When a customer contract changes (scope, price, term, obligations), ASC 606 requires an assessment of how that affects recognition.

Some modifications must trigger cumulative catch-up (restating past revenue), others are accounted for prospectively, and some lead to a separate contract treatment.

Upsells and cross-sells create new performance obligations and often require re-allocation of transaction price; treatment depends on whether they are separate or part of an existing contract.

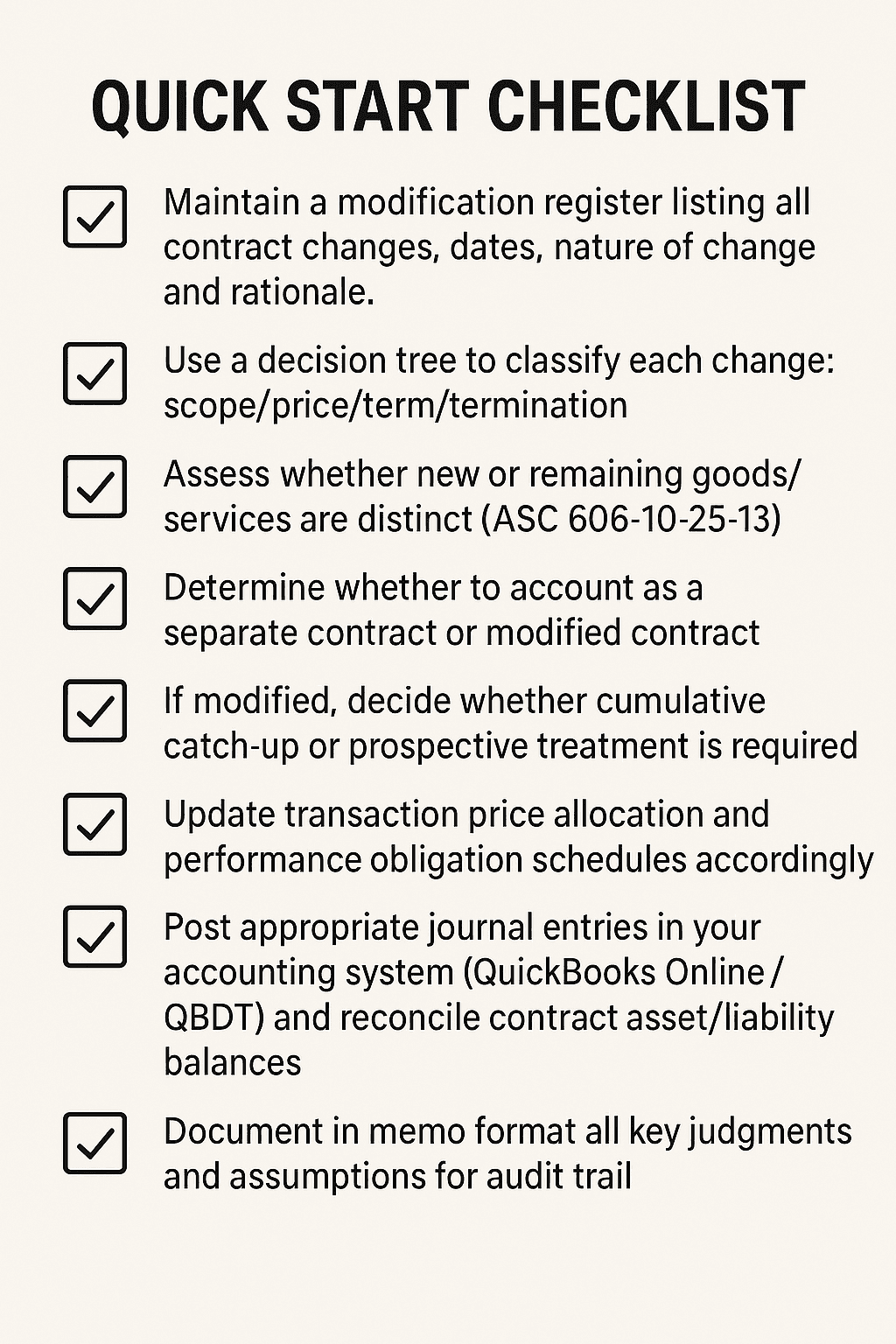

SaaS firms must build robust processes to identify changes, assess distinctness of obligations, adjust allocation, and document for audit.

Three SaaS case-studies illustrate: (1) term/price change requiring catch-up; (2) termination and replacement requiring prospective treatment; (3) upsell requiring separate contract treatment — no past catch-up.

Executive Summary

Accountants, controllers and finance teams supporting SaaS businesses know that the initial subscription contract is rarely the end of the story. Mid-term changes happen: term extensions, price reductions, additional modules, terminations or customer upgrades. Under ASC 606, each of these triggers a detailed assessment: Did the change create new rights and obligations? Are the remaining goods or services distinct? Should the transaction price be re-allocated? Does past revenue require adjustment (catch-up) or only future recognition?

This blog unpacks these nuances, explaining what “revenue re-allocation” means, where upsells and cross-sells fit, and the difference between cumulative catch-up and prospective treatment. We then explore three practical SaaS case-studies: first where a contract’s term and consideration change and require catch-up; second where termination/ replacement means only future allocation adjustment; third where an upsell is accounted as a separate contract, no catch-up required. For each scenario we provide journal entry logic, decision trees and disclosure guidance. Finally, a control checklist and risks section help finance teams stay audit-ready.

H2 1. What Does “Revenue Reallocation” Mean?

“Revenue reallocation” refers to adjusting how the transaction price is allocated to performance obligations when a contract change (modification) occurs. Under ASC 606, when a contract is modified and still forms part of the existing contract, the entity re-assesses the remaining performance obligations and the transaction price. If those remaining obligations are distinct, the entity allocates the revised transaction price to those obligations. This reallocation can change the timing or amount of revenue to be recognised.

H2 2. What Does “Cumulative Catch-Up” Mean?

A “cumulative catch-up” adjustment arises when a contract modification changes both the scope or price and the remaining goods/services are not distinct from those already delivered. In that case, revenue already recognised must be adjusted to reflect the revised transaction price as if the modified contract had been in place from the start of the contract. This means restating prior periods’ revenue (catch-up) rather than only accounting prospectively. It ensures the expense or revenue recognised matches the total deliverables under the modified agreement. For SaaS, when an extension is granted for no additional consideration, or when price is changed for future access only, assessing distinctness is critical to determine whether catch-up is required

.

H2 3. Where Do Upsells and Cross-Sells Fit In?

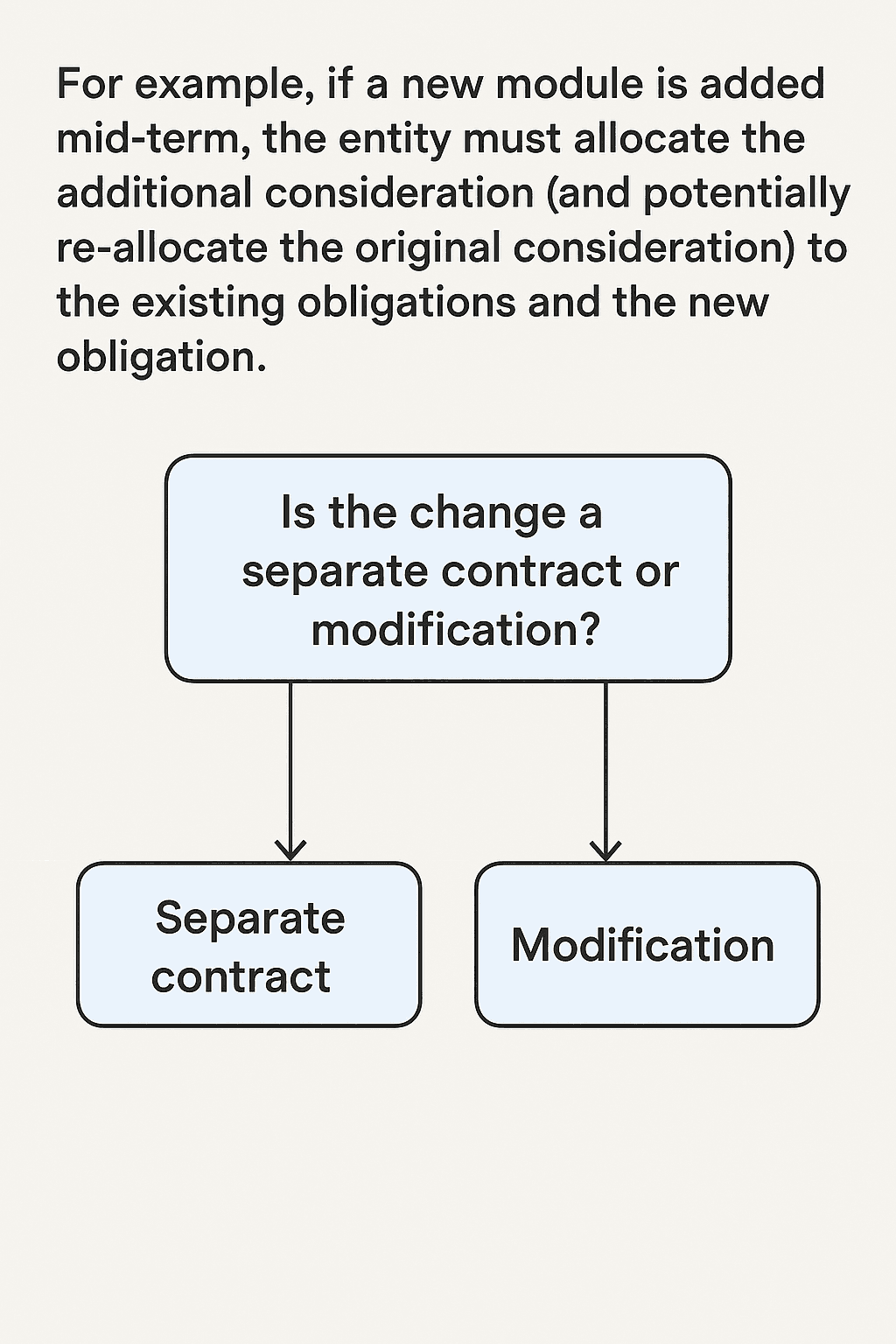

Upsells (adding premium features to the same customer) and cross-sells (adding new but related services) create new deliverables. Under ASC 606, the key question is whether the additional deliverable(s) are distinct from the existing performance obligations and whether the contract change creates a separate contract or modifies the existing one.

If the upsell/cross-sell is distinct and the customer pays additional consideration → often accounted as a separate contract or a new performance obligation of the existing contract.

If the additional service is not distinct (for example, a minor add-on included in original subscription) and no new consideration or minimal one → modification of existing contract, requiring reassessment of remaining performance obligations and price reallocation.

In practice for SaaS: offering a new module for extra fee often leads to separate contracts; discounting upgrade rights without extra fee may trigger modification of the existing contract.

H2 4. Common and Edge Scenarios in SaaS Contract Changes

Common Scenarios

Price increase for the remaining term because of inflation clause in subscription.

Extension of subscription term at no extra charge due to retention strategy.

Customer upgrades mid-term to a higher plan with additional features.

The customer terminates early and requests a pro-rated refund.

Each has recognition implications: timing, allocation, catch-up, liability for refunds.

Edge Scenarios

Portfolio-wide price concession across 5,000 subscriptions mid-renewal period (treatment across many contracts).

Stand-alone selling price (SSP) changes for modules being upsold, requiring reassessment of allocations.

Service interruption leading to deferral of performance obligations and contract modification.

Customer obtains new rights (e.g., customization) as a result of renewal without additional fee — modification logic required.

These edge cases often generate audit scrutiny because of judgement, volume and complexity.

H2 5. Case-Studies in SaaS Contract Modifications

Case Study 1: Continuation of Original Contract (Term & Consideration Changed) – Cumulative Catch-Up Required

Facts: A SaaS company sells a 12-month plan for $1,200 (PO = basic service). At month six, the customer requests a 12-month extension (so the total term becomes 24 months) at no additional fee. The remaining 18 months of original plan and 12 additional months are not distinct in nature of service.

Assessment: The contract is modified. Because the remaining service is the same as already delivered, the entity must apply a cumulative catch-up, restating revenue as if the contract had been for 24 months from inception.

Journal Entry (Simplified):

At modification date: compute revised revenue recognised to date and restate. Adjust contract assets or liability accordingly.

Future months: recognise $1,200 ÷ 24 = $50 per month.

Disclosure: Explanation in the footnote of modification, restatement amounts and impact on prior period comparatives.

Case Study 2: Termination and Replacement Contract – Prospective Treatment Only

Facts: A SaaS firm signs a 36-month contract for $3,600. After 18 months, the customer terminates early and signs a new 24-month contract for $2,400 (new services and pricing).

Assessment: The original contract ends and a new contract begins. There is no remaining service obligation on the original contract. No catch-up because the new contract is separate. Revenue recognition for old contract stops at termination; new contract recognised prospectively.

Journal Entry:

At termination: stop recognising revenue for original contract; recognise refund or liability if applicable.

For a new contract: begin recognition as per schedule.

Disclosure: Provide note on termination, new contract commencement, and no restatement required of old contract’s revenue.

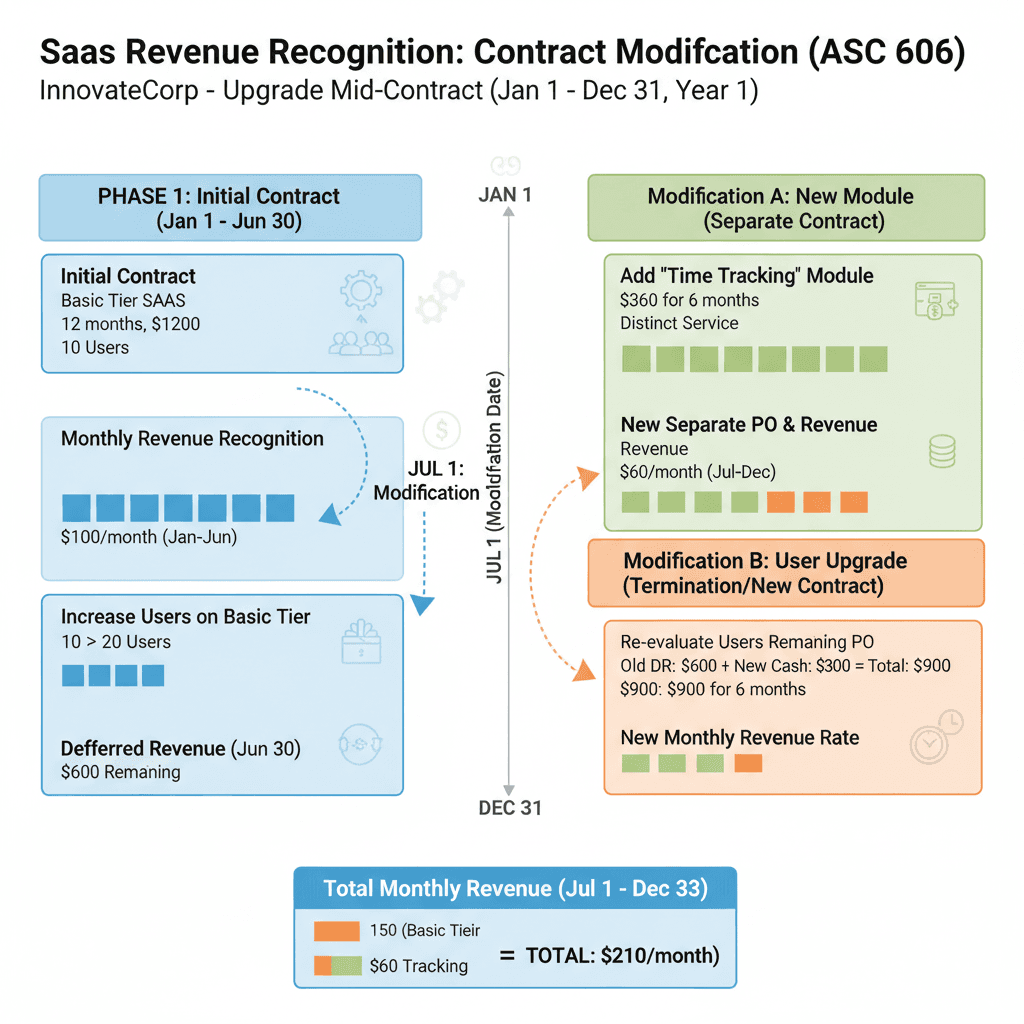

Case Study 3: Upsell as Separate Contract – No Catch-Up / No Reallocation of Original

Facts: A SaaS company sells base subscriptions for $800 (12 months). At month four, the customer adds a premium analytics module for $240. The module is distinct, priced at SSP, and new billing. The base subscription continues unchanged.

Assessment: The upsell is a separate contract (or separate PO within the same contract) with distinct deliverable and price. No transaction price reallocation for original contract, no cumulative catch-up required. Original subscription continues recognition unchanged; module revenue recognised separately over its term.

Journal Entry:

Recognise module revenue separate ($240 ÷ remaining 8 months = $30 per month).

No change to base contract revenue schedule.

Disclosure: Note added module contract, term and recognition method; indicate no effect on original contract’s comparatives.

Tool / Workflow Comparison (if applicable)

Workflow | Strengths | Limitations | Best For |

Spreadsheet + QuickBooks Online export | Low cost, flexible | High manual effort, audit risk | Small SaaS firms with limited modifications |

Automation, integrated | Implementation cost, complexity | Mid market SaaS with many contract variations | |

Dedicated modification tracking tool | Built for change tracking, consistent | Tool cost, training required | Complex SaaS firms, multiple modifications, many entities |

Risks & Mitigations

Risk: Treating all modifications prospectively when catch-up is required ⇒ mis-stated revenue.

Mitigation: Use a decision tree for each contract change and document reasoning.Risk: Ignoring performance obligation reassessment or distinctness ⇒ incorrect allocation or timing.

Mitigation: Review PO definitions upon each modification; involve revenue accounting specialists.Risk: Using spreadsheets without proper audit trail ⇒ audit issues.

Mitigation: Maintain central modification register, memo for each change, and tie-out schedules.Risk: Not capturing portfolio-level changes (e.g., price reductions across many contracts) ⇒ systemic mis-recognition.

Mitigation: Build triggers and automation for high-volume modifications and review in aggregate.

FAQ

Q1: When does a contract modification require a cumulative catch-up adjustment?

A1: When the modification changes the transaction price or adds/reduces goods or services and the remaining goods/services are not distinct from those already delivered. In that case you restate revenue to date as if the modified contract were in place from inception. [10]

Q2: Can we always treat an upsell as a separate contract?

A2: No. Only when the additional good/service is distinct and priced at an SSP and the change meets the separate contract criteria under ASC 606-10-25-8. If not, it may instead modify the existing contract. [3]

Q3: Does early termination always lead to revenue adjustment?

A3: Termination ends the contract; you stop recognising revenue for remaining obligations and may recognise a liability for refunds or credits. Whether prior revenue needs restatement depends on whether a modification occurred before termination. [4]

Q4: If a price reduction applies to many contracts simultaneously (portfolio effect), how should we treat it?

A4: Each contract must be assessed individually, but practically you may apply a standardized treatment if modification terms are identical across the portfolio. The key is ensuring consistent judgement and documentation. [7]

Q5: How should we document these modification treatments in QuickBooks Online?

A5: Maintain a contract register, link each modification to memo referencing ASC 606 guidance, adjust deferred revenue/contract asset accounts via journal entries, and keep mapping to supporting schedules and revisited allocation metrics for audit trail.

Glossary

Contract modification: A change in the terms of a contract that creates new or changes existing enforceable rights/obligations (ASC 606-10-25-10).

Performance obligation (PO): A promise in a contract to deliver a distinct good or service to the customer.

Separate contract: When a contract modification is accounted for as a new contract rather than modification of the original one (ASC 606-10-25-8).

Cumulative catch-up adjustment: A restatement of revenue recognised to date when modification affects transaction price or timing and remaining obligations are not distinct.

Prospective treatment: Accounting for a modification by recognising changes only for future goods/services without adjusting past recognised amounts.