Purchase price allocation is not a valuation exercise alone; it is an accounting conclusion.

Fair value drives everything, but tax, revenue, and systems decide whether it holds.

Most PPA issues surface months later during audits or revenue reviews.

QuickBooks Online does not support PPA natively; structure and discipline matter.

The biggest mistakes are not technical; they are sequencing and documentation failures.

Executive Summary

Purchase price allocation is one of those accounting topics everyone claims to understand until they actually have to execute it. On paper, the process looks straightforward: allocate the purchase price to identifiable assets and liabilities at fair value, recognize goodwill or a bargain purchase gain, and move on.

In practice, PPA sits at the intersection of valuation, revenue recognition, tax accounting, and financial systems. A mistake in any one area can ripple across amortization, deferred taxes, revenue timing, and future impairments.

For SaaS companies using QuickBooks Online, the challenge is amplified. QuickBooks Online does not understand fair value, tax basis, or acquisition accounting. Every conclusion must be built outside the system and then carefully translated into journal entries that will survive audits and management scrutiny.

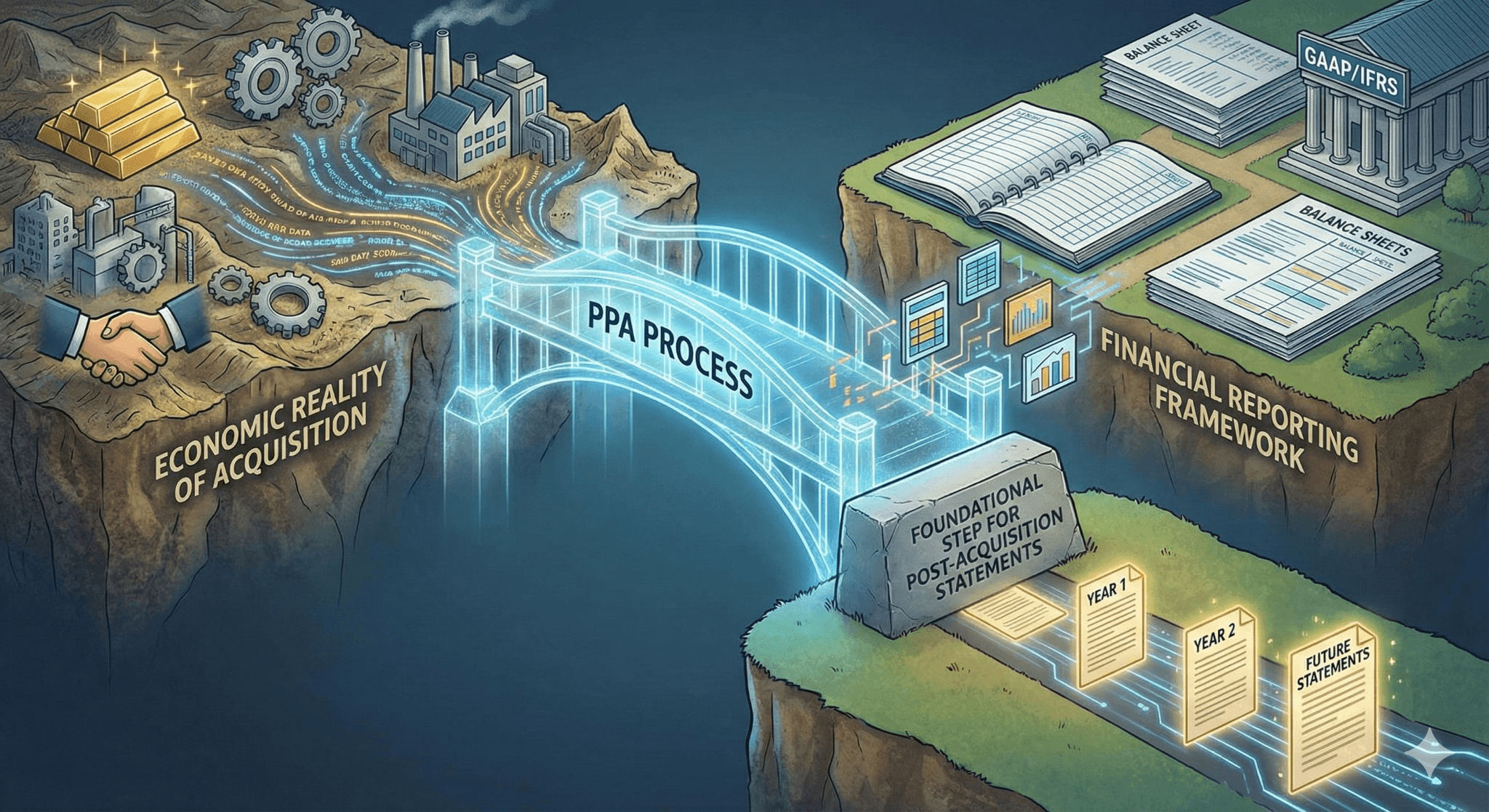

This guide walks through purchase price allocation from a practical, execution-first perspective. It explains what PPA really is, how it works under US GAAP, how SaaS economics change the analysis, where QuickBooks Online complicates matters, and how experienced finance teams avoid painful rework months after close.

1. What Purchase Price Allocation Really Is (And What It Is Not)

Let us start by stripping away jargon.

Purchase price allocation is not about “assigning numbers to assets.”

It is about answering one question:

What did the acquirer actually buy, and what is it worth today?

Under ASC 805, the acquirer must:

Identify all assets acquired and liabilities assumed.

Measure them at fair value on the acquisition date.

Allocate the purchase consideration accordingly.

Anything left over becomes goodwill or a bargain purchase gain.

What PPA Is Not

It is not a tax exercise, even though tax effects matter.

It is not a revenue exercise, even though deferred revenue is involved.

It is not a valuation report, even though valuations support it.

The process of Purchase Price Allocation (PPA) is frequently misunderstood. It is essential to clarify what a PPA is not before defining what it fundamentally is.What Purchase Price Allocation (PPA) is NOT:

It is not solely a tax exercise, even though tax effects matter significantly.

While the tax deductibility of certain acquired assets (like goodwill or intangible assets) is a crucial consideration and must be factored into the final accounting conclusion, the PPA's primary purpose is financial reporting under accounting standards (e.g., GAAP or IFRS), not tax compliance. Tax attributes, such as deferred tax liabilities or assets arising from the PPA, are an effect of the allocation, not the goal of the allocation.

It is not a revenue exercise, even though deferred revenue is involved.

The PPA requires identifying and fair valuing all liabilities, including contract liabilities like deferred revenue, assumed by the acquirer. This step directly impacts post-acquisition revenue recognition. However, the PPA itself is a balance sheet exercise focused on asset and liability measurement at the acquisition date, not an income statement or revenue forecasting activity. It is the adjustment and subsequent accounting treatment of the acquired deferred revenue that relates to future revenue, not the PPA process itself.

It is not a valuation report, even though valuations support it.

The PPA process relies heavily on valuations performed by independent specialists to determine the fair value of various identified tangible and intangible assets, as well as assumed liabilities. However, a PPA is broader than a collection of individual valuation reports. It requires integrating these valuations, reconciling them to the total purchase price, and applying complex accounting principles and judgments, particularly concerning the allocation of any residual amount to goodwill.

What Purchase Price Allocation (PPA) IS:

PPA is an accounting conclusion informed by all of the above.

The Purchase Price Allocation (PPA) is the mandatory accounting process, typically under ASC 805 or IFRS 3, that an acquirer performs after a business combination. Its core purpose is to allocate the total cost of the acquisition (the purchase price) to the assets acquired and liabilities assumed of the target company based on their respective fair values as of the acquisition date.

The PPA is the final, comprehensive record of:

Identification: Separating and identifying all tangible and recognized intangible assets and liabilities.

Measurement: Determining the fair value of each identified asset and liability.

Reconciliation: Calculating the residual value, which is the difference between the total purchase price paid and the net fair value of the identified assets and liabilities. This residual amount is recognized as Goodwill.

In summary, the PPA translates the economic reality of an acquisition into the required framework of financial reporting, serving as the foundational step for all subsequent post-acquisition financial statements.

2. Why PPA Is Especially Complex for SaaS Businesses

Traditional businesses acquire:

Inventory

Property

Equipment

SaaS businesses acquire:

Code

Customers

Contracts

Data

Deferred revenue obligations

These assets are:

Intangible

Hard to value

Closely tied to revenue recognition

This is why SaaS PPAs attract more audit attention than asset-heavy deals.

3. The Core Steps of Purchase Price Allocation Under US GAAP

The steps sound simple. The execution rarely is.

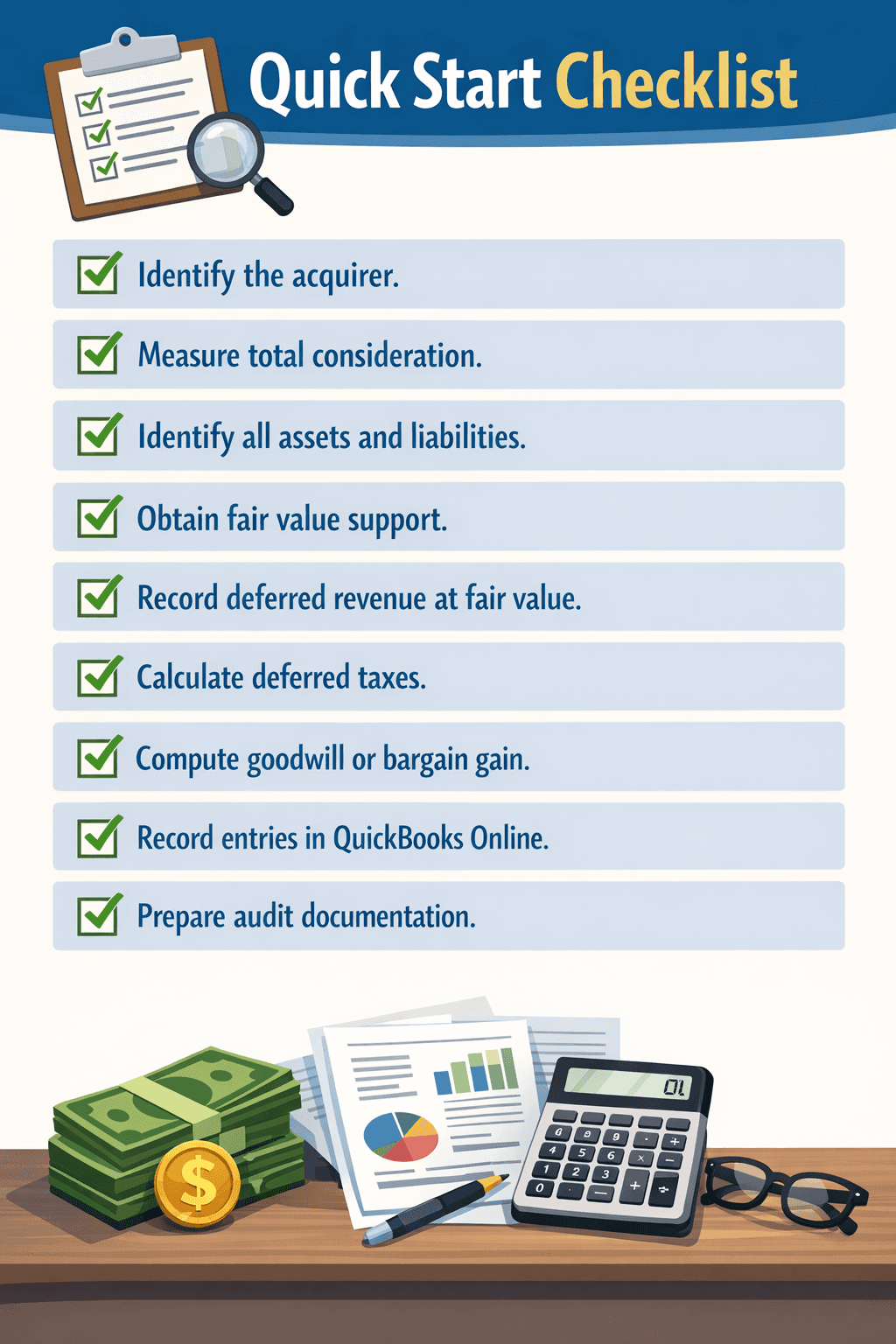

Step 1: Identify the Acquirer

This sounds trivial, but in mergers, roll-ups, or reverse acquisitions, it can be controversial.

The acquirer is the entity that:

Gains control

Directs operations

Bears economic risk

Mistakes here invalidate the entire PPA.

Step 2: Measure Consideration Transferred

Consideration includes more than cash.

It may include:

Cash paid

Equity issued

Earnouts

Assumed liabilities

Earnouts must be measured at fair value on day one, not when paid.

QuickBooks Online often records earnouts when paid, which is wrong for GAAP.

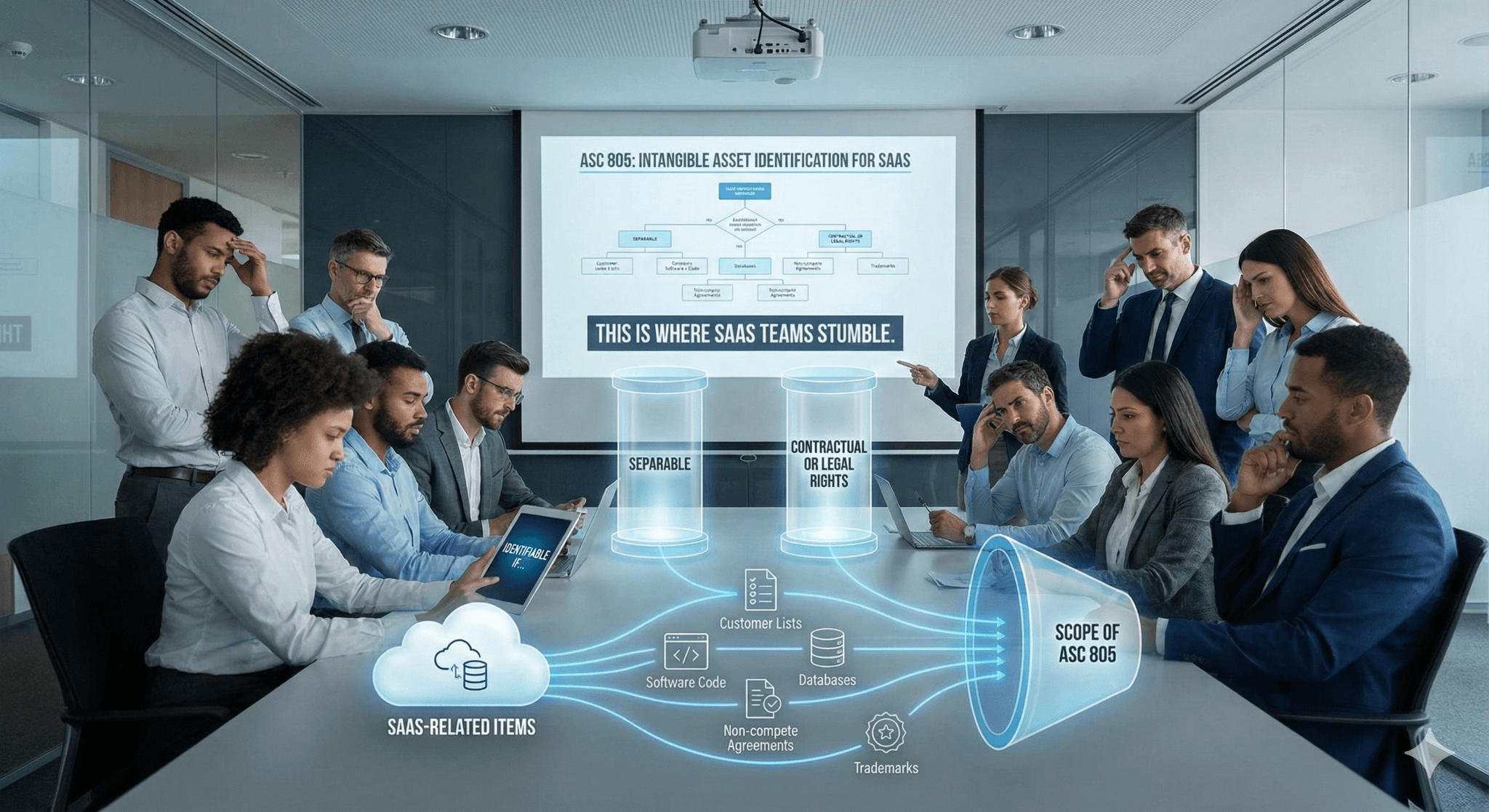

Step 3: Identify All Identifiable Assets and Liabilities

This is where SaaS teams stumble.

Under ASC 805, an intangible asset is identifiable if it:

Is separable, or

Arises from contractual or legal rights

This pulls many SaaS-related items into scope.

4. Common Identifiable Assets in SaaS PPAs

4.1 Developed Technology

This is almost always recognized.

It represents:

The existing codebase

Underlying architecture

Functional software

It does not include future features.

Valuation usually uses:

Relief-from-royalty method

Cost-to-recreate as a sanity check

4.2 Customer Relationships

These represent:

Existing customers

Expected renewals

Historical churn patterns

They are not goodwill simply because customers “could leave.”

Customer relationships are amortized, often over 3–7 years.

4.3 Trade Names and Trademarks

Often overlooked.

If the acquirer intends to continue using the brand, it likely has value.

If the brand will be sunset immediately, value may be minimal.

4.4 Deferred Revenue (Yes, It Is a Liability)

Deferred revenue is not carried over at book value.

It is measured at fair value, which reflects:

Cost to fulfill remaining obligations

Reasonable profit margin

This usually results in a haircut compared to the seller’s books.

5. Deferred Revenue: The Most Misunderstood Part of PPA

This deserves special attention.

Book Reality

The seller may show $1,000,000 of deferred revenue.

PPA Reality

The acquirer records only the fair value of remaining performance obligations, which might be $600,000.

The missing $400,000 is not “lost revenue.”

It never existed for the acquirer.

This affects post-acquisition revenue trends and surprises many executives.

6. Case Scenario 1: SaaS Acquisition With Deferred Revenue Shock

Facts

Purchase price: $8 million

Seller deferred revenue: $2 million

Cost to fulfill: $1.2 million

Required margin: $200,000

Fair value of deferred revenue: $1.4 million

Impact

$600,000 reduction in liabilities

Increase in net identifiable assets

Increase in goodwill or reduction in bargain gain

Revenue post-close looks lower than seller’s forecast, but accounting is correct.

7. Assembling the Fair Value Balance Sheet

Once assets and liabilities are identified, they must be assembled into a fair value balance sheet.

This is the heart of PPA.

Example structure:

Item | Fair Value |

Cash | $500,000 |

AR | $900,000 |

Developed technology | $3,000,000 |

Customer relationships | $2,500,000 |

Trade name | $400,000 |

Deferred revenue | $(1,400,000) |

AP | $(600,000) |

Net identifiable assets are compared to consideration transferred.

8. Goodwill vs Bargain Purchase

If consideration exceeds net assets, goodwill arises.

If net assets exceed consideration, a bargain purchase gain arises.

Bargain purchases are rare and heavily scrutinized.

Auditors assume:

Measurement error

Missing liabilities

Overstated asset values

9. Case Scenario 2: Goodwill Driven by Customer Concentration Risk

Two SaaS companies acquire similar targets at the same price.

One has diversified customers.

The other has one customer representing 60% of revenue.

Customer relationships are valued lower in the second deal.

Goodwill increases, even though economics look similar.

This is not manipulation; it reflects risk.

10. Deferred Taxes and PPA (Why They Cannot Be Ignored)

Fair value adjustments create temporary differences.

These require deferred tax assets or liabilities under ASC 740.

Deferred taxes are recorded as part of PPA and affect goodwill or bargain gains.

Ignoring them is one of the fastest ways to fail an audit.

11. Recording PPA in QuickBooks Online

QuickBooks Online does not understand PPA.

You must translate conclusions into journal entries.

Typical Entries

Record intangible assets

Record fair value deferred revenue

Record deferred taxes

Record goodwill or bargain gain

Each entry must be supported by workpapers.

12. Case Scenario 3: Post-Close Audit Adjustment Due to Incomplete PPA

A SaaS acquirer records developed technology and goodwill.

They forget:

Deferred revenue fair value adjustment

Deferred tax liabilities

Six months later, auditors require:

Revenue restatement

Goodwill reduction

Deferred tax entries

The issue was not judgment. It was incompleteness.

13. Amortization and Ongoing Accounting

After PPA:

Intangibles are amortized.

Deferred revenue is recognized.

Deferred taxes reverse over time.

Amortization affects EBITDA.

This matters for earnouts and debt covenants.

14. Internal Controls Over PPA

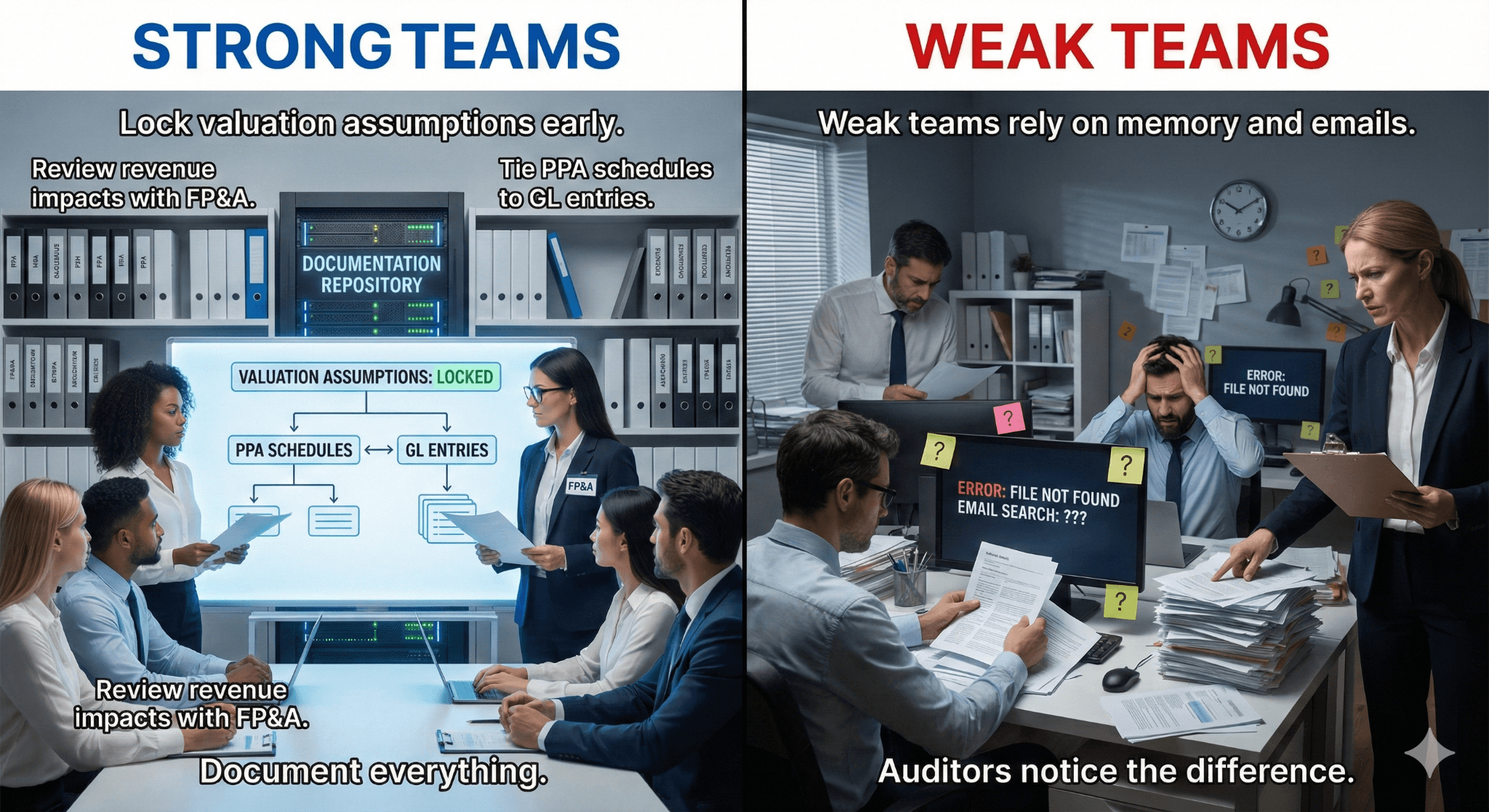

Strong teams:

Lock valuation assumptions early.

Tie PPA schedules to GL entries.

Review revenue impacts with FP&A.

Document everything.

Weak teams rely on memory and emails.

Auditors notice the difference.

Risks and Mitigations

Risk | Mitigation |

Overstated revenue | Deferred revenue fair value |

Audit restatements | Complete PPA documentation |

EBITDA surprises | Amortization forecasting |

System limitations | External schedules |

FAQ

Is a third-party valuation mandatory?

Not legally, but practically yes for material deals.

Can PPA be finalized after close?

Yes, within the measurement period, but changes must be justified.

Does PPA affect taxes immediately?

Often no, but deferred taxes arise immediately.

Can QuickBooks Online handle PPA natively?

No.

Why does revenue drop after acquisition?

Deferred revenue fair value adjustment.

Glossary

ASC 805: Business combinations standard.

PPA: Purchase price allocation.

Deferred Revenue Fair Value: Cost-based measurement of obligations.

Goodwill: Residual value after allocation.

Measurement Period: Up to one year for PPA adjustments.

Final Thought

Purchase price allocation is not an academic exercise. It is where deal economics meet accounting reality.

SaaS companies feel the impact more than most because intangible assets, deferred revenue, and tax effects dominate the balance sheet. Teams that treat PPA as a checklist exercise often spend the next year explaining variances and fixing mistakes.

Teams that approach it deliberately, document assumptions, and respect sequencing avoid surprises and earn credibility with auditors and stakeholders.

That difference matters long after the deal closes.