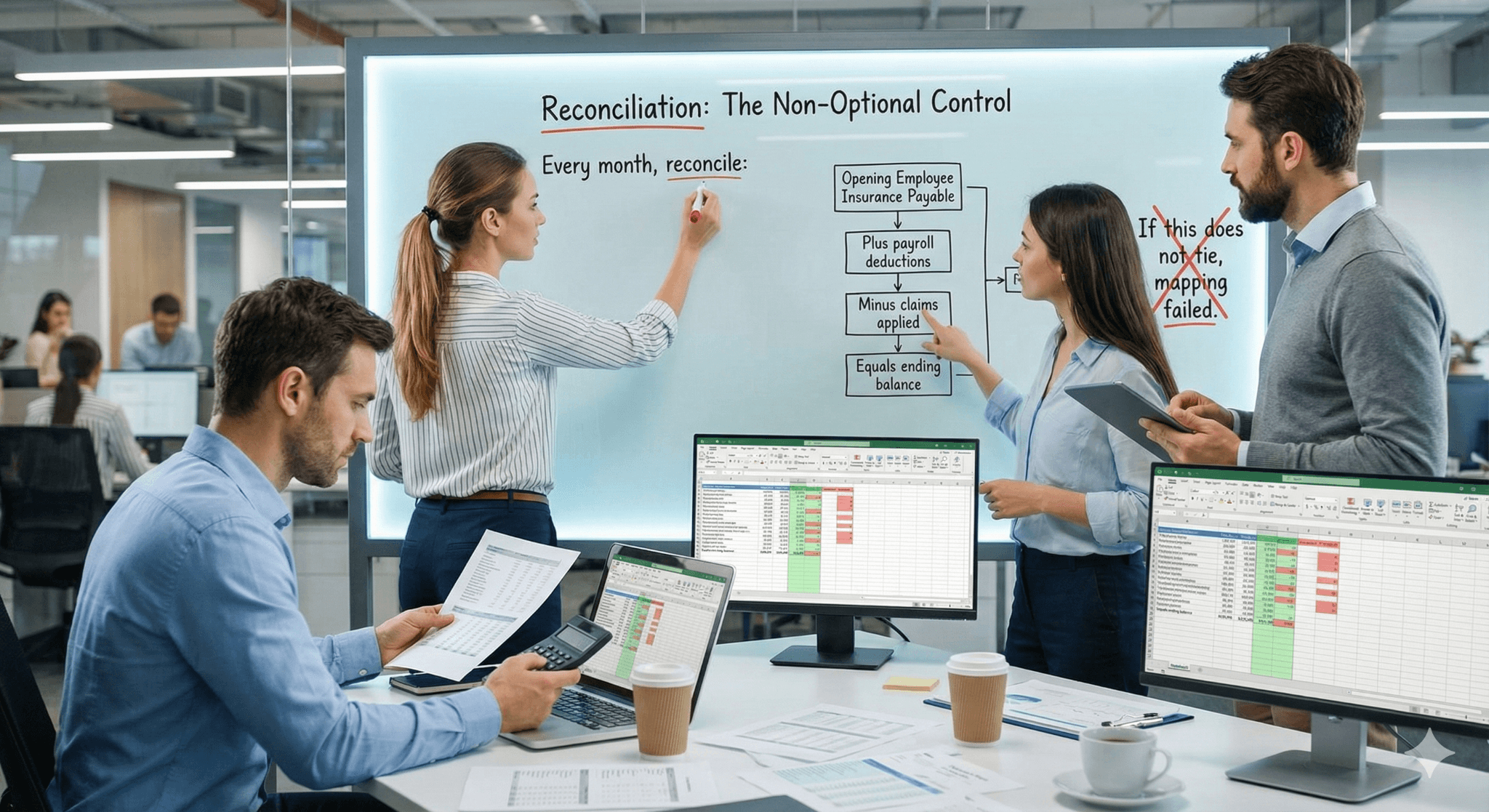

Reconciliation: The Non-Optional Control

Every month, reconcile:

Opening Employee Insurance Payable

Plus payroll deductions

Minus claims applied

Equals ending balance

If this does not tie, mapping fails.

Mini-Case: Audit Red Flag from Poor Mapping

Finding

Employee insurance payable had a credit balance that never cleared.

Cause

Claims coded to expense, not liability.

Resolution

Rebuild mapping. Restate prior periods.

Lesson

Mapping errors accumulate silently.

Tool and Workflow Comparison

Approach | Accuracy | Effort | Audit Risk |

Default QuickBooks Online mapping | Low | Low | High |

Manual reclasses | Medium | High | Medium |

Proper payroll mapping with FinBoard.ai | High | Medium | Low |

Common Pushback and Reality

“QuickBooks Online does not support self-funded plans.”

It does, if you use liabilities correctly.

“This is too complex for SMBs.”

Incorrect mapping is more costly.

“Auditors never asked before.”

They will when amounts grow.

FAQ

Are employee deductions income?

No.

Are claims always expenses?

No, not if accrued.

Can this be automated?

Partially. Judgment remains.

Is this GAAP required?

Yes, under accrual accounting.

Glossary

Self-Funded Plan

Employer bears claim risk.

Employee Insurance Payable

Liability for withheld employee contributions.

Claims Payable

Liability for incurred medical claims.

IBNR

Incurred but not reported claims.