How to Capitalize an Operating Lease in QuickBooks Online under ASC 842

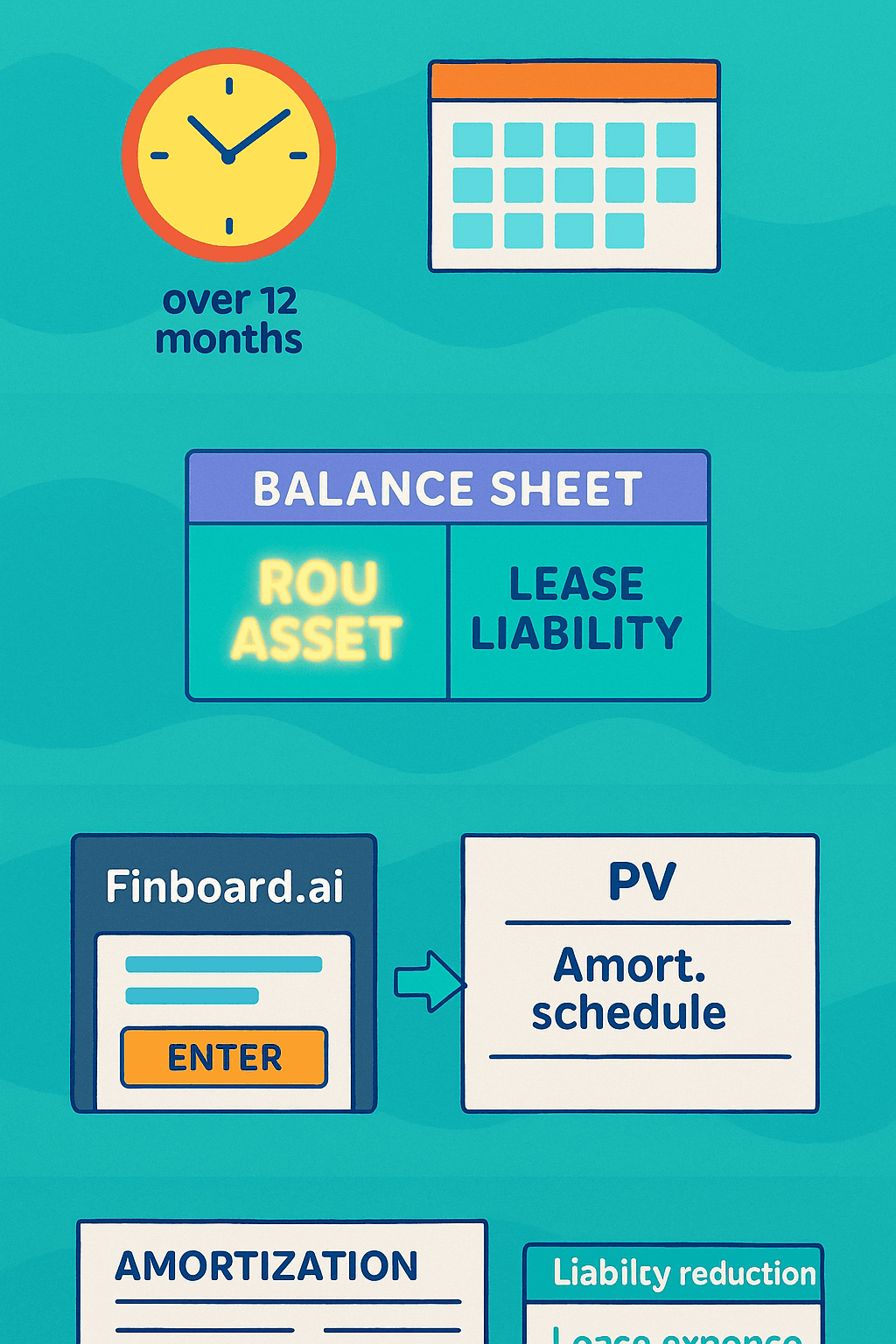

ASC 842 requires every operating lease longer than 12 months to be capitalized on the balance sheet by recording a Right-of-Use (ROU) asset and a matching Lease Liability at the present value (PV) of future lease payments. This is where many small and mid-sized companies using QuickBooks Online run into hurdles. QuickBooks Online does not have a native lease accounting module – it cannot calculate the PV of lease payments, cannot automatically generate amortization schedules, and cannot split monthly payments into liability reduction vs. ROU amortization. Manual journal entries and recurring transactions, which quickly becomes error-prone if you manage multiple leases.

A practical solution is to use a specialized tool like Finboard.ai. With Finboard.ai, you can input the lease contract terms (payment schedule, discount rate, commencement date, options, residuals), and the system automatically computes the PV of future lease payments. It generates an opening journal entry with the ROU asset and lease liability balances, and then produces a full amortization schedule that splits cash payments into liability reduction and straight-line lease expense. These entries can be posted directly into QuickBooks Online, eliminating manual Excel work.

Executive summary

ASC 842 requires lessees to bring nearly all leases onto the balance sheet, including operating leases. Small and mid-market companies using QuickBooks Online often face challenges because QuickBooks Online does not have a dedicated lease accounting module. It cannot compute present value, automatically create right-of-use (ROU) assets and lease liabilities, or handle amortization and interest allocation.

The practical approach is to capture contract details, calculate present value of lease payments externally, create ROU asset and lease liability accounts in QuickBooks Online, post the opening journal entry, and then record monthly lease expense while reducing the liability. Tools such as Finboard.ai can help automate this workflow.

This guide outlines key data fields, QuickBooks Online steps, sample journal entries, reconciliation methods, and control points to ensure ASC 842 compliance is auditable and repeatable.

When to capitalise: ASC-842 scope and classification

Under ASC 842, all leases longer than 12 months (except short-term elections) are recognised on the balance sheet. Unlike ASC 840, the focus is no longer on “capital vs. operating” classification tests — instead, both types require recognition of an ROU asset and lease liability.

Step-by-step: Compute PV, create accounts, and post opening JE

Minimum data required: lease payments, lease term, discount rate (incremental borrowing rate or implicit rate if known), commencement date, initial direct costs, incentives, residual values.

Compute Present Value (PV):

Build an amortization schedule in Excel or use a lease accounting tool like Finboard.ai.

Apply a discount rate to all fixed payments.

Record PV as both ROU asset and lease liability.

Template operating leases under ADC 842 can be accessed in https://finboard.ai/templates/operating-lease-template-asc-842-for-quickbooks-online

Chart of Accounts setup in QuickBooks Online:

Right-of-Use Asset — Operating Lease (Non-current Asset)

Accumulated Amortization — Contra Asset

Lease Liability — split between Current and Non-Current

Example Opening Journal Entry (PV = $150,000; IDC = $3,000):

Date: Lease commencement

Dr. Right-of-Use Asset $153,000

Cr. Lease Liability (Non-current) $150,000

Cr. Cash/Bank (IDC paid) $3,000

Attach the amortization/PV worksheet and lease contract to the JE or reference it in the memo.

Periodic entries under ASC 842 (Operating Lease)

1. Initial Recognition (Lease Commencement)

At the start of the lease, you recognize:

Lease Liability: Present value of future lease payments

ROU Asset: Lease liability + Initial Direct Costs (IDC) − any lease incentives

Example:

Lease term: 4 years (48 months)

Monthly payment: $5,000

PV of lease payments: $215,000

IDC: $5,000

Journal Entry (Opening):

Dr. Right-of-Use Asset $220,000

Cr. Lease Liability (Non-current) $215,000

Cr. Bank/Cash (IDC paid) $5,000

Explanation:

ROU Asset = PV of lease liability + IDC

Lease liability recorded at PV

IDC paid in cash reduces cash

2. Monthly Lease Expense Recognition

For operating leases, P&L recognizes a single lease expense (straight-line) each month.

Total lease expense per month = $5,000

Cash payment to lessor = $5,000

Journal Entry (Monthly Recognition):

Dr. Lease Expense (P&L) $5,000

Cr. Lease Liability (current) $5,000

Dr. Lease Liability (current) $5,000

Cr. Cash / Bank $5,000

Explanation:

Total lease expense is straight-line, regardless of interest calculation

Lease liability decreases as cash is paid

No separate interest and amortization split in P&L for operating leases

4. Summary of Key Points for Operating Leases (ASC 842)

Action | Debit | Credit | Notes |

Initial recognition | ROU Asset | Lease Liability + Cash | PV of lease + IDC |

Monthly P&L expense | Lease Expense | Lease Liability | Straight-line; single line in P&L |

Cash payment | Lease Liability | Bank/Cash | Full invoice paid; liability reduces accordingly |

Audit trail and disclosure

Maintain:

Signed lease agreement

PV calculation and discount rate policy

Opening JE with attachments

Monthly amortization schedule and reconciliations

Disclosure schedule (ASC 842 footnote requirements):

Weighted-average discount rate

Weighted-average remaining lease term

Maturity analysis of lease liabilities by year

Total lease expense for the period (straight-line basis)

Build disclosure schedules from amortization spreadsheets or third-party tools like Finboard.ai , as QuickBooks Online cannot produce them natively.

Tools, apps, and automation

Options:

QuickBooks Online : Supports fixed assets but requires manual lease JE entries.

Finboard.ai : Automates PV calculations for ROU asset and amortization under ASC 842.

Manual spreadsheet + recurring JEs: Cost-effective for few leases; higher risk for multiple leases.

Comparison:

Tool/Workflow | Automates PV? | Straight-line lease expense? | Posts JEs to QuickBooks Online? |

QuickBooks Online | No | Limited | Yes |

Finboard.ai with googlesheet | Yes | Yes | Manual only |

Spreadsheet + recurring JE | No | Manual | Manual only |

Recommendation:

For one or two leases, manual spreadsheets + JEs may suffice. For multiple leases or where disclosures must be audit-ready, third-party tools are strongly recommended.

Risks and mitigations

Incorrect PV calculation → Use proper discount rates and formulas; independent review.

Lease expense misstatement → Ensure straight-line recognition across term.

Weak documentation → Attach contracts, schedules, and memos consistently.

Disclosure errors → Build templates from exports; review annually.

App integration issues → Test and reconcile after implementation.

Mini-Case (QuickBooks Online-centric)

A logistics company signs a 4-year warehouse lease, $5,000 monthly starting Jan 1, 2025. PV at 5% discount rate = $215,000. Initial direct costs = $5,000.

Opening JE: ROU asset $220,000, liability $215,000, IDC $5,000 paid.

Monthly lease expense: $5,000 straight-line.

Liability amortization tracked in Excel; reconciled to QuickBooks Online monthly.

Auditors requested PV workbook and discount rate memo. All reconciliations passed.

FAQ

Q1: Does ASC 842 require operating leases to be on the balance sheet?

Yes. All leases over 12 months require ROU asset and liability recognition.

Q2: How is lease expense recognised under ASC 842 operating leases?

As a single straight-line lease expense across the lease term.

Q3: Can QuickBooks Online calculate PV or handle lease schedules?

No. PV and amortization must be prepared externally or through a third-party tool like Finboard.ai.

Q4: How do I keep the process auditable?

Maintain a lease register, attach contracts and PV schedules to JEs, and reconcile monthly.

Q5: What about short-term leases?

If 12 months or less and exemption is elected, treat payments as expense and disclose election.

Glossary

ROU asset: Capitalised right to use a leased asset.

Lease liability: PV of lease payments recognised on balance sheet.

Straight-line lease expense: Even recognition of lease expense over the lease term.

Discount rate: Incremental borrowing rate or implicit rate, used for PV calculation.

ASC 842: US GAAP standard requiring nearly all leases to be capitalised on the balance sheet.