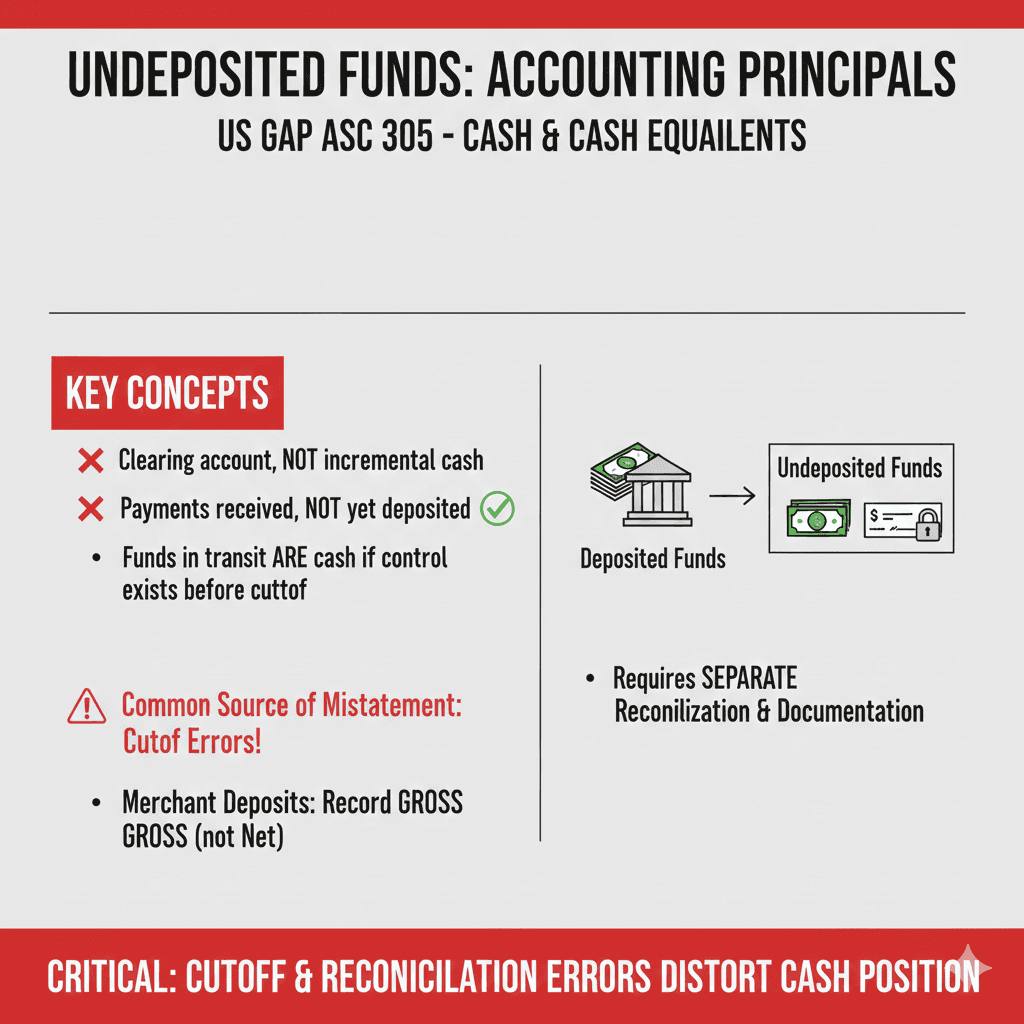

Undeposited Funds is a clearing account, not incremental cash. It represents payments received but not yet deposited into the bank.

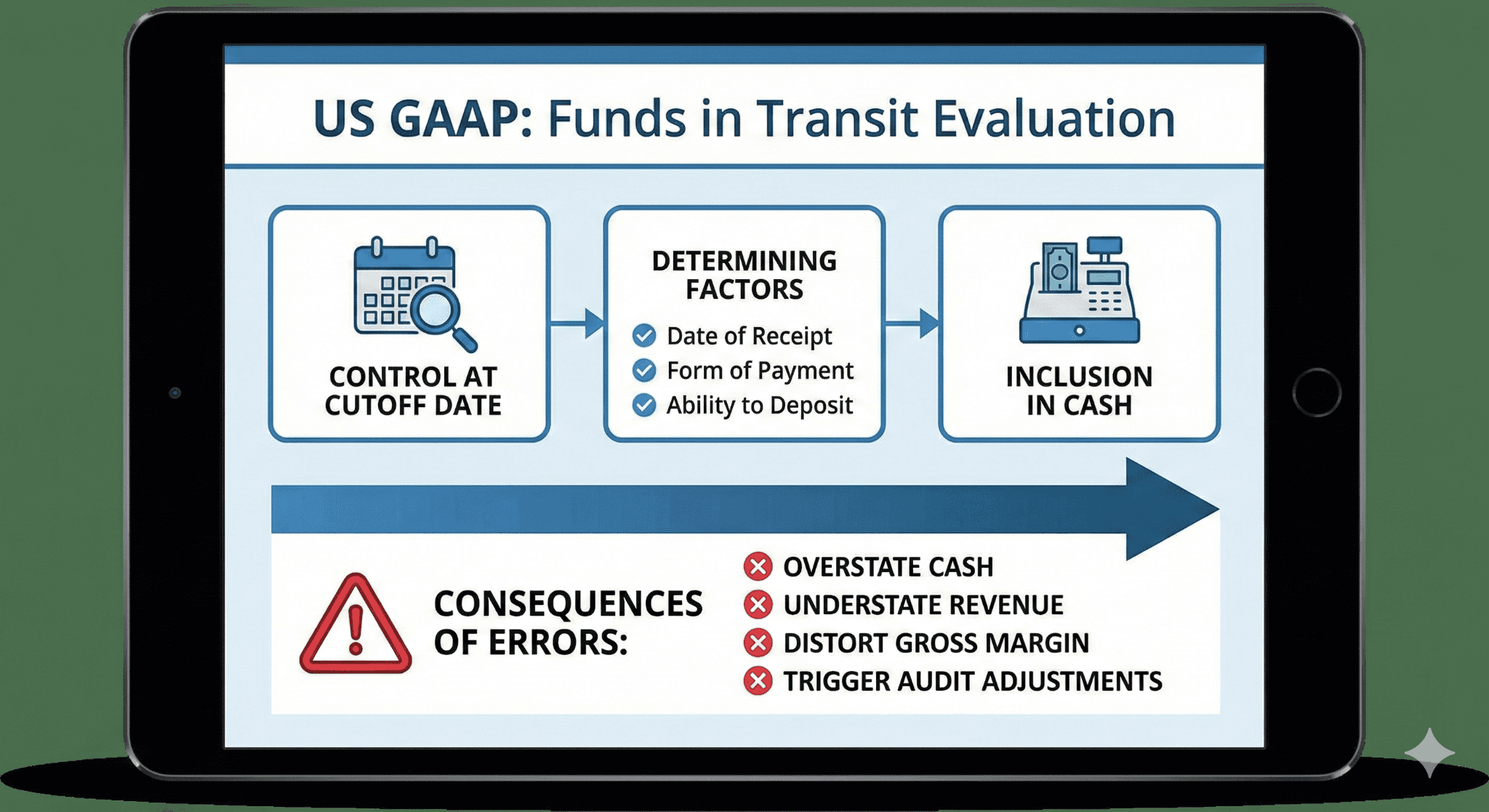

Under US GAAP (ASC 305 – Cash and Cash Equivalents, Canonical), funds in transit are included in cash if the company has control before the reporting cutoff.

Month-end and year-end cutoff errors are the most common source of misstatement.

Merchant processor deposits must be recorded gross, not net of fees.

Undeposited Funds require its own reconciliation and documentation process, separate from the bank reconciliation.

Executive Summary

Undeposited Funds is one of the most operationally convenient yet conceptually misunderstood accounts in QuickBooks Online. It simplifies deposit grouping. However, from a US GAAP perspective, it introduces timing risk, reconciliation complexity, and internal control exposure. Many small and mid-market entities rely on bank feeds and assume the bank reconciliation alone ensures accuracy. That assumption is incorrect.

Under US GAAP, funds in transit must be evaluated based on control at the reporting cutoff. The date of receipt, the form of payment, and the ability to deposit determine inclusion in cash. Errors in this area can overstate cash, understate revenue, distort gross margin, or trigger audit adjustments.

This guide explains the GAAP framework, defines key terminology, and walks through practical case scenarios including physical checks, POS batches, merchant processors, ACH timing differences, intercompany transfers, and stale balances. It provides QuickBooks-Online centric workflows and documentation standards designed for controllers, accountants, and bookkeepers operating in SMB environments.

1. Understanding Undeposited Funds Under US GAAP

What Is Undeposited Funds?

Undeposited Funds in QuickBooks Online is a default current asset account used to temporarily hold customer payments before they are grouped into a bank deposit [1]. It is a clearing account. A clearing account temporarily accumulates transactions until they are finalized elsewhere.

This account exists to solve a workflow issue. Businesses often receive multiple payments and deposit them together. The bank records one deposit. QuickBooks Online must mirror that grouping to reconcile properly.

GAAP Perspective: ASC 305 – Cash and Cash Equivalents (Canonical)

Under ASC 305, cash includes:

Currency on hand

Demand deposits

Cash equivalents with short maturities

Funds in transit may qualify as cash if the entity has control over them at the reporting date.

Control means the company has possession or the ability to direct use of the funds. For example:

A physical check received and secured before cutoff

Cash counted and logged in a register drawer

ACH confirmation showing funds transferred before cutoff

If control does not exist at period-end, recognition must wait until the next period.

2. Month-End Cutoff: The Core Risk Area

Cutoff refers to ensuring transactions are recorded in the correct accounting period [5]. For Undeposited Funds, cutoff issues arise when receipt date and deposit date fall in different periods.

Controllers often focus on the bank statement date. That approach is incomplete. GAAP focuses on the date of receipt and control.

Timeline Illustration

Event | Date | Accounting Impact |

Payment received | January 30 | Record cash (Undeposited Funds) |

Deposit prepared | February 1 | Reclassify to bank |

Bank statement shows deposit | February 2 | Reconciling item |

Income is recognized when earned under accrual accounting. Cash is recognized when received if control exists.

3. Detailed Case Scenarios

Below are practical scenarios frequently encountered in SMB environments.

Case Scenario 1: Physical Check Received on Last Day of Month

Facts

Customer drops off check at 4:30 PM on March 31.

Accounting closes books at 6:00 PM.

Deposit occurs April 2.

Analysis

Control exists on March 31 because the company physically possesses the check. Under GAAP, cash increases March 31.

Journal Entry (March 31)

Dr Undeposited Funds

Cr Accounts Receivable

Documentation Required

Copy of check

Check log showing date received

Deposit slip dated April 2

Audit Risk if Omitted

Cash understated in March. Revenue may also be understated if tied to payment timing.

Case Scenario 2: Check Mailed March 31, Received April 3

Control does not exist on March 31. Recognition occurs April 3. Even if the customer dated the check March 31, the company cannot include it in March cash.

Case Scenario 3: POS Batch Close at Month-End

Retail businesses close POS batches nightly.

Facts

POS batch closed January 31 at 11:45 PM.

Credit card processor deposits February 2.

Under accrual accounting, revenue is recognized January 31 when sale occurs. Cash or receivable from the processor should also be recognized January 31 if settlement is probable and control is established.

Entry January 31

Dr Undeposited Funds or Processor Receivable

Cr Revenue

Documentation

POS batch report

Processor settlement summary

Case Scenario 4: Merchant Processor Deposits Net of Fees

Merchant processors such as Stripe or Square deposit net amounts [8].

Facts

Gross sales: $25,000

Fees: $750

Net deposit: $24,250

Deposit received April 2

If sales occurred March 31, revenue must be recorded gross in March.

March 31 Entry

Dr Undeposited Funds 25,000

Cr Revenue 25,000

April 2 Entry

Dr Bank 24,250

Dr Merchant Fees Expense 750

Cr Undeposited Funds 25,000

Recording only the net deposit understates revenue and distorts margins [9].

Case Scenario 5: ACH Initiated Before Cutoff, Settled After

Facts

Customer initiates ACH on June 30 at 5 PM.

Bank shows pending status.

Settlement clears July 1.

If ACH is irrevocable and the company has confirmation, inclusion in June cash may be appropriate. If not confirmed, defer to July.

Documentation must support the conclusion. Controllers should document policy for ACH timing.

Case Scenario 6: Cash Collected by Field Staff

Field technician collects $3,000 in cash on September 29.

Cash delivered to office October 2.

Control exists when a company employee collects cash if custody is secure and documented.

Required documentation:

Signed receipt to customer

Field collection log

Evidence of secure storage

Weak documentation may result in audit adjustment.

Case Scenario 7: Stale Undeposited Funds Balance

Year-end review shows $18,000 in Undeposited Funds dated 90 days prior.

Common causes:

Duplicate deposits from bank feed auto-match [3]

Deposit recorded without linked payment

Voided invoices not cleared

Clearing via lump-sum journal entry is inappropriate without investigation [2].

Case Scenario 8: Intercompany Funds in Transit

Parent company wires $100,000 December 31.

Subsidiary receives January 2.

Parent records reduction in cash December 31.

Subsidiary records increase when funds are received.

Consolidation requires elimination of in-transit differences.

4. Should You Accrue or Not?

Many practitioners ask whether funds in transit require accrual. The answer depends on the accounting basis.

Accrual Basis

Revenue recognized when earned. Cash timing separate. Undeposited Funds used only for clearing.

Cash Basis

Revenue recognized when payment was received. If the check is physically received before cutoff, revenue is recognized even if not deposited [10].

5. Documentation Requirements for Audit Readiness

Internal controls over cash remain a top audit focus .

Required Evidence at Month-End

Item | Purpose |

Undeposited Funds detail report | Identify open items |

Deposit log | Confirm receipt dates |

Bank reconciliation | Validate cleared deposits |

Processor statements | Support gross revenue |

Cutoff checklist | Formal management assertion |

6. Reconciling Undeposited Funds Separately from Bank

Many bookkeepers reconcile only the bank. That is insufficient.

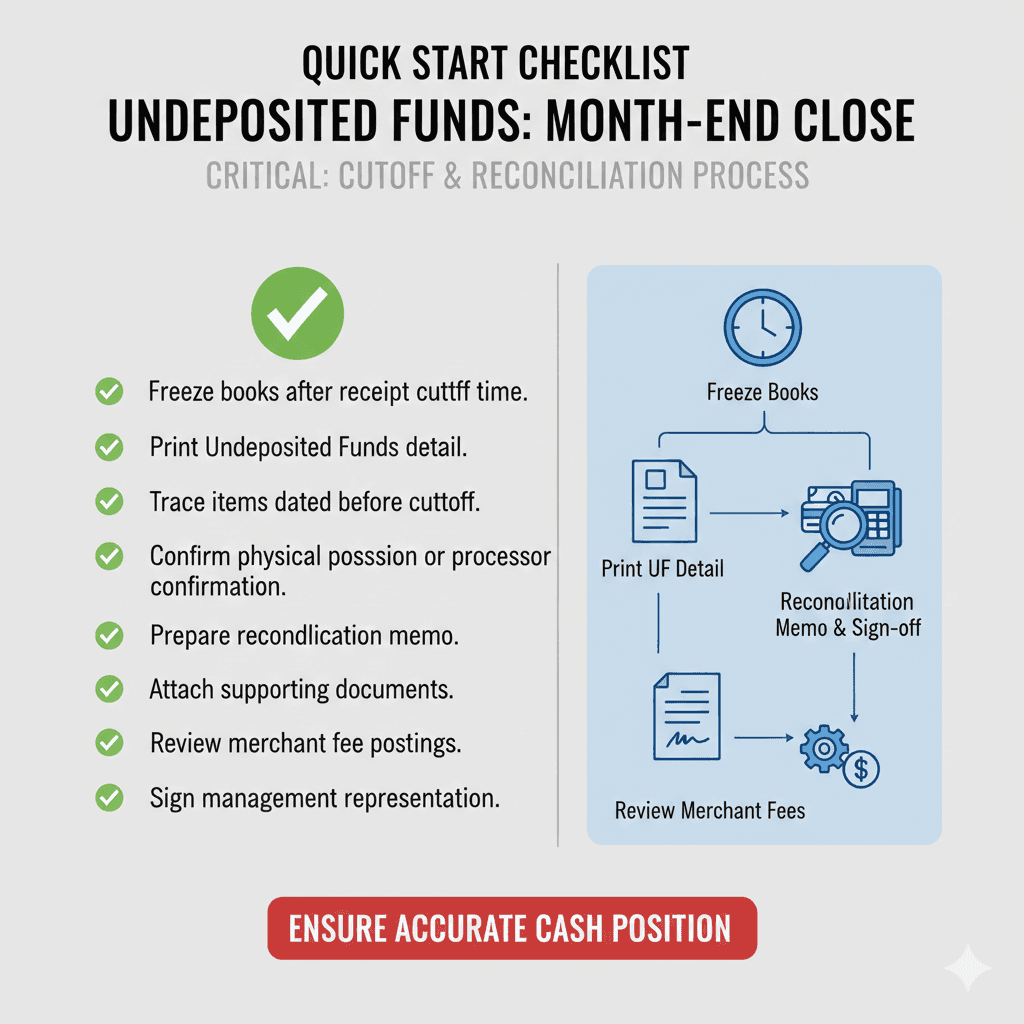

Monthly Undeposited Funds Review Process

Run General Ledger detail for Undeposited Funds.

Sort by transaction date.

Identify items older than 5–7 days.

Trace each to deposit transaction.

Investigate unmatched entries.

Undeposited Funds should normally clear within days in high-volume environments.

7. Internal Control Framework

Key Risks

Theft before deposit

Duplicate posting

Cutoff misstatement

Net revenue misclassification

Control Matrix

Risk | Preventive Control | Detective Control |

Theft | Dual custody on deposits | Surprise cash counts |

Duplicate deposit | Standard workflow | Weekly clearing account review |

Cutoff errors | Written policy | Month-end certification |

Net recording | Gross revenue policy | Margin analytics review |

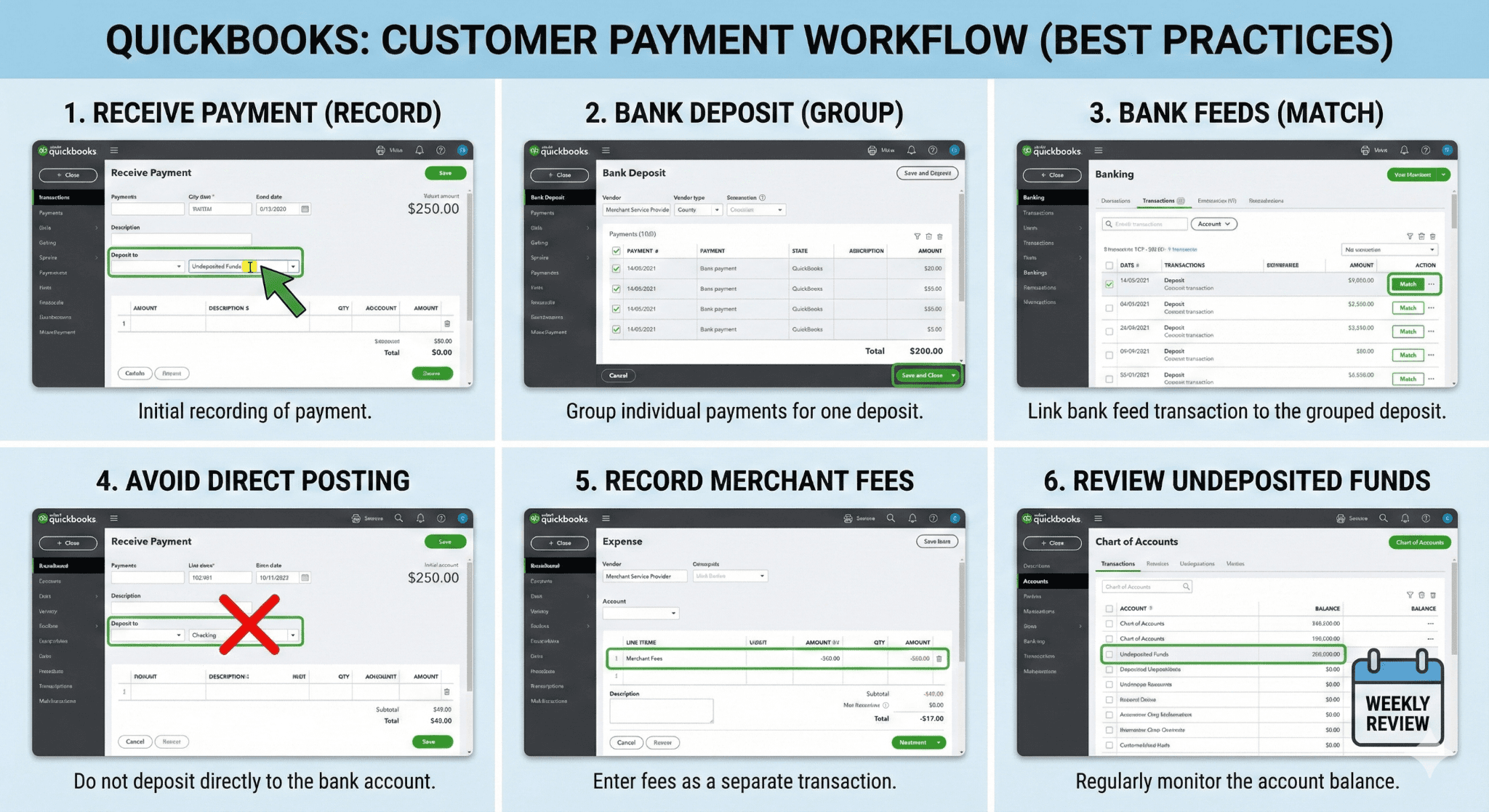

8. QuickBooks Online Workflow: Best Practices

Record customer payments to Undeposited Funds [1].

Use the “Bank Deposit” function to group payments.

Match bank feed to grouped deposit.

Avoid posting payments directly to bank.

Record merchant fees separately.

Review Undeposited Funds weekly.

9. Advanced Year-End Example

A mid-market distributor had:

$72,000 checks received December 30

$15,000 POS batch December 31

$9,000 cash collected by sales rep December 29

Deposits made January 2.

Total in transit: $96,000.

Controller initially excluded these amounts from December cash. Audit adjustment increased cash by 8 percent and corrected working capital ratio.

Documentation supported inclusion.

10. Risks and Consequences

Error | Financial Statement Impact |

Failure to record in transit funds | Understated cash |

Duplicate deposit | Overstated cash |

Net revenue recording | Understated revenue |

Journal entry cleanup | Weak audit trail |

Cash misstatements directly affect liquidity ratios and debt covenant compliance.

11. Quick Start Month-End Checklist

12. Frequently Asked Questions

1. Should Undeposited Funds ever carry a large balance?

Only temporarily. Persistent balances indicate process breakdown.

2. Is Undeposited Funds considered restricted cash?

No. It is unrestricted if control exists.

3. Can I bypass Undeposited Funds for simplicity?

Not recommended if deposits group multiple payments.

4. How often should it be reconciled?

Weekly for high-volume entities. Monthly at minimum.

5. Are merchant fees operating expenses?

Yes. They are typically classified as selling expenses.

Glossary

Clearing Account: Temporary account used until final classification.

Cutoff: Assignment of transactions to correct reporting period.

Funds in Transit: Cash received but not yet reflected in bank statement.

Gross Revenue: Total sales before deductions.

Control: Ability to direct use of funds.

Conclusion

Undeposited Funds are operationally simple but financially sensitive. Under US GAAP, funds in transit require judgment grounded in control and cutoff principles. Controllers must implement formal review procedures, document receipt timing, and reconcile clearing accounts independently of the bank.

In SMB environments using QuickBooks Online, the difference between a clean month-end close and a material audit adjustment often lies in this single account.

Strong process discipline transforms Undeposited Funds from a nuisance into a reliable component of internal control.